Good breadth is a sign of a high-quality market.

And we just haven’t been seeing that lately.

The bulk of the S&P’s gains has come from just five stocks: Tesla, Nvidia, Google, Microsoft and Apple. Meanwhile, more and more stocks keep declining.

It’s like a dangerous game of stock market Jenga. The tower is still there, but pull out the wrong block, and it all comes tumbling down.

Could a Federal Reserve interest-rate hike bring about the big downfall?

Ted Bauman and Clint Lee talk about the best- and worst-case scenarios, which types of stocks would be hit the hardest once the Fed pulls back, industries that are likely to do well and the perfect defensive exchange-traded fund.

Will the Tower Collapse?

The Jenga tower has fewer and fewer supporting blocks.

From the top, everything looks great. From below, it’s a mess.

According to Bloomberg: “The broad indexes were only down a few percentage points, but there were more than a thousand stocks making 52-week lows on a daily basis. And, of course, the stocks that went up were the same ones that seem to always go up: Apple Inc., Microsoft Corp., Nvidia Corp. and a few others.”

In a deceptive market such as this one, what’s left to choose from? Will this be another dot-com bust? Find out what Ted and Clint have to say and what you should look out for during times like these.

Click here to watch this week’s video or click on the image below:

VIDEO TRANSCRIPT

Angela: We’ve spoken a lot this year about the deceptive markets. I know I’ve opened with this a few times, but it’s just been an ongoing theme that we’ve had a handful of stocks really generating the bulk of the gains in the market.

This market keeps wanting to pull back, but the buyers are diving in. They’re buying the dip and they’re not allowing that to happen, but now I don’t know if things might change because of what’s going on, but it looks like the Fed is serious about ending QE.

And now people again are nervous about inflation and they demand that the Fed is going to raise rates and there’s all this pressure building. If that happens and the dip buyers say sayonara, what’s going to happen and what’s the best place to park your money in that worst case scenario?

Ted, I’d like to open up those questions to you to start.

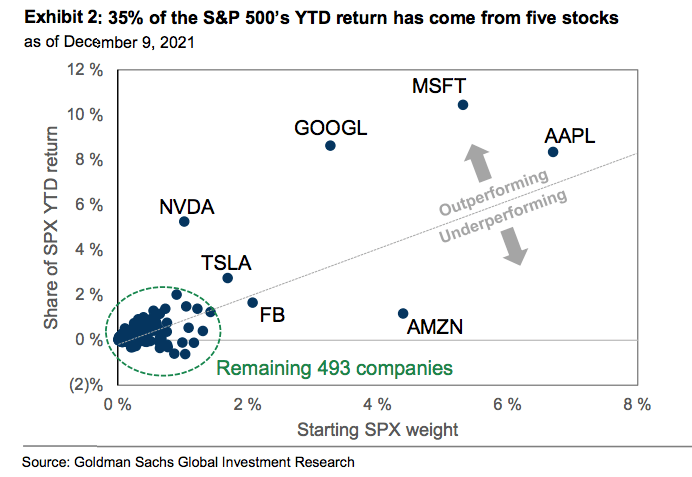

Ted: Sure. Well, I think it’s useful to look at just how extreme that dominance by the top five have been. I grabbed a couple of charts. Here’s one that shows the top stocks that have outperformed and how much they’ve outperformed and also their share of the S&P 500’s return this year.

One of the biggest ones is actually a stock that we hold in The Bauman Letter … and I’ll give you a freebie. It’s Microsoft. Look at that. When you have a stock that big that’s outperforming that much, and it has that much weight in the index…

But look at the bottom left corner. That’s everybody else.

Most of those stocks have had a pretty pedestrian year. The top one, if I look at it, is around 2%, but it’s been the year of these big companies.

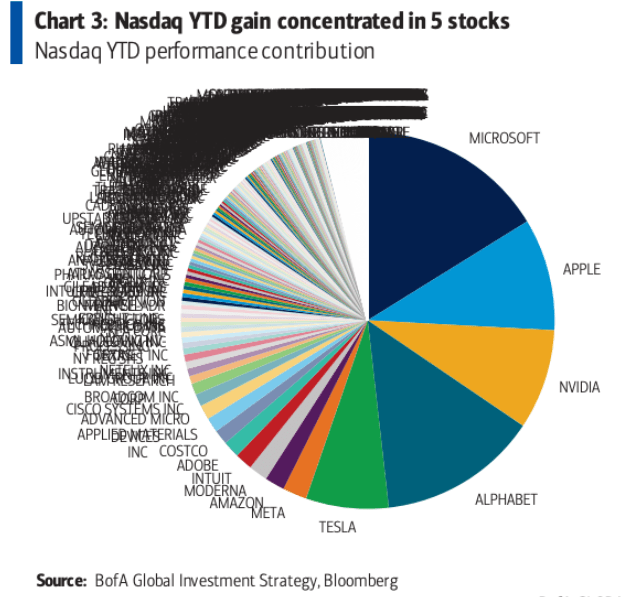

Here’s a second chart and I threw this one in there, even though it’s a God awful chart. Somebody actually did a pie chart that showed all 500, or whatever they are right now, stocks in the S&P 500, by their weight. By the time you get down to the small ones, it looks like an ant farm.

But basically that’s the stocks that have driven the market this year. And the reason that’s important, I think, is for two reasons: one is that people keep asking, why is the index looking good? Why are specific stocks not doing well?

There’s your answer. The specific stocks are in the ant farm. They’re in that little messy bit there or they’re in that little cluster in the first graph.

Unless you’re going to buy an index fund, this is why we’ve had such a hard time with the smaller stocks this year.

Having said that though, there are questions even for the big stocks as to what would happen if the Fed started to withdraw liquidity from the market. That’s not a direct thing. It’s not like the Fed prints money and then it goes straight out to buy money on the stock or stocks in the stock market. To the extent that it makes other things less attractive, it’s helped this whole process, particularly the big ones, because the big ones… Something that I think a lot of people forget, low interest rates mean these big guys had extremely low costs of capital and that gives them the ability to expand either organically or through acquisitions in ways that nobody smaller than them can do. All that comes into question now.

Angela: All right. Now, Clint, if we could talk about this market breadth a little bit, because as far as I know, when you have a really good market breath and that it’s spread out among a bunch of different stocks. That means you’ve got a high quality market, but it’s not exactly what we’re seeing now. So can we just talk a little bit more about that market breadth?

Clint: I mean, we’ve talked about breadth a lot this year and for good reason and I think really since with what’s transpired in the market since late November, it’s something to pay very close attention to right here.

I wanted to just highlight breadth is a catch-all term. There’s a lot of different ways to measure it, to describe it and to monitor it. And so I wanted to go into a few of the things that we’re watching to monitor it, the warning signs to look for, but why it can also be a little bit deceiving as well.

The first key point is that, look we’ve talked a lot about high quality this year and you just mentioned the quality advance. That’s really what it comes down to when you’re measuring stock market participation.

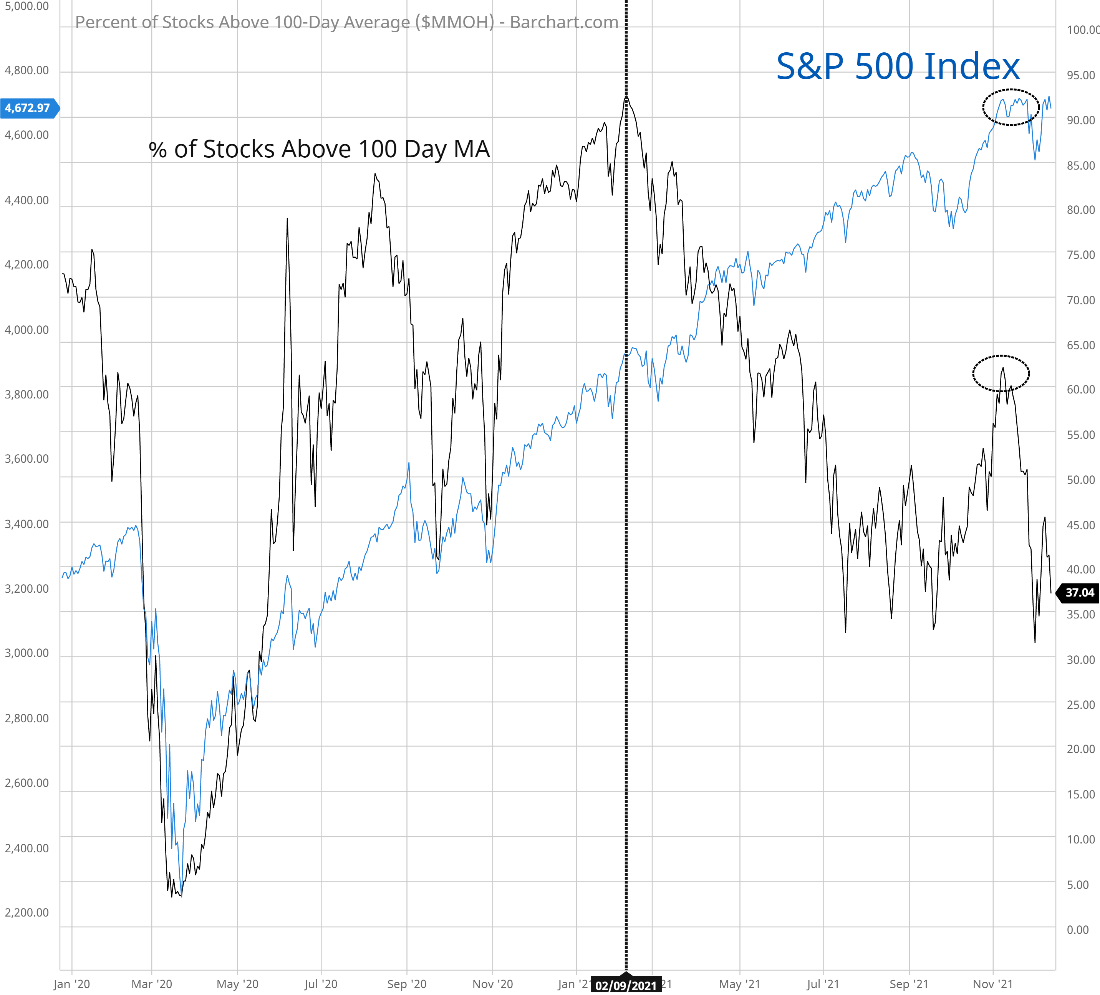

A high-quality advance is one where you see across the board stocks moving higher when you’re in an uptrend and vice versa. So the first chart I want to start with really shows a tale of two different markets coming out of the pandemic, coming out of the bare market when the stock market sold off in early 2020 in the pandemic. So that’s where we’re going to start with this chart and then this goes all the way through their current day and there’s a couple things on here.

The blue lines, the S&P 500 itself corresponding to the scale on the left, this black line. This is a percent of stocks above a 100-day moving average. Now the 50-day moving average or the 200-day moving average, they get a lot of attention.

I like to monitor the 100-day moving average. It’s just a good intermediate measure for what’s going on with the market’s breadth and really this tale of two markets. I drew a line on here to show you these two different periods.

So coming out of the pandemic up until where this line exists, it’s about February 2021. You can see on this point when the S&P was making new highs at this time. This measure was running over 90%. Now that’s actually abnormally strong, but that’s just a sign of how broad based the markets gains were at this point in time, but look at what’s happened since then. You’ve continued to see the S&P 500 march steadily higher, while this gauge has just kept on moving lower. At one point we were making new highs on the S&P and this metric was only at 50%.

Most recently when we were at new highs, this only recovered to about 60%. So it just goes to show you underneath the hood, versus what we were seeing earlier this year and how it’s deteriorated. This is one way to measure it. Another way is to look at new highs and new lows, and there’s a couple ways to use that.

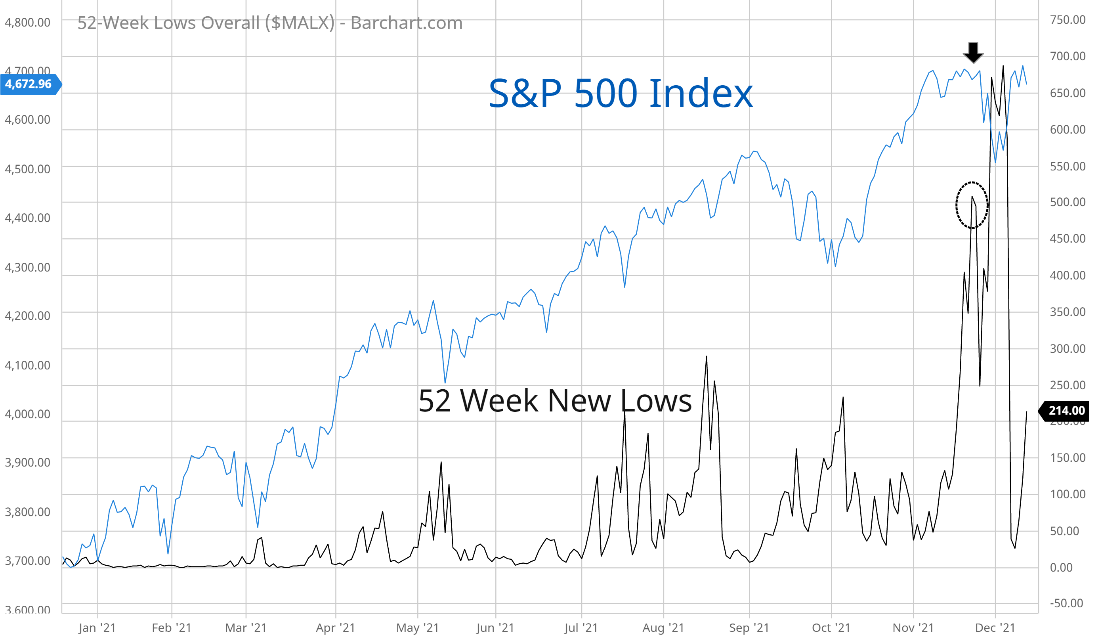

One sign you don’t want to see is a growing number of new highs in the stock market and a growing number of new lows at the same time. That tells you something bad is going on. What you also don’t want to see, is as the market’s advancing, you want to see new highs expand. You don’t want to see new lows expand, and that’s what we’ve seen this year.

So here’s a chart, the S&P 500. This is year to date with 52 week new lows.

Now this isn’t just new lows in the S&P 500 index. This is across the market, because once again, we’re trying to measure not just in the S&P but across the market, how things look. You can see as the year went on, as the S&P was moving higher, you start seeing these new lows keep expanding.

This black line on here, corresponds to the scale on the right, and it keeps moving higher. You get to the point to where I’ve got the arrow drawn on the S&P 500 when we were hitting these highs on the year and look at the circle at how much the 52 week new lows grew despite the market being at high.

This goes to show you how broad based it is with how many stocks are struggling underneath the hood right now.

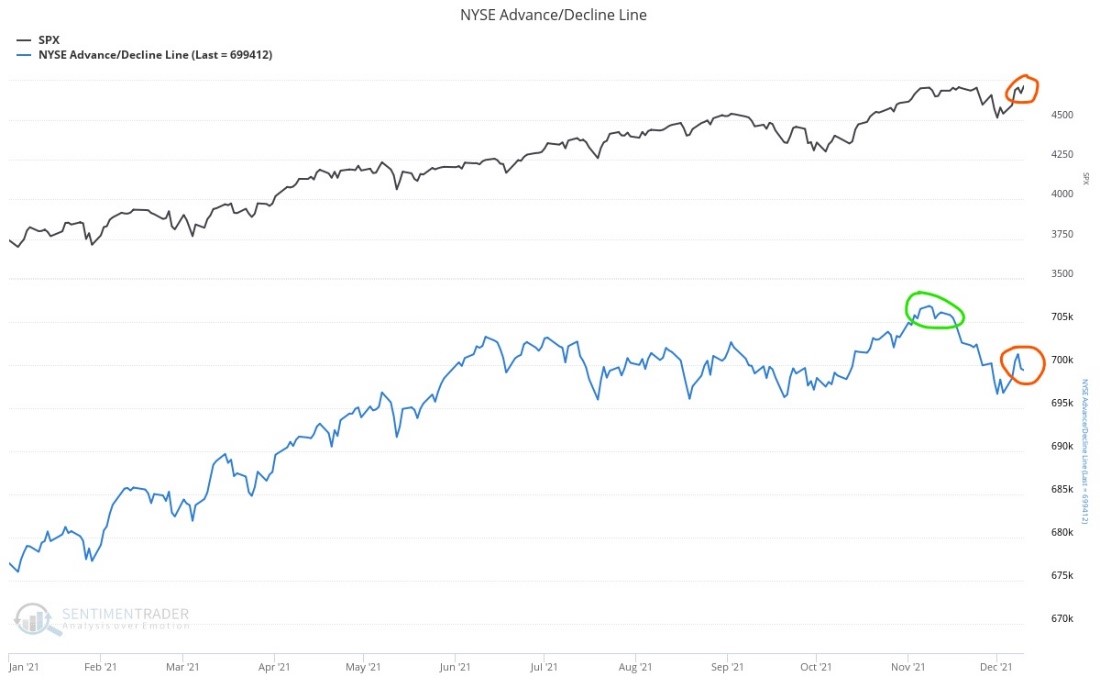

Now the last metric, I want to show something else that I track closely and I think you’re probably going to start to hear a lot more in the news … is with something called the advanced decline line. Specifically it’s for the New York Stock Exchange, the advanced decline line. All this does is it looks each day at how many stocks are advancing versus declining. Takes the difference between the two and then adds it to the prior day.

When you start this going back, you keep this cumulative running total, and it’s just a way to represent what the average stock is doing.

Here’s how that line looks relative to the S&P this year, this is a year to date chart. The S&P’s the black line on top and this blue line is that advanced decline line on the bottom.

What you want to see is this AD line leading the way, or at least keeping up with the index, and you had that with where I circled in green on here. Just going into November, small caps were doing really well. The S&P moved out to new highs, and this blue line was confirming that.

Most recently, where I circled in orange, you got the S&P rebounding after this dip, but this AD line is going anywhere. I think people are going to start to pay close attention to that. Does that mean that the bubble’s bursting while deteriorating breath like this can actually go on for quite some time, if before you start to see really the big indexes, like the S&P 500 rollover, and that’s the last chart I want to show in here.

So same thing, S&P versus the advanced decline line, but this goes back to the last big valuation bubble. The dot.com bubble. What you can see is that the S&P from January, 1998, through early 2000, the S&P kept grinding higher. Meanwhile, this blue line was just collapsing.

So you can have breadth, continue to look very bad, to be very poor yet, as Ted’s pointing out with the big stocks and the S&P driving the market… That can last for quite some time, as the tech bubble showed us.

Angela: Ted, what do you see happening here? Any warnings for us?

Ted: It’s difficult to extrapolate directly from history, but I think the critical thing is Clint’s pointing out is that it’s like Jenga. You’re taking pieces away, all those stocks that are declining as opposed to rising, but the tower is still there. And eventually you pull out one that makes the tower collapse. Now I’m not necessarily saying that’s going to happen right away. As Clint pointed out, you can get a long slide, the history of the dot.com bust. Which a lot of investors weren’t around for at this point. A lot of current investors didn’t experience that … that you’ve got this stuff moving under the hood, and yet people were still bullish, bullish, bullish, and then eventually it did all collapse and when it did, it collapsed quickly.

Now, the thing, I think the backdrop right now is that ever since the great financial crisis and the Fed started with this mega QE, joining the bank of Japan that had already been doing it and then the European central bank doing it. What’s happened is that we’ve got to a situation where it’s very difficult to know what the actual market clearing price of a lot of critical assets are. In other words, because the reference point, which is bonds and the return on bonds, has been artificially suppressed, people have been bidding things up way beyond what they would do under, quote-on-quote, normal positions.

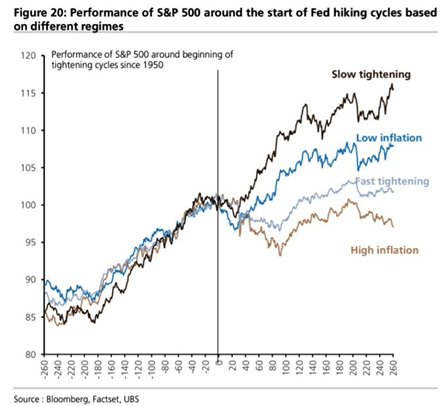

So the big question is, what happens now that the Fed tightens? Here’s a chart that shows what tends to happen with the S&P 500 when the Fed starts a hiking cycle.

I think I showed this a couple of weeks back, and basically since 1950, the best scenario is if the Fed tightens slowly. Which is, I think, what the market is looking at right now. They’re basically saying if the Fed tightens, it’s not going to happen all at once. Unless some bizarre scenario happens, which we’re not expecting. But the other thing is that when you have high inflation, which is the other problem we have right now … slow tightening plus high inflation would put us somewhere in the middle of that, which means that after a pretty big run up, you would probably see a much flatter market going forward. Which means that you can’t expect the big gains that you’ve had in the past or else, if you do, you’re going to find them elsewhere and that’s something that I wanted to talk about in particular. And I’ll come to that in a minute…

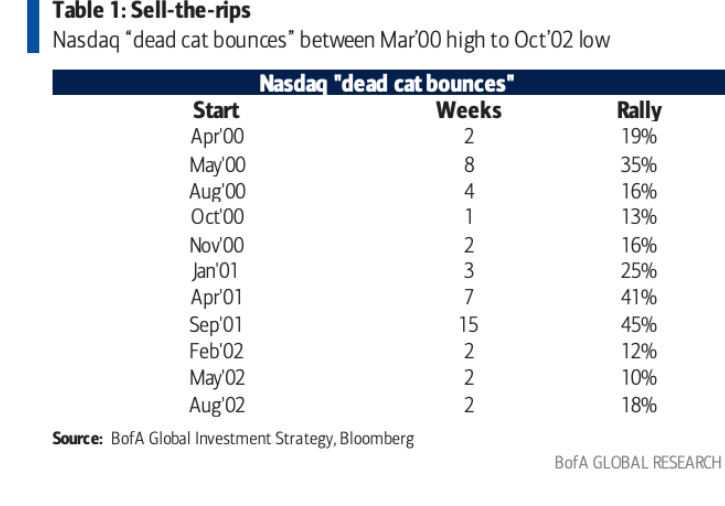

But one of the things to watch out for, and this happened during the dot.com bust, was that you had a lot of dead cat bounces. Here’s a chart that shows rallies between the March 2000 high and the October 2000 low.

What that means is that the market fell significantly from March to October. But look at some of the rallies and some of those rallies lasted for a while, but then they collapsed again. It’s really difficult to tell whether a rally is going to be sustainable or not. And that’s probably going to cause a lot of difficulties for investors, but here’s the critical thing. What’s the rally based on? In the dot.com era, it was based on the notion that these stocks were going to actually do things. And people went back to their initial thesis and they convinced themselves that everything was going to be okay and so they started buying back in again, and so you had these rallies.

Right now, it’s all interest-rate based and right now we have so many high, multiple stocks that have thin or unpredictable or no profits at all. Those stocks have to derate. In other words, they have to come down to lower multiples and if you’re not earning profits, there’s no way to compensate for multiple compression.

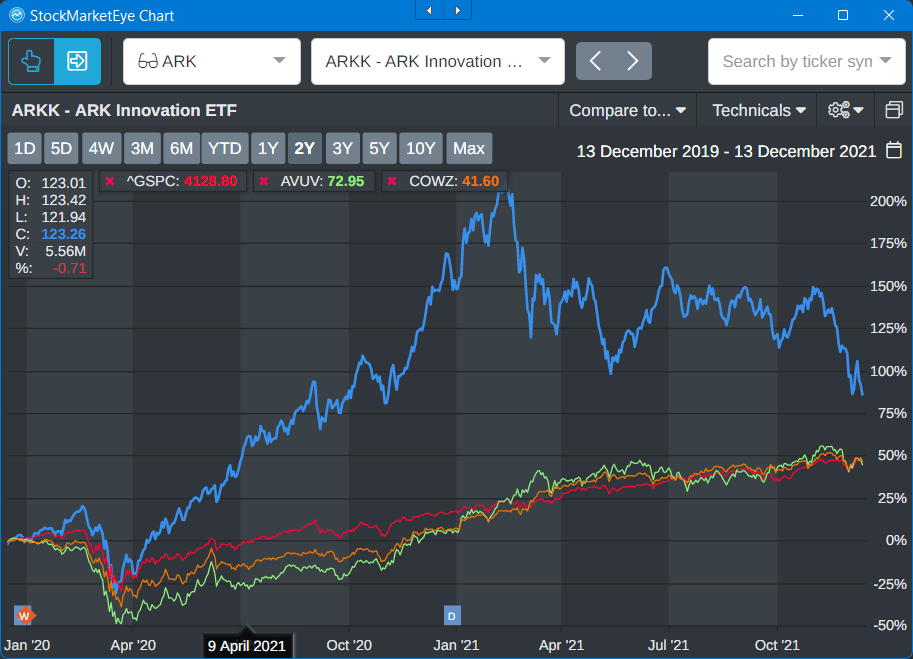

There’s a guy who writes in to me a lot on The Bauman Letter. I always appreciate hearing from him and he’s always criticizing me for not being bullish on Cathie Wood and her ARKK stuff. I’m sure he is going to write into me again after this video, but I just wanted to show you, this is his thesis right here.

Here’s the first chart.

He starts back in January 20 and says, “Look at that.” Geez, you’re up, look how much more you’re up than the market. And I’ve also included a couple of ETFs in there that I’m going to come back to in a moment.

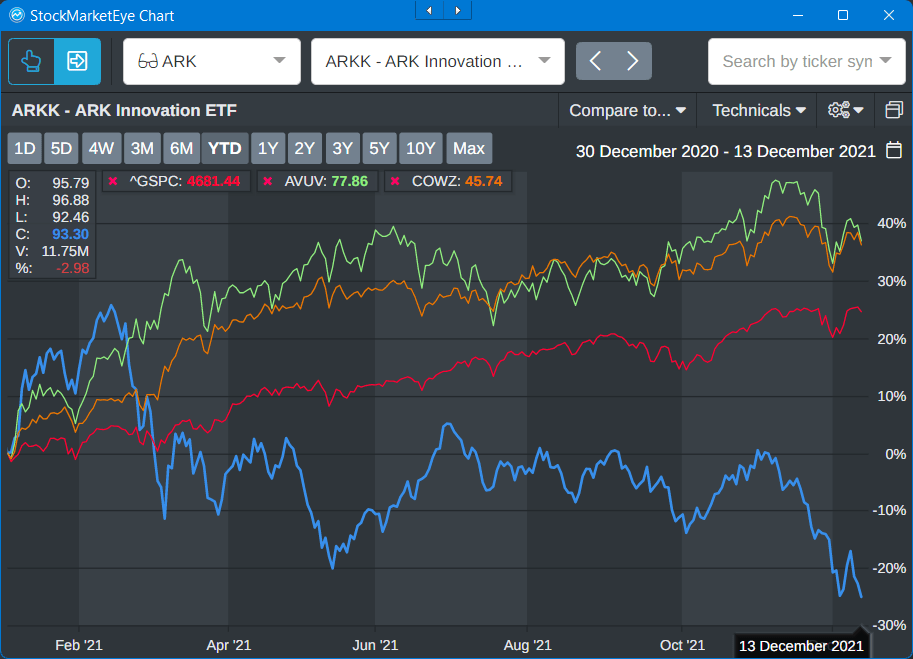

Now here’s my take. This is the same performance, but since the beginning of this year.

Okay, so the blue line is ARKK. That’s basically all the next generation stuff. The red line is the S&P 500, the green line is actually a small cap, quality stocks and growth stocks. These are small cap stocks that are earning good money and growing quickly, they’re not growth stocks that are not earning money. Look how they’ve outperformed, not just the market, but these future oriented stocks.

So it’s great. If you bought them two years ago, you’re still up, but look how much you would’ve lost if you bought them in January.

The orange line on the other hand is what they call cash cows. That’s why it’s called C-O-W-Z. And it’s an ETF that holds companies that produce a lot of free cash flow. The critical thing is now that we’re looking at a scenario where people are starting to price in Fed rolling back QE … And of course today we’re risk off because there’s bad news about Corona, and Omicron, but that’s just noise at this point, because nobody knows anything. The key thing is that the Fed starts to pull back on this money. These stocks are going to derate and you’re going to want to look at other kinds of stocks that have much more defensive characteristics.

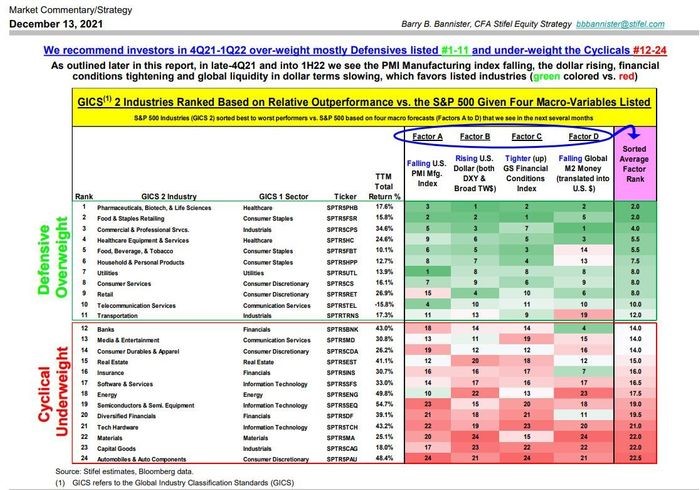

Here’s a chart that, kind of complex, but I found it this morning and it shows industries that are likely to do well given various scenarios.

So if you get slowing in the economy, that’s the producer manufacturing index. If the dollar is getting stronger, if you get tighter financial conditions, which is the Fed of pulling back on QE and a folding global money supply, then this is what this model thinks is going to happen.

This comes from Stifel, an analyst house. And basically what they’re saying is, you want to be in defensives. You want to be in pharmaceuticals, foods and staples, commercial, and professional services, healthcare. Basically this stuff that people need constantly. On the other hand, capital goods, materials, tech, financials, automobiles, semiconductors, that stuff might not do so well. The critical thing though is within each of these sectors, they’re going to be some companies that are going to be doing well because of their unique characteristic, which means you’re going to have to look hard for them, which is what we do.

Angela: That’s exactly what we do at The Bauman Letter. Funny, you should mention that.

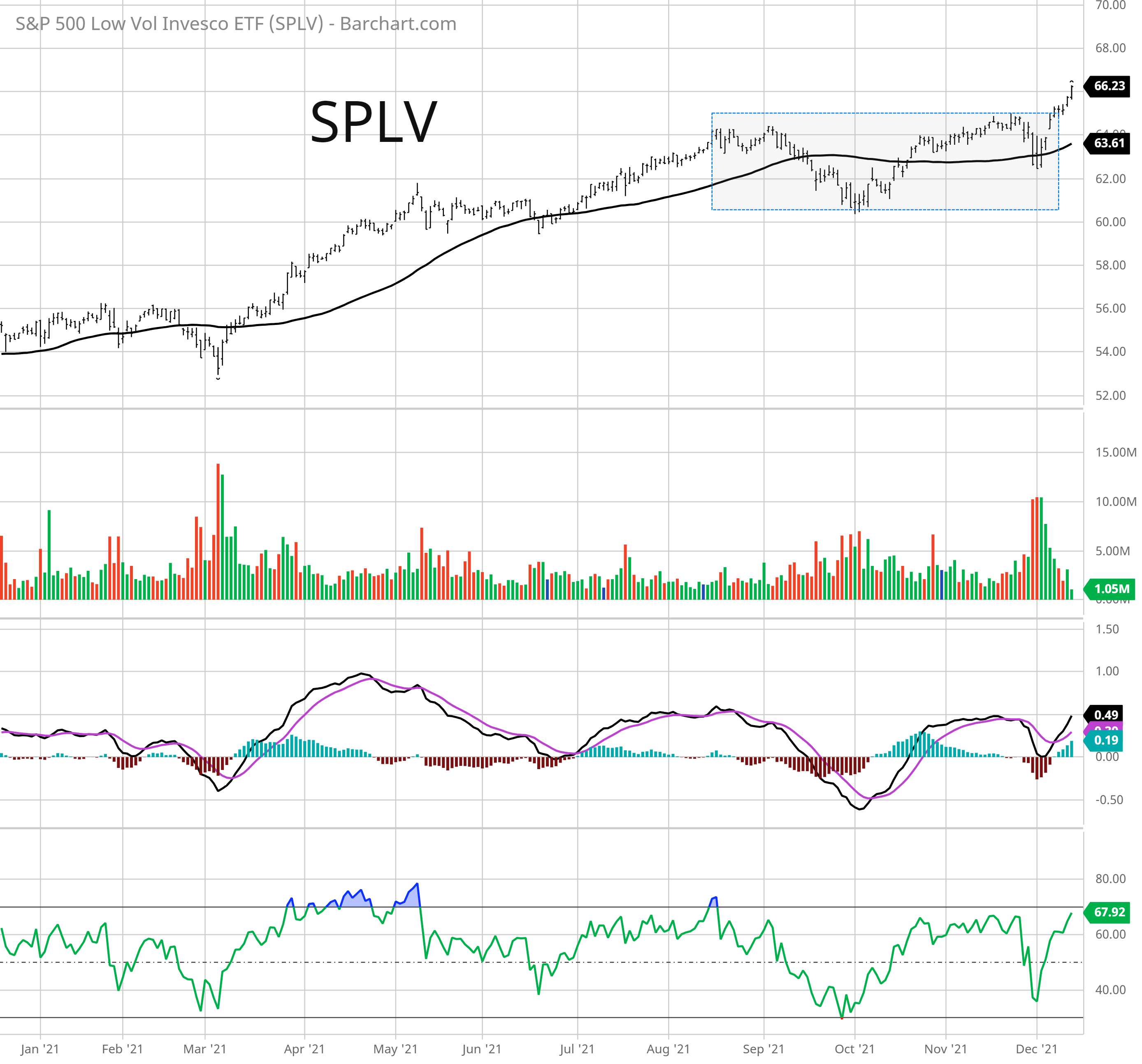

Clint: Just really quick. One ETF to play some of the themes that you’re talking about, Ted, especially on the defensive side is with SPLV. It’s an Invesco, low volatility ETF. It’s simply looks over the past year at the 100 stocks and the S&P 500 with the lowest realized volatility in their share price.

Why do they have that low vol? It could be any number of reasons, whether it’s the stability of their end markets or maybe they have a good moat and they operate high margin businesses, whatever the case may be. But over 50% of that ETF is in those defensive sectors.

And just really quick, here’s a chart of SPLV over the past year.

Despite some of the weakness that we’re seeing in various areas of the market, this is one area that’s been holding up and has actually been breaking out to new highs here. You can see this recent move over that $65 level here was key for SPLV. So that’s one holding those types of companies that are starting to benefit in this uncertain environment.

Angela: All right. Ted, as you mentioned, The Bauman Letter, it’s always a great solution for everyone watching.

Ted: We’re aiming for companies that have guaranteed revenues right now at this point. And I think that’s the thing to do. So our last couple of picks have been companies that are leaning into really strong demand growth, for a variety of reasons. We’re doing that again this month with something that is really one of the biggest boosters of demand for this particular company that’s come along in the last 50 years.

So go where the money is, and that’s what we’re doing.

And remember stocks go up for all kinds of reasons, but in the long run, they go up when they earn a lot of money … so that’s why we’re favoring those kinds of companies.

Good investing,

Angela Jirau

Publisher, The Bauman Letter