Earnings reports are strong from top companies, but are they strong enough to carry stock prices higher as 2022 presses on?

In today’s episode of Your Money Matters, Ted and Clint reveal a few “Big Picture” factors that could signal where stocks are headed … and which stocks might make the best buy.

Click here to watch this week’s video or click on the image below:

Transcript

Ted:

Hello everyone. It’s Ted Bauman here with Clint Lee, with your weekly Your Money Matters video from Big Picture, Big Profits. For those of you who have asked, we have renamed our free e-zine, or whatever you want to call it, our free emails that come out four days a week. We don’t send it out on Thursdays. It’s called Big Picture, Big Profits. Now. If you’re interested in subscribing to that, or to The Bauman Letter, you can click on the link above my left shoulder, up in the corner. There’s a little eye that’ll take you to a landing page, where if you’d like to give The Bauman Letter a try, you can do so with a money-back guarantee, for 12 months. You can get your money back at any time, if you like.

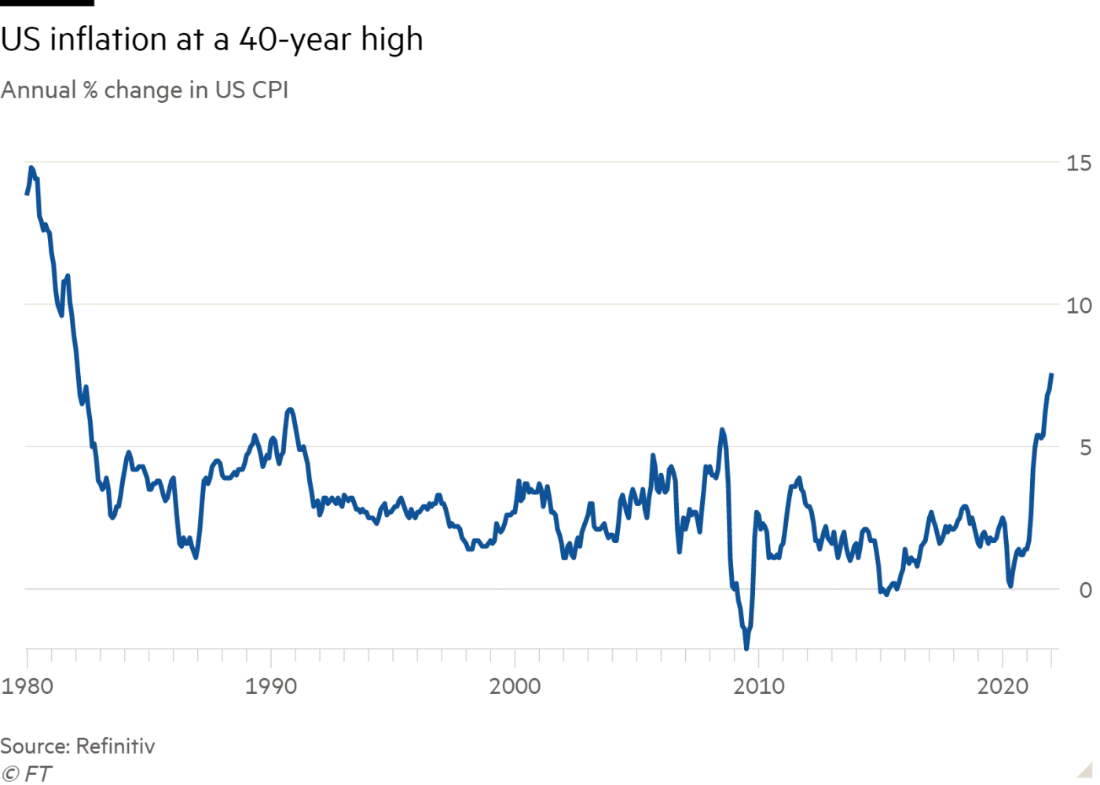

Today, we’re going to talk about the prospects for companies within the prospect, or rather, with the threat of the combination of a pullback in the stock market and a pullback in the economy. I spoke about this on Friday in my video, and on Friday I spoke about four things that you can do to preserve capital. What I didn’t talk about was what you could invest in. I did talk on Friday about some certain types of ETFs, which will hedge you on the downside. Today, we want to talk about companies that are likely to do better than other companies if we do, in fact, see a recession later this year or next. Let’s start with some basic facts. U.S. inflation is at a 40-year high, here is the chart:

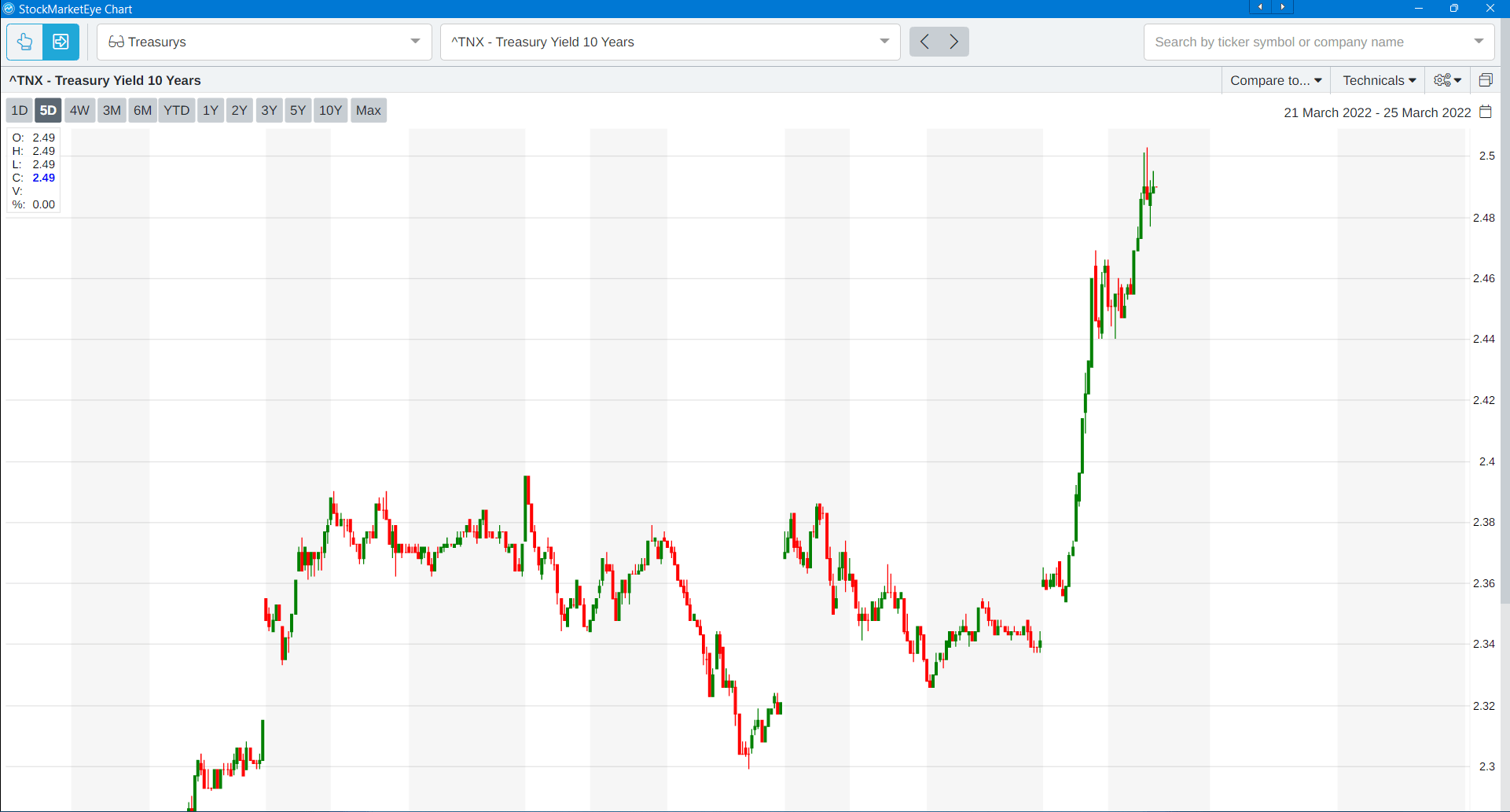

We are comfortably above the inflation rates that we saw in our most recent boosts or bumps in inflation. One was just prior to the subprime crisis, the other was in the early 1990s. The big inflation really happened in the ‘70s and ‘80s. We haven’t gotten to that point yet, but we are certainly at a higher point than we have been. Now, the reaction to this is what’s important, and this is where I think a lot of danger falls for certain kinds of companies. Here is a five-day chart, the last five trading set for the 10-year Treasury:

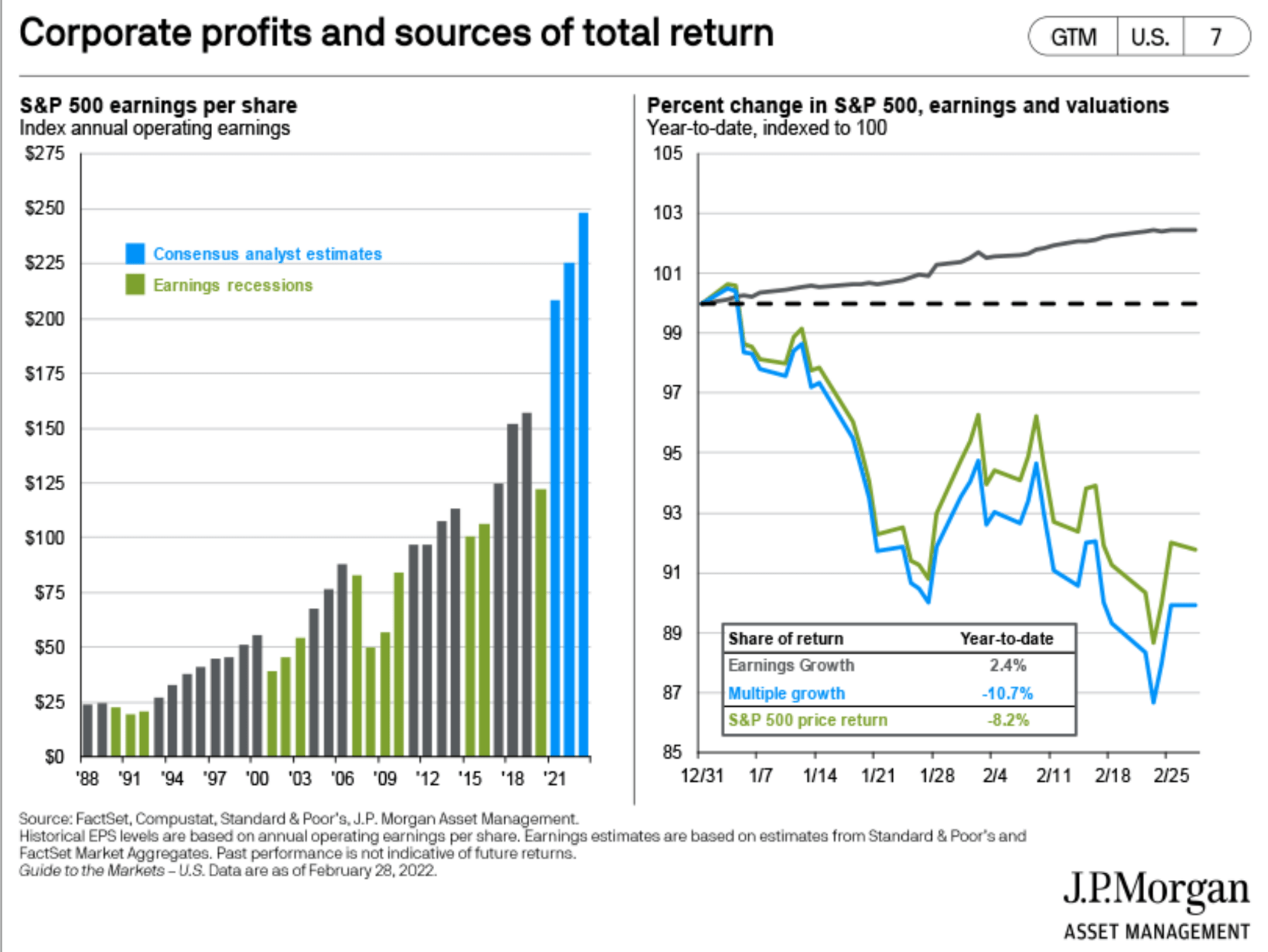

Look at today’s action. We jumped today, big time. Obviously there’s a big pull away from bonds now, that’s raising yields. A lot of people are going into cash, probably doing some of the things that I recommended, like going into gold and other things, pulling out of bonds. The key thing here is that there is an expectation of short-term pullback in the economy, and that is usually what happens. The sign that you usually get is a pullback in bonds, if that’s happening. Finally, let’s look at earnings projections, or rather, what’s happened so far this year. Not projections, but what’s happened with earnings and with multiples:

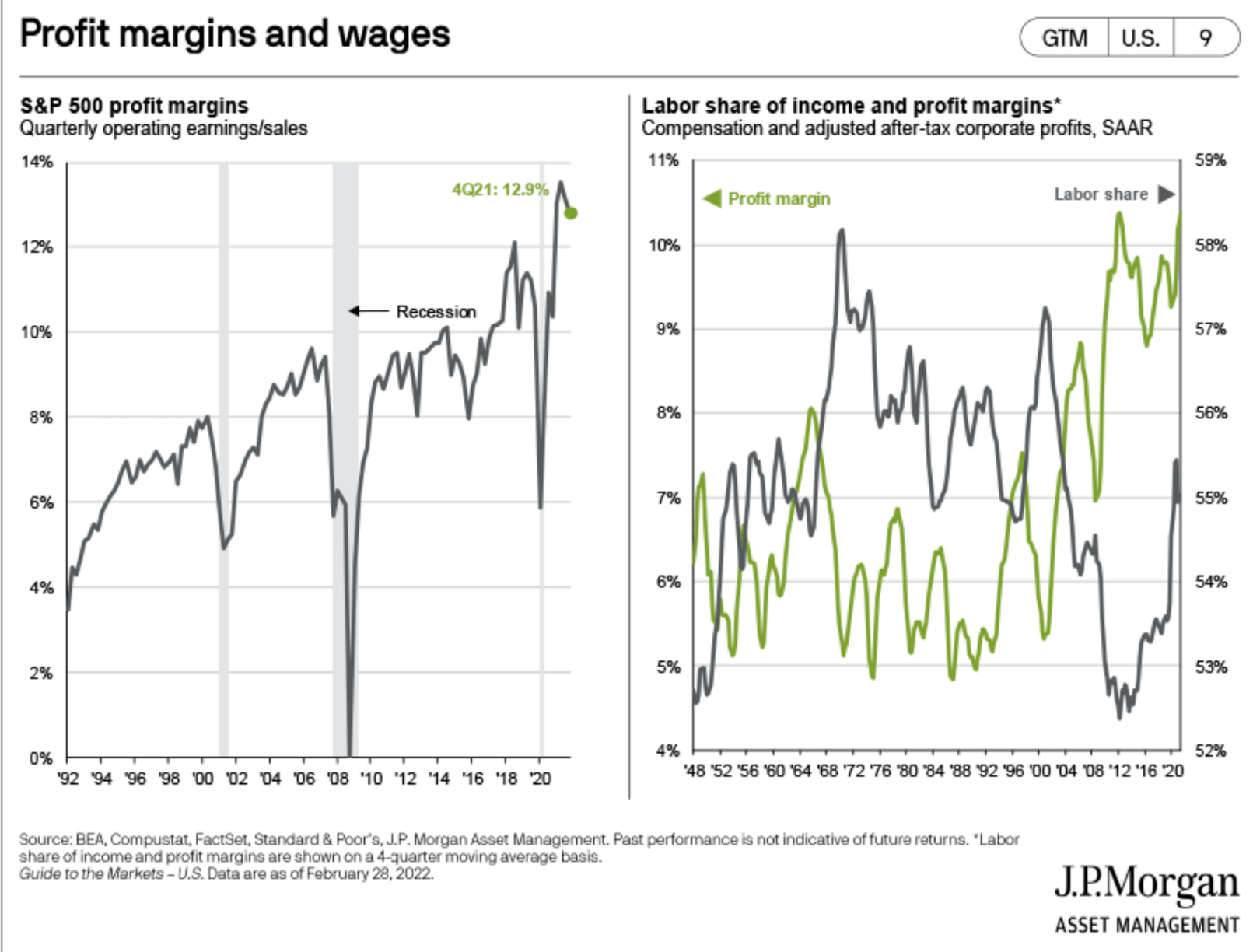

This is an important consideration. When you talk about multiples, basically you’re talking about people willing to pay more for a share, more for a dollar of earnings. What we’ve seen this year is a pretty significant pullback of multiples, almost 11% overall, but we’ve seen earnings growth that doesn’t actually compensate for that. The big question is, can we expect earnings to be strong enough later on this year to be able to lift stock prices, not necessarily across the board, but in specific sectors? If so, how do we anticipate which sectors those will be? The last thing I want to bring your attention to is one of the most important variables in earnings, and that is the price of labor.

Even though, in a lot of important sectors of the economy, like Big Tech, labor is not as big of a component of input costs as it used to be for manufacturing firms, it’s still important. This chart shows that we’ve seen a pretty good increase in profit margins during the last decade or so. We saw a big pull back during COVID, but they’ve bounced back even stronger than before. The critical thing, though, is that has reversed course more recently. We’ve started to see a pullback in that. On the right-hand side, we can see what is basically an inverse relationship between profit margins and the cost of labor. The green line is profit margins, and to look at the most recent action, going back to the subprime crisis, labor compensation fell dramatically as a proportion of earnings, or rather, basically as a proportion of corporate income and earnings. Labor picked up again, starting roughly in 2014, 2015, then it took off big time as the economy got tight, but it’s now started to pull back again.

The critical thing is, if labor becomes more expensive, that is hard for companies who are trying to make profits. It certainly means that the ability to grow profits, to compensate for falling multiples, is constrained. Clint, what are the big factors that we’re looking at in squeezing profit margins of potential earnings this year?

Clint:

Yeah, it really comes down to three or four key challenges to that earnings picture, and being able to maintain those margins. If we talk about what those challenges are that’s going to help guide us to sectors to avoid, and where some opportunities may be at. First, let’s talk about input costs in general, for corporations.

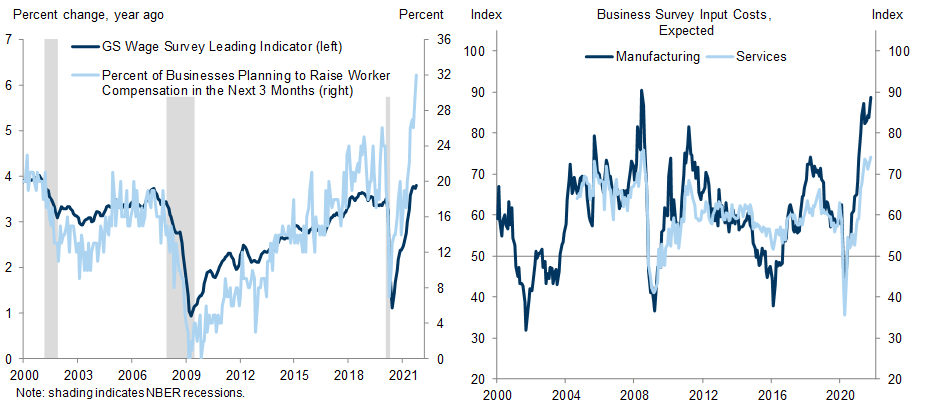

The first chart I have here, this comes from Goldman Sachs, and this shows input cost, or what businesses are expecting in terms of input cost. When this line’s rising, that means a higher level of cost, and vice versa when it’s falling. Now, it’s important to note that this does not include labor, this is non-labor input cost. You can see for both the manufacturing and services sector, this goes back to 2000.

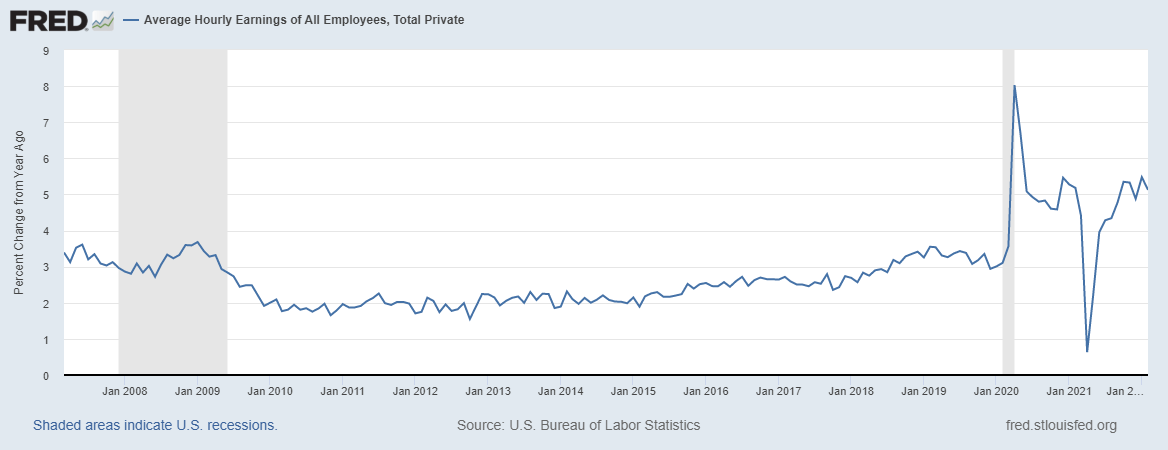

On the right-hand side we’re seeing a big spike up. We’re seeing both the manufacturing and services sector are running at levels that are the highest since the 2008 time frame. You’re going to the financial crisis, a big hallmark back then. Characteristically, the economy back then was surging energy prices. A lot of people don’t remember the surge in oil prices that we were seeing back in 2008. That’s definitely a factor this time around as well, for input costs in general, and overall levels of inflation that you pointed out earlier. Now, that’s non-labor. Let’s look at the labor side of the equation here really quick. The next chart I have, this is average hourly earnings.

This comes from the payrolls report that’s released on the first Friday of every month. This goes back to 2008, and you can see on here, this is a tale of two regimes, two different economic cycles.

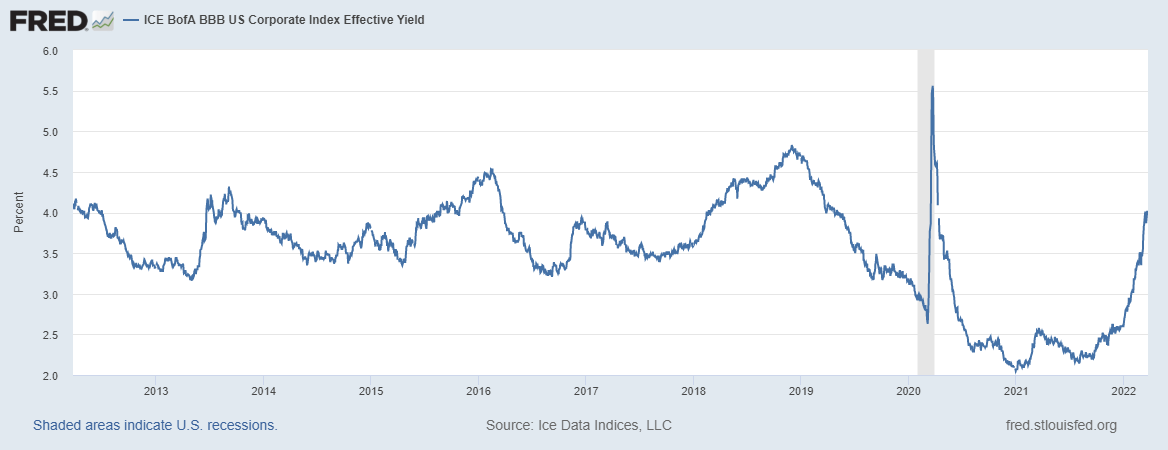

If you look at the right-hand side, there’s some volatility, some variability in this number, but if you look at where we’ve been at the last several months, we’ve been trending right around this 5% growth in average hourly earnings year over year. You look before the pandemic, and we were in that 2% to 3% range. Highlighting both the labor costs that are increasing for businesses, and the impact that can have on profit margins. One other rising cost, I really haven’t seen much discussion around this lately, but it’s the impact of rising interest rates, and what that means for interest expense for businesses. We know there’s been a lot of corporate borrowings over the last several years at rock bottom rates. Now, those rates are rapidly readjusting. Here’s a chart, this shows the average yield for BBB corporate bonds, investment grade bonds.

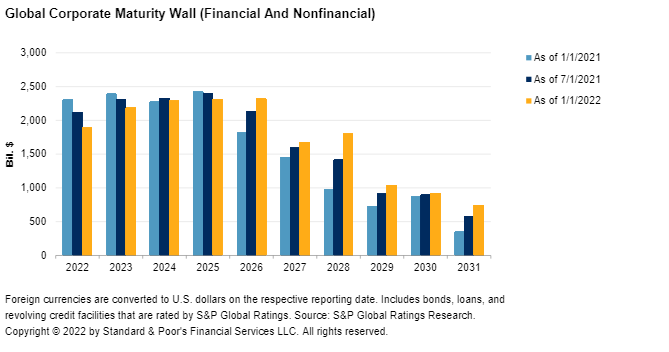

I took this back to 2013, just so you can see the peaks and troughs and different cycles. We had the big drop post-pandemic, we spent a couple of years, 2020, some of 2021, in this 2% to 2.5% range. Rates have doubled, you see the spike higher, we’re now sitting at 4%, and here’s why this is so important. Here’s a chart that shows corporate maturities coming up over the next several years:

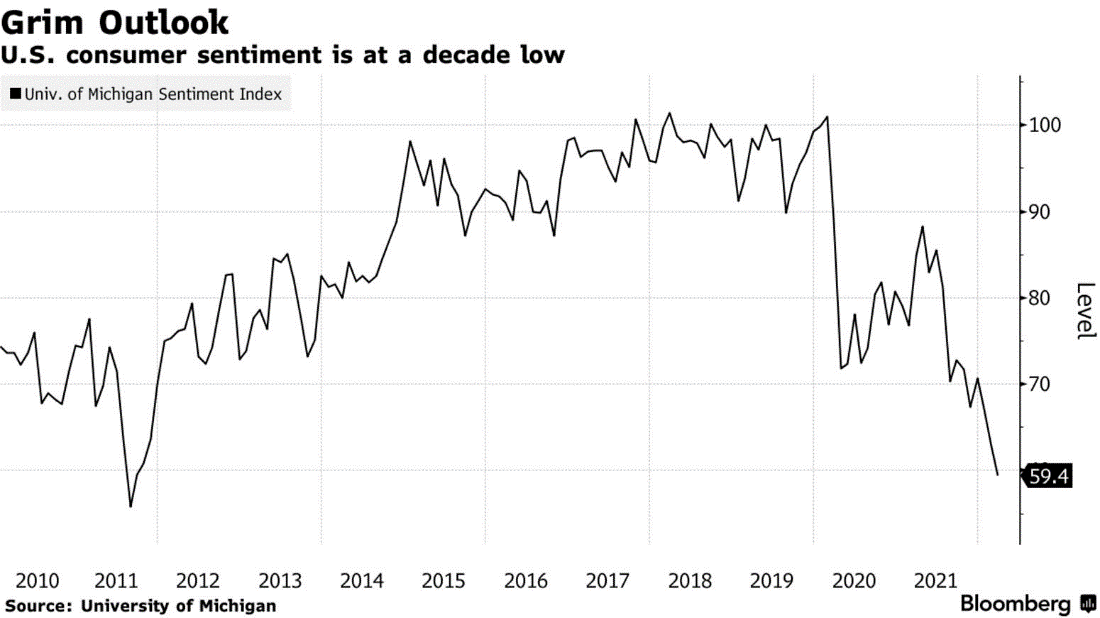

This comes from the S&P. This is only for bonds for companies rated by S&P. The key point here is, you look at the orange line. The orange bar is the more recent projections. Just in this year and next year alone, 2023, there is $4 trillion in global corporate maturities. Once again, this is just on the bonds rated by S&P. Companies are going to have to refinance, and they’re going to be refinancing at a much higher interest rate than when they originally were issuing those bonds. Now, this is all, impacting the cost side of the equation. One other big concern is what could happen with the top line. That’s because consumer confidence levels have been plunging lately:

We actually got an updated look today, as we’re recording this, at the University of Michigan, they put out a consumer sentiment number, and that that dropped to 59.4 in the most recent report. That is the lowest level in a decade, a big cause for concern. What’s driving that rating lower has a lot to do with inflation. The concern now is, or does that ultimately start to flow through into consumer spending figures, and impact the top line of corporations as well?

Ted:

Essentially, what you’re saying is that businesses are getting it coming and going. They’re getting rising input costs on the one side, and if consumers are not feeling positive about the future, they’re liable to pinch pennies, which means that companies that are selling things that people can do without, discretionary expenditures could be a real problem. What’s the strategy to deal with this? I’ll just throw in my $0.02. I think one of the things that you want to look for is companies that have what Warren Buffet likes, which is moats. Moats are companies that really have, for whatever reason, whether it’s a positive or negative reason, are able to limit their competition. They tend to be companies that have large footprints, where there are a few number of firms. Take telecoms, for example, a classic case in point.

We’ve only got three or four big telecoms company in the United States. Those guys can raise their prices, because what are you going to do, stop using a telephone? Are you going to stop using internet? No. They can raise their prices. That’s the kind of company that you would expect to perform better than the market going forward. Now, remember what we’re saying, we’re not saying these companies are going to see huge gains. What we’re saying is that they’re going to outperform the rest of the market. That’s critical to understand, I think, because we’re coming out of a decade when people are used to seeing huge gains in firms. We’re moving into a situation where you just want to get whatever gains are on offer.

I think that’s a critical thing to remember. That doesn’t mean there won’t be some companies that go ballistic. We’ve got a couple in our Bauman Letter/Profit Switch and you’ve done some great options trade on them. What we’re trying to do here is eek out gains when everybody else is flat-lining. What have you got first Clint?

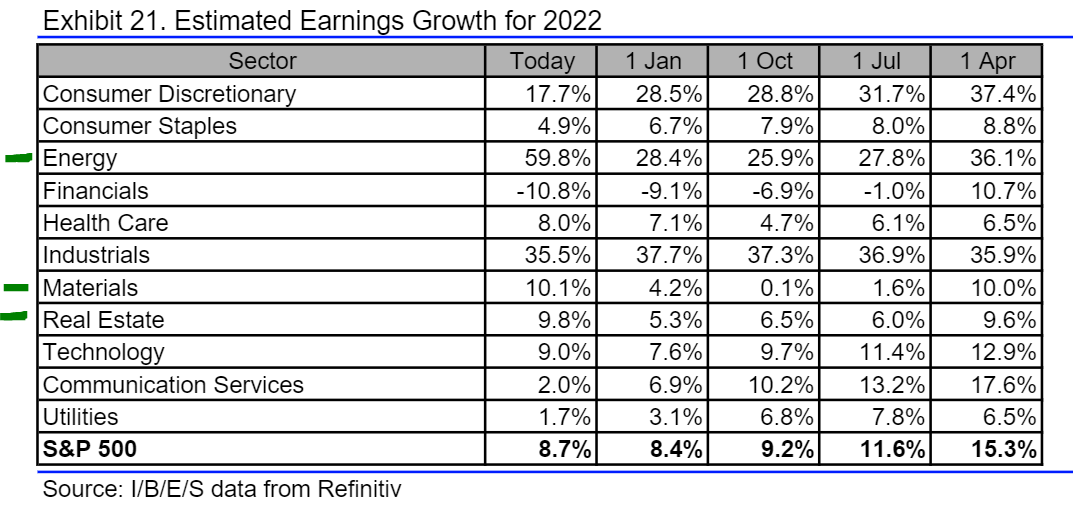

One area I would look at is to follow positive trends and analyst revisions. Look at the companies, the sectors where analysts are in real-time taking into account what’s going on, and you’re seeing a positive direction of profit revisions. A table to illustrate where you’re seeing some of this, this shows the different S&P 500 sectors, you’ve got the S&P 500 at the bottom.

This shows by date, throughout time, how the earnings growth trajectory is looking for 2022. On the left-hand side of these columns, you can see where that stands today versus various points in the past. I’ve highlighted a couple of sectors on here where you’ve seen, once again, this positive trend in earnings revisions. Look at energy, for example. At the start of this year, on January 1, the energy sector was expected to post 28% earnings growth. Today, that number has jumped to 60%.

You can go through and look at different sectors. Some others that stood out for me were materials, I’ve seen a nice revision. We talk a lot about real estate as well. A lot of REITs have this built-in ability to pass on increased costs that factor in inflation, in terms of higher rents. You’ve seen a positive revision in real estate as well. When I take it all together, taking into consideration the input cost, what we’re seeing in commodity markets, one ETF I like, and I wrote about it as well this week, is ticker MOO. It’s the VanEck Agribusiness ETF. A lot of companies in there are exposed to some of the rise in commodity prices, especially what we’re seeing in terms of crop prices, fertilizers. A lot of companies, established players in the agriculture space, have moats like you mentioned, Ted. That’s one ETF I would look at here as well.

I see what they did there, with MOO as the name of their ETF. I’m going to throw out VNQ, and I like VNQ because, basically, it’s real estate, which is primarily REITs in VNQ. You mentioned them, but one of the critical things about the REIT sector, a lot of people think, interest rates are rising, that’ll be bad for them, because they have a lot of capital, they borrow a lot. One of the things about REITs, especially quality REITs, the ones that we focus on in The Bauman Letter, is that they can achieve much lower weighted average costs of capital than a lot of other companies, because they have real assets behind their operations. They’re not just borrowing against future earnings, they’re borrowing against real assets, which means that banks are willing to accept a lower risk premium for those kinds of companies.

Also, because they’re very labor light, they don’t have a lot of employees, you can run an enormous real estate portfolio, particularly things like industrial warehouses, you name it, you can do it with a very light head count. Those companies can actually do much better than you would think, even under a tightening scenario. Also, in a recessionary scenario, because they lock in their rental increases, you have low-weighted effort, cost of capital, you have long-term rentals that have inflation escalators built in. They say land, safest houses and all that, I think the REIT sector is going to do well.

Obviously, you want to be discriminatory, in the sense that you don’t want to go for REITs that don’t qualify in that sense, that are going to pay higher interest rates for their borrowings. Look for the quality ones, the ones that have huge balance sheets, lots of cash. That’ll also mean that you’ll get dividends, which is something that you’d really like to have in a weak market.

Anyway, that’s all from us this week. See you again next week. Clint won’t be with us, but I’ll have somebody with me, we’ll see who it’ll be. We’ll see you next week, on Monday. I’ll be on my normal YouTube video on Friday. See you next week.

Good investing,

Angela Jirau

Publisher, The Bauman Letter