Over the weekend, I had dinner with a Swiss friend who runs an investment management firm in Zürich that caters to Americans.

My wife and daughter found our after-dinner shop talk excruciatingly boring and retired to the TV.

That’s when the conversation really got going.

We shared war stories. In different ways, our job is to find market-beating returns … and to provide accurate explanations when the market moves the wrong way.

It can be a tough task.

For example, I mentioned that my Profit Switch service had outperformed major U.S. benchmarks since the beginning of the year. It was down only 1% compared to a 5.5% slide for the S&P 500, and over 10% for the Nasdaq.

My friend said his managed portfolios enjoyed a similar performance. Despite that, his clients weren’t impressed. They wanted yield in all conditions, not just to protect their capital against pullbacks.

That led to a discussion of ways to make money in a downturn. We covered hedging currencies, like the Swiss franc and Japanese yen. We spoke about gold. We considered commodities, agreeing they were a good short-term play, but would suffer if rising interest rates led to a recession.

Eventually, we came to inverse leveraged exchange-traded funds (ETFs) … those tempting plays that promise to make money when markets decline…

Protection Through Leverage … or Playing With Fire?

Leveraged ETFs use derivatives to amplify the returns of an underlying index. They aim to return two or three times the gains of the index over a specific period.

Inverse leveraged ETFs promise something even more remarkable: gains two or three times larger than the decline of its index.

For example, imagine an index ETF is trading at $100 a share, and its “3X inverse” ETF is trading at $20. If the index falls by 10% to $90, the inverse ETF will increase by 30%, to $26.

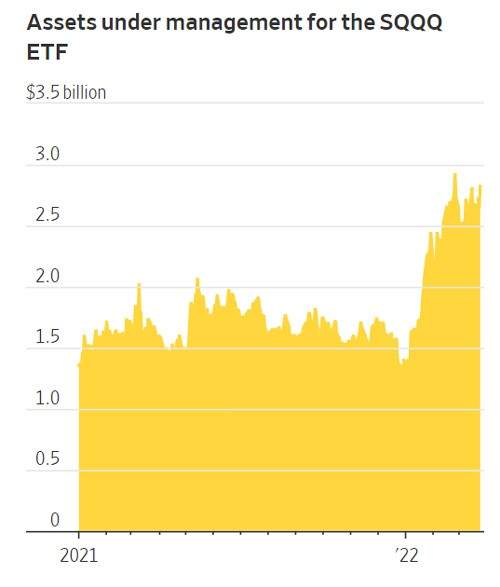

The Wall Street Journal recently reported that retail investors who cut their teeth in the Federal Reserve-induced hyper bull market of 2020 are now redirecting their animal spirits to these leveraged inverse ETFs:

Evan Fetter, a 25-year-old in the U.S. military, saw an opportunity to swing for the fences. He poured $15,000 into the ProShares UltraPro Short QQQ (Nasdaq: SQQQ), an exchange-traded product that is designed to triple the daily return of the Nasdaq 100 Index, bidding for what he called a “once-in-a-lifetime gain.” The trade has been underwater at times, but Mr. Fetter says he hopes to hold the shares until his investment is worth $50,000.

Mr. Fetter is not alone. Inflows to SQQQ have skyrocketed since the beginning of the year:

Is Evan Fetter’s SQQQ buy-and-hold strategy a good one?

Nope. Here’s why.

2 Reasons Not to Hold Inverse Leveraged ETFs for Too Long

Leveraged ETFs use a combination of index futures, options and leverage to produce their returns.

There’s only one problem: The strategy only works one day at a time.

That’s because index futures and options are subject to “time decay.” The closer both derivatives get to their maturity date, the less valuable they are. They only provide their full potential return on the day they’re bought.

Because of that, managers of leveraged ETFs must rebalance their futures and options holdings daily. Every day, they sell the previous day’s contracts, roll them over into new ones and adjust their holdings to reflect moves in the underlying index.

For this reason, you’re only guaranteed two or threefold returns on a leveraged ETF on the day you bought it. After that, “tracking error” will eventually reduce your returns to much less than that.

So, problem No. 1 is that if you’re going to trade leverage inverse ETFs, you’ve got to watch the market like a hawk. You must buy and sell your holdings every day.

Problem No. 2 is that inverse leveraged ETFs amplify the direction of the underlying index. If the index goes up, you gain two to three times as much money as it does.

The same is also true in reverse. If the index pulls back, you lose two to three times as much.

For these reasons, holding inverse leveraged ETFs over long periods can be a recipe for disaster. Mr. Fetter’s plan to turn $15,000 into $50,000 with SQQQ is almost certain to fail.

Rules of the Road

But that doesn’t mean you must avoid inverse leveraged ETFs. Just follow these rules:

- Only use them when the market has a confirmed trend, either up or down. Using them in periods of high volatility leads to so much whiplash that gains and losses usually cancel each other out … or worse.

- Only purchase leveraged ETFs with good liquidity and volume. Remember, you want to be able to buy and sell these instruments with precise timing. Insufficient liquidity could mean that you can’t find a seller or buyer, or that the bid-ask spread is too high to make it worthwhile. Make sure you choose ETFs with at least 500,000 trades per day. For similar reasons, target ETFs with at least $100 million in assets under management.

- Leveraged ETFs require active management, which is more expensive than passive index funds. So, you should expect to pay higher expense ratios, but don’t buy an ETF that charges more than 1%.

- Be prepared to monitor the performance of a leveraged ETF throughout the day. If you’re unable to do this, use a percentage-based trailing stop to protect yourself from a sudden intraday change in market direction … something we’ve seen repeatedly this year.

- Be prepared to see significant losses on days when the market goes against you. If you find that hard to handle, avoid leveraged ETFs altogether.

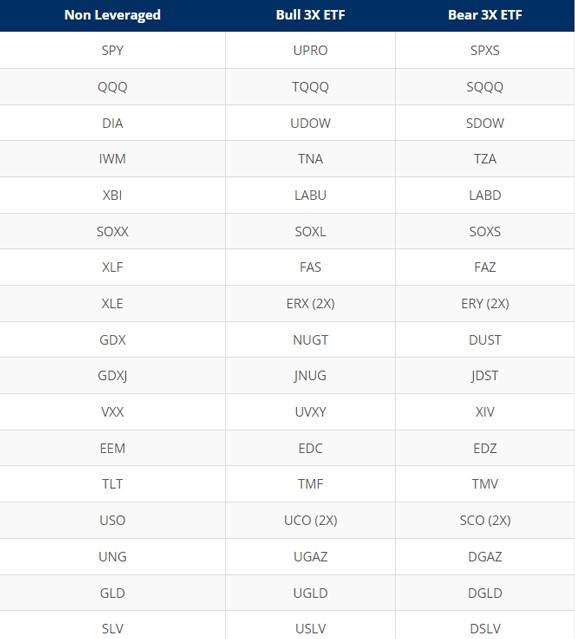

If you think you can abide by these rules, here are some of the most popular bull and bear triple-leveraged ETFs:

My Swiss friend and I don’t use inverse leveraged ETFs in managing our professional portfolios. It’s too complex, risky, time-consuming and time-sensitive to do on behalf of third parties like his clients and my subscribers.

But if you’ve got the guts to try, go for it … one day at a time!

Kind regards,

Ted Bauman

Editor, The Bauman Letter