Are you still retiring this year?

I’ve learned this can be a sensitive question after a heavy stock market decline.

Stock market volatility can build a fortune … or destroy hard-earned wealth in the blink of an eye. It all depends on how you react to it.

In order to profit from the market’s volatility, an investor must be nimble and separate themselves from emotional and cognitive biases.

The buy-and-hold mantra is a common fallacy I’ve witnessed among many investors as I’ve grown in this industry.

Market timing and active management have been wrongly associated with speculation, which has led to investors missing huge gains — or even worse, losing a sizeable chunk of their wealth.

The Risk of Buy and Hold

Watching your portfolio value dwindle away during a market downturn is a feeling that can’t be replicated.

Although U.S. stock market crashes have historically been followed by rebounds, the inherent risk of buy and hold remains.

It is estimated that 75% of the stock market is owned by investors over the age of 55.

Many of these investors don’t have the ability to sit back and wait for their portfolio value to recover, if it does at all.

For those approaching retirement, a large portfolio drawdown can sabotage their retirement —sometimes delaying it indefinitely.

For those already in retirement, living and medical expenses don’t disappear. That means investments have to be sold at inopportune times.

Is Your Retirement Plan Safe?

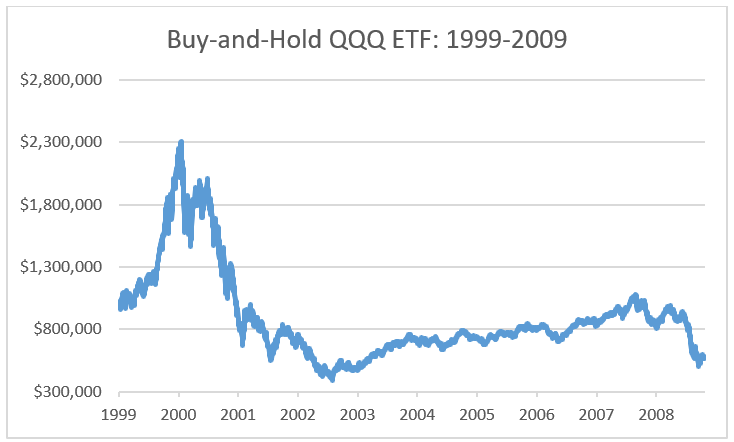

Consider a 10-year example in which someone invested $1 million in the Nasdaq Composite Index by buying the PowerShares QQQ Trust (Nasdaq: QQQ) at the beginning of 1999.

The investor quickly saw the portfolio increase to $2.3 million by March 2000, which prompted the thought: I’ll retire in a year.

As it turned out, the market crashed and the portfolio dropped to $600,000 in a year in a half, wiping out the investor’s retirement plan:

(Source: Bloomberg)

The investor continued to put off retirement while holding the same investment. After 10 years of holding, the portfolio was still below $600,000, over a 40% loss from where it began.

After nearly 10 years of pushing it back, the investor was forced to retire and liquidate the portfolio for expenses. As a result, millions of dollars of wealth was destroyed.

I bring this up not to scare you, but to show you that there is something better.

Michael Carr’s Strike Zone

My colleague Michael Carr figured out how to navigate the stock market and make money when it goes up and down.

In order to do this, he created a proprietary indicator he calls the “Strike Zone.”

His strategy completely contradicts the buy-and-hold ideology. Cash is conserved until the Strike Zone is signaled, and at that time a trade is placed.

This strategy offers huge upside potential while eliminating the risks inherent in buy-and-hold investing.

On Thursday, Michael will give a special presentation on how his Strike Zone strategy works. You can sign up for it now by clicking here.

Regards,

Research Analyst, Automatic Fortunes