Mousetraps make me nervous. I put some out over the weekend. When I tested one with a pencil, it broke it in half.

There they sit up in the attic, quietly doing nothing. Just waiting for a trigger. Then … SNAP!

You see, I’m not worried about the long-term impact of the coronavirus. The Chinese markets, airlines and oil prices will decline for the time being. But ultimately, all of this will pass.

Meanwhile, an enormous financial mousetrap is in serious danger of being set off. And it could spell major disaster for the U.S. markets and economy.

Yet — for some reason — you never hear anything about it.

This Borrower’s Market Is Leading to Disaster

I have a thing about debt. I hate it. It’s dangerous. And it tends to blow up households … and economies.

Oh, I know that if everybody had to earn money before they could make long-term investments such as factories and houses, the economy would collapse.

The problem is that those uses of debt are declining relative to one just a step above gambling: “covenant-lite” corporate loans.

A covenant-lite loan has two characteristics:

- The borrower already has excessive debt and/or a poor credit rating.

- The lender agrees to make a new loan to that borrower without asking for promises to do things like reduce costs or allow the ratio of total debt to earnings to exceed a certain amount (“covenants”).

It’s as if someone close to bankruptcy went to buy a new house, and mortgage companies competed so hard for her business that she ended up with a deal that excluded the possibility of foreclosure.

Why would lenders make these extremely risky loans?

It’s simple: In today’s low interest rate environment, they offer better yield than other fixed-income investments like Treasury bonds and high-quality corporate debt.

Thanks to the Federal Reserve’s purchases of Treasury bonds from the market, trillions of dollars around the world are looking for yield. Risky corporate loans provide it.

But with so many lenders looking for deals, risky corporate borrowers can insist on conditions that favor them … such as abandoning restrictive covenants.

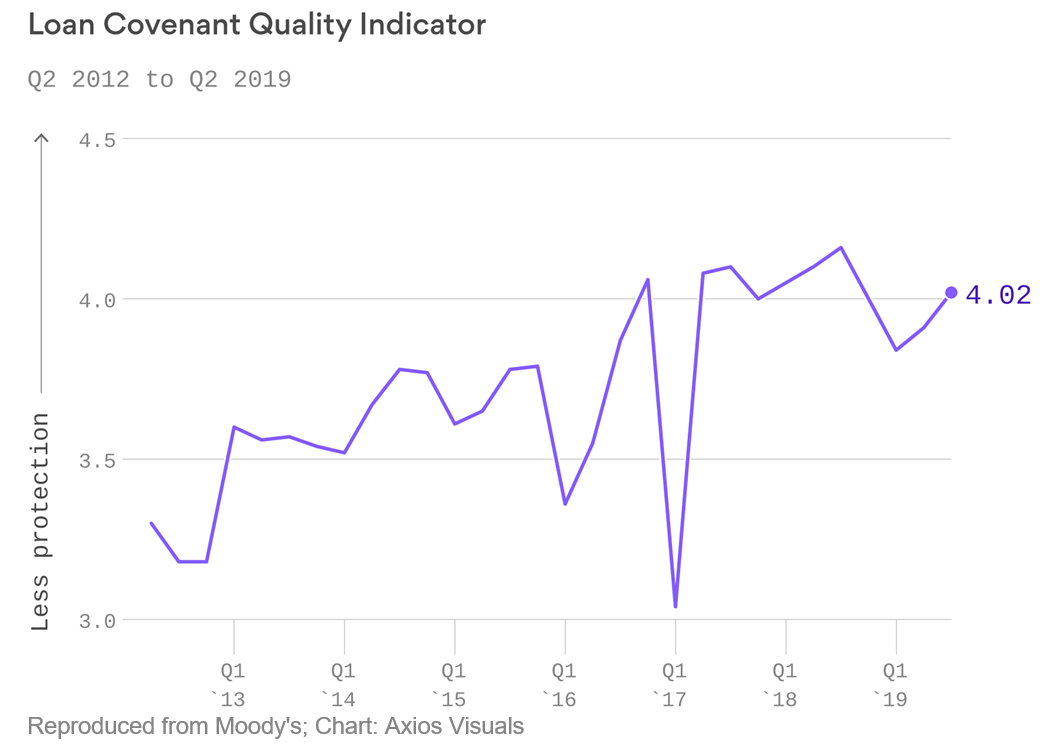

Ratings agency Moody’s measures loan covenant quality on a 5-point scale … with 1 meaning the strongest investor protections and 5 meaning the weakest.

It’s just risen to over 4 again:

According to Moody’s Senior Covenant Officer, Derek Gluckman: “The findings suggest that risks are increasing and that while investors are voicing caution, they are not effectively pushing back on permissive covenant terms.”

In other words, it’s a borrower’s market.

The Debt Mousetrap Prepares to Snap

Debt is a financial mousetrap. As long as conditions are stable, it just sits there on a company’s balance sheet.

Some companies become so dependent on debt that they’re known as “zombies” — financially dead, but still walking.

When enough companies reach zombie status — say, when the Moody’s measure exceeds 4 — all those individual mousetraps become one big mousetrap for the entire economy. Just like the mousetrap that sprung in 2008 when Lehman Brothers collapsed.

The coronavirus isn’t going to trigger the debt mousetrap. But eventually something will. A big, overindebted company will go bankrupt, and its lenders will be unable to meet their own obligations. That’ll cause the financial equivalent of a room full of mousetraps setting each other off.

Here’s the thing: You almost certainly know about the coronavirus — but you’ve probably never heard about the U.S. corporate debt mousetrap. Eventually, there will be a catalyst that springs the corporate debt trap. It’s only then that you’ll hear about it.

But it’s best to start preparing for it now. You can do that in two ways. Build a hedging position around assets that move opposite the market in the crisis … and keep a close eye on debt levels:

- Buy gold. Everyone should keep at least 5% of their portfolio by value in gold, either via exchange-traded funds (ETFs) like the SPDR Gold Shares ETF (NYSE: GLD) or by owning the metal itself. As you get older, you should increase the proportion of gold in your portfolio to between 10% and 15%, depending on your situation and preferences.

- Hold safe-haven currencies. My Swiss friend always advises his clients to keep some of their holdings in the Swiss franc and the Japanese yen. That’s because, like gold, both currencies tend to appreciate when the broader market suffers a downturn. You can either buy them directly through your broker or by investing in ETFs such as the Invesco CurrencyShares Japanese Yen Trust (NYSE: FXY) and the Invesco CurrencyShares Swiss Franc Trust (NYSE: FXF).

Most importantly, go beyond the headlines and keep yourself informed.

I don’t wait for the headlines to tell me that there’s trouble brewing. I set up Google alerts for search terms like “covenant-lite,” “corporate debt” and “loan covenant quality.” That’s because I want to know everything I can about the mousetrap … not just the mouse that triggers it.

You can do the same thing … and you can keep reading Bauman Daily, where we’re committed to giving you the whole picture, mousetraps and all.

Kind regards,

Editor, The Bauman Letter