Normally, predicting the economy is easier than picking winning stocks.

Economic indicators like the purchasing managers’ index are pretty reliable, while individual companies can generate all sorts of surprises.

In 2020, the pattern reversed.

Successfully predicting the performance of the U.S. economy was impossible. “Exogenous” variables like stimulus payments and infection rates determined everything.

On the other hand, as someone commented on one of my recent YouTube videos, “Even my dog made money in the stock market this year.”

The difference?

A Rigged Market

The degree of “freedom” of the real economy versus financial markets in 2020.

Although federal stimulus payments replaced some lost income, investment — the number one driver of economic growth — was way down. Rational businesses and households (with one exception: housing) decided to keep their money in the bank. Stimulus wasn’t enough to override basic economic signals, which were terrible.

But financial markets reaped the benefit of a market that was anything but free.

Global central bank injections of nearly $8 trillion meant that the pricing of equities and bonds wasn’t based on the free interaction of demand and supply. The market was rigged. Investors — and presumably, some dogs — made a killing.

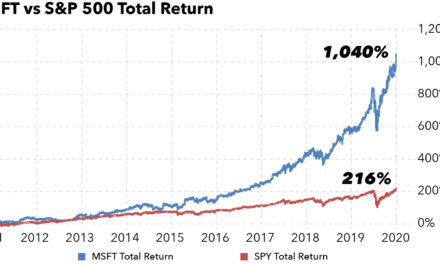

Of course, smart investors made outsized returns by doing what they always do: hunting for the best companies. We certainly did that in The Bauman Letter, where we’ve had incredible market-beating gains this year.

Overall, however, the real economy was riddled with risk … while the Federal Reserve created an environment in financial markets where there was no such thing.

That can’t go on forever … and Wall Street knows it.

So what should you expect from 2021?

Above all, what should you do?

2021: Over to Earnings

It’s difficult to pinpoint the Fed’s contribution to stock market gains this year. But one thing is clear: Gains after the massive interventions of March were far greater than for the year as a whole.

Clearly, if the Fed hadn’t intervened, this year would have been a catastrophe for equity investors.

The problem is that the Fed’s intervention has left U.S. stocks dramatically overpriced relative to their actual earnings.

As the chart below shows, all markets are overpriced. The U.S. is in a league of its own:

Fed apologists like to say equity markets are forward-looking. If stocks are overpriced relative to earnings, it’s because investors anticipate increased earnings in the future. They’re willing to pay more for stocks now with the expectation that companies will “grow into” those valuations.

There are two problems with that view … and I predict both will be big topics of discussion in 2021.

- At some point, the “growing into a high share price” logic reaches its limits.

Tesla (Nasdaq: TSLA) trades at 1,280 times current earnings. At this level, it would take the company 1,280 years to “grow into” its current share price.

Of course, we can expect Tesla to increase its earnings over time. That’s exactly what Tesla bulls argue.

But Tesla’s present market capitalization exceeds that of all other publicly listed automakers combined. For Tesla to grow into its current valuation, it needs to achieve annual sales more than the entire global automobile market.

Next time somebody tells you a company will “grow into its share price,” ask them how many years it will take and how much of the market it will need to capture along the way.

- Future earnings are usually overstated.

Every year, companies and Wall Street analysts try to estimate next year’s earnings. Almost every time, they overshoot.

The chart below shows annual earnings-per-share forecasts (light blue) for S&P 500 companies compared to their actual results (dark blue). Over the last decade, earnings have only significantly exceeded forecasts twice — in 2010 and 2018:

That suggests 2021 earnings estimates are overblown and that many companies will consistently miss them.

Given other clouds on the horizon, that won’t be good for their share prices.

The Fed Plays Lucy

I’m willing to bet that many investors will ignore the above because they assume the Fed will continue to rescue equity markets no matter what ails them. They’re used to “unfree” financial markets, and they like them that way.

As the Fed has made abundantly clear in word and deed, however, it’s done supporting equity markets for now.

It’s concerned about the dramatic increase in wealth inequality distorted equity markets have caused. It’s more concerned about the state of the real economy, but its toolkit is practically useless for that.

And on top of that, the Republican majority in the Senate clearly wants to rein in the Fed and prevent it from taking aggressive steps for the foreseeable future.

So, for those who expect the Fed to keep their portfolios bubbling next year, fix your mind’s eye on the image of Lucy whipping the football away from Charlie Brown. That’s likely to be your experience.

Despite It All, Not a Bearish Call

Of course, COVID-19 hasn’t disappeared yet, and won’t be for a while. Depending on the outcome of the election here in Georgia on January 5, we shouldn’t expect significant federal stimulus either.

My bottom line is that the spectacular rise in stock valuations in popular investment sectors like technology and online retail is likely to slow and even stall next year. Stocks are just too expensive, and the tailwinds are evaporating.

But read my lips: I’M NOT BEARISH ON 2021.

As I’ve argued repeatedly this quarter, I’m bullish on European and emerging markets, renewable energy and underpriced value stocks.

I see rapidly growing long-term opportunities in electric vehicles, battery energy storage, and cloud-based software. All of those are going to be in my sights next year.

The single biggest factor guiding my approach to the markets in 2021 is how free they are.

For generations, we’ve been encouraged to understand economic freedom as the absence of constraints, like regulations and taxes.

But real economic freedom is the absence of all forms of government intervention, including stimulus. It’s the freedom for markets to find their own price and output levels, good or bad.

My political sniffer tells me that in 2021, markets are going to be a lot freer than they were this year. … for good or bad.

That’s going to place a premium on expert stock market analysis and advice.

In truly free markets, investors need the sort of intensive research that The Bauman Letter brings. It’s why, even though Fed and congressional stimulus evaporated in the second half of the year, we’ve seen open gains of 42.8%, 52.2% and even 70.01% in only three months. Of course, these are some of our best gains, but they show the incredible potential of our strategy.

So, in 2021, let your dog play his brokerage account the way he did in 2020.

If you want yours to prosper, stay tuned to this channel, and let’s make the big money!

Kind regards,

Editor, The Bauman Letter