I’m a hedger by nature.

Before I had a wife to remind me, I put my keys and wallet on the floor in front of the door so I wouldn’t leave without them.

I carry a portable power pack in my Jeep in case I forget to turn the lights off and the battery runs down.

I have not one, but two automatic bilge pumps in my boat, which has two separate solar charging systems to keep the battery that operates them fresh.

As I’ve written before, I also like to hedge my investments.

I always hold gold. When the COVID-19 virus first started to rock the markets, I bought exchange-traded funds (ETFs) that hold Treasury bonds and safe-haven currencies. While the rest of the market is down, those positions are up double digits.

Today, I want to tell you about another hedging opportunity. But it’s not one you’re going to read about in the mainstream news.

That’s because this hedge is designed to protect you from a veritable ticking time bomb in the U.S. economy. It’s the single biggest threat out there. And it is much bigger than the current pandemic.

And in the time it took me to write this article, it jumped 10%!

Lessons Unlearned

My tween-age daughter has a hard time learning from her mistakes. But she’s nothing compared to U.S. financial markets and policymakers.

A credit crisis blew up the global economy in 2008. Thanks to COVID-19, it could happen again this year.

What would have been a short recession 30 years ago nearly tanked the global economy in 2008 because irresponsible lending had leveraged U.S. housing markets into an unsustainable bubble.

When that bubble popped, the entire global economy had to deleverage … fast. The lucky ones, like Wall Street banks, got bailouts. The rest of us lost our homes and suffered through years of reduced earnings.

We are in bubble territory again … but this time it’s carefully hidden behind the crumbling façade of our 11-year-old bull market.

And it’s all because the lords of our financial universe are making the same mistake all over again.

Money for Nothing

When interest rates are extremely low in a growing economy, four things happen:

- Everybody, including lenders, searches for higher yield than they can get in the bond market.

- Borrowing becomes cheap and easy, both because lenders are eager to make loans and because borrowers assume they can easily make their payments.

- The volume and proportion of risky loans increases over time as lenders chase yield and borrowers chase cheap credit.

- Eventually, credit markets reach a critical point where everybody realizes this is unsustainable. Credit markets seize up. Borrowers are forced to default. It’s called a “Minsky moment” — named after economist Hyman Minsky, who first described this process.

Since the 2008 financial crisis, we’ve been building up to a Minsky moment in corporate credit markets.

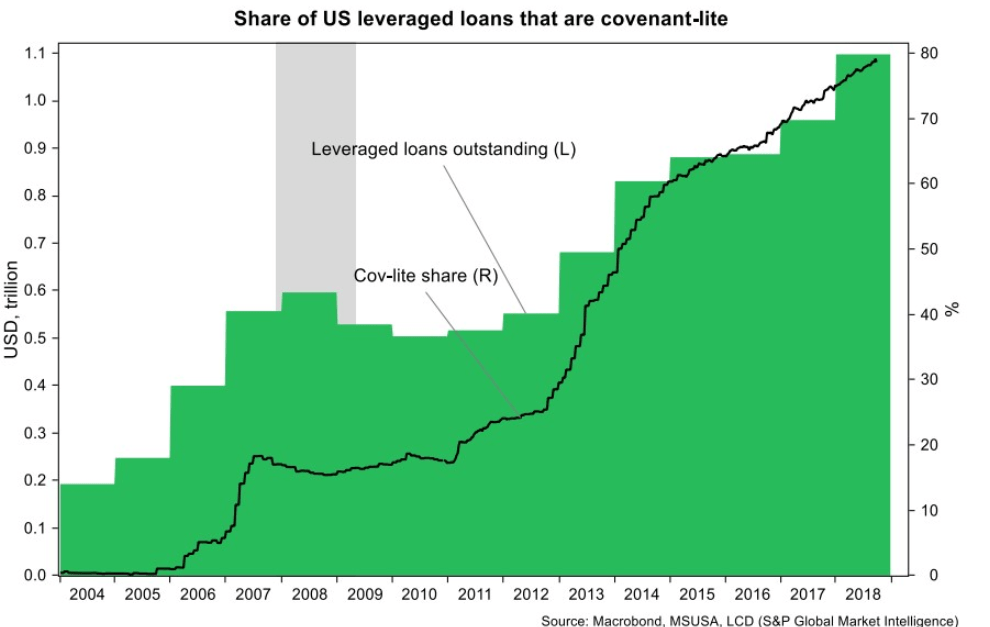

In corporate bond markets, “leveraged loans” are those made to companies with poor credit histories and stressed business operations.

Within the leveraged loan sector, “covenant-lite loans” don’t give lenders much recourse if the borrower doesn’t pay. They are the riskiest of all.

Starting quickly after the financial crisis, the total share of leveraged loans in the U.S. corporate sector began to rise rapidly. Last year, it reached over $1 trillion, compared to almost nothing before the financial crisis.

At the same time, the share of covenant-lite loans rocketed from around 20% of the total in 2010 to nearly 80% today:

As the volume and proportion of these so-called “junk bonds” expanded, so too did the pool of willing lenders.

After the financial crisis, certain rules discouraged mainstream banks from taking on too much risky debt. So in stepped a variety of nonbank lenders.

This “shadow banking” sector includes pension funds, mutual funds and hedge funds. All piled into junk bonds to earn bigger yields than they could get in the Treasury market.

Now, one of the distinguishing features of leveraged loans — and covenant-lite loans in particular — is that they tend to be short in duration. When the loan comes due, the borrower and lender simply roll it over into a new loan … until the lender balks for some reason.

A Minsky moment occurs when everyone decides simultaneously that they no longer want to buy junk bonds. Companies struggle to roll their loans over. Many of them have a tough time paying them. Hedge funds that have invested in junk bonds are hit with a wave of redemptions from their investors and are forced to borrow money in the “repo” market to maintain liquidity.

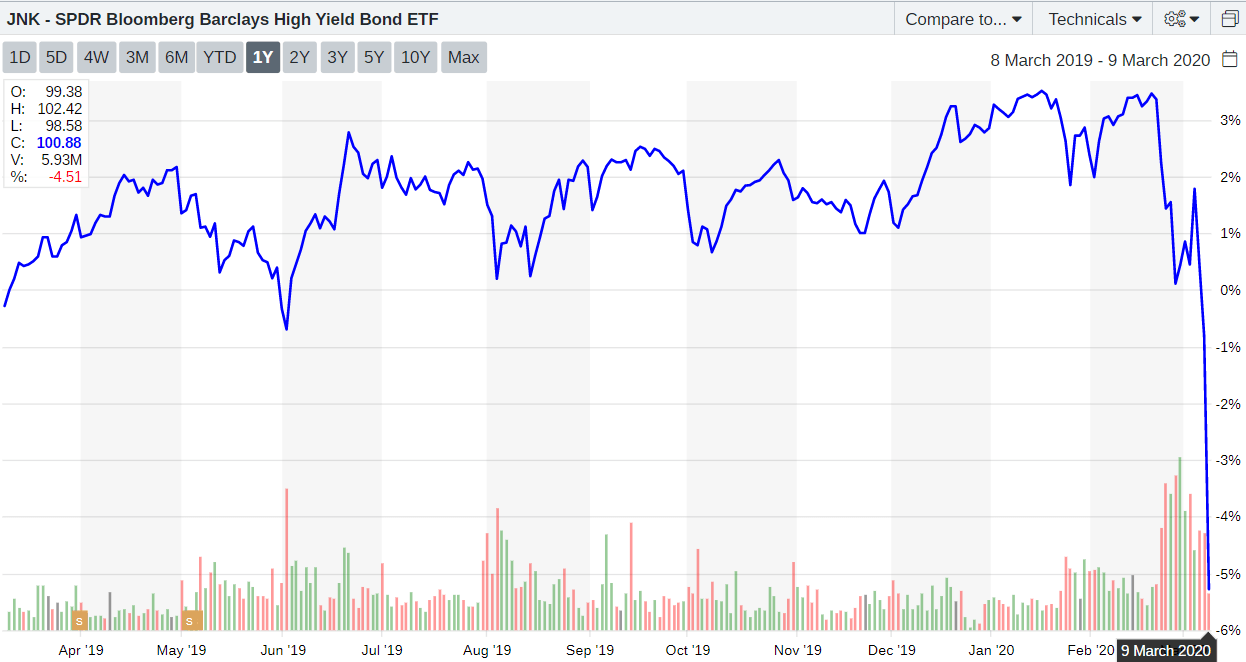

The chart below shows the yield on the biggest ETF holding high-yield corporate bonds, the SPDR Bloomberg Barclays High Yield Bond ETF (NYSE: JNK). The demand for junk bonds has evaporated practically overnight:

Profit From a Minsky Moment

The combination of this sharp drop in demand for junk bonds and the Fed’s decision to pump more money into the repo market tells me that we’re perilously close to a Minsky moment in the junk bond sector.

It’s too early to tell whether financial markets will pull back from this. If they don’t, we can expect a wave of bankruptcies and layoffs as financially stressed companies cease operations. That could easily tip us into recession.

There is one way to play this in your favor, however. It’s not for the faint of heart, and like similar strategies, it’s something you must watch every day.

I’m referring to the ProShares Short High Yield ETF (NYSE: SJB). It’s an “inverse” ETF designed to short the junk bond market. If JNK goes down by 5%, SJB goes up by 5%.

I predict SJB is going to appreciate significantly in the coming weeks and months. But remember, this isn’t something you want to buy and hold.

For one thing, the market could turn around suddenly and wipe out your gains. Also, inverse ETFs like SJB rapidly diverge from their target indexes for technical reasons. So, the best strategy is to buy SJB around market open and sell around market close.

Think of a strategy like SJB as a bilge pump for your own investment portfolio … but remember, it’s not automatic like the ones on my boat. You’ll want to pump it manually every day!

Kind regards,

Editor, The Bauman Letter