Note from Charles Sizemore, Chief Editor: This week in the Banyan Edge, we’re featuring the insights of Adam O’Dell’s right-hand analyst and chief research analyst of Money & Markets, Matt Clark.

Matt’s past career as a journalist has him clued in to the political goings-on that impact our financial world. And this past week, he noticed an underreported statement from a key White House figure that could drastically reshape the banking system.

Read on to learn what Matt uncovered, and why it’s making small regional banks one of the biggest short opportunities we’ve seen since 2008…

Treasury Secretary Janet Yellen made an unnoticed statement in a talk with big bank CEOs a few weeks ago.

The former Federal Reserve chair said that more bank mergers may be necessary in order to put the current crisis behind us. (Mergers like … oh, I don’t know … JPMorgan’s acquisition of First Republic one month ago).

The executives must’ve been big fans of this endorsement. I’m sure Jamie Dimon, CEO of JPMorgan, would love the opportunity to pick up more assets for pennies on the dollar and absorb them into America’s biggest bank.

For small regional banks and lenders, it was more like getting bad news from the doctor. The Treasury Secretary suggested that less competition, fewer choices and growing monopolies in the financial industry are the best path toward stability.

Naturally, traders punished small regional banking stocks. They’ve been taking it on the chin as it is … but this report sent the SPDR S&P Regional Banking ETF (NYSE: KRE) flying down almost 2% on the day.

Any rational capitalist would agree this trend will not benefit everyday consumers. Competition is the hallmark of capitalism, after all.

Still, we also cannot deny this trend is real. Right now, we have the most powerful government in the world favoring the biggest banks getting bigger at smaller banks’ expense. That demands our attention.

There’s a lot you can do to ensure you capitalize on this trend. Let’s talk about it…

Why Bigger Is Now Better

Real quick, let’s rewind to the 2008 financial crisis.

Big banks were at the heart of the financial collapse because of their appetite for risky lending practices that caused a housing sector bubble which eventually burst.

Most of us remember how that turned out…

But there was some good that came out of it which is paying dividends today. Specifically, the Dodd-Frank Act, which the government enacted in the wake of 2008, has made it so big banks’ balance sheets are much cleaner now than they were back then. Because of that, they’re handling the current crisis well.

Funny enough, we’re now seeing the polar opposite of 2008. It’s now small banks that are the problem.

They have massive exposure to long-duration Treasurys coupled with huge exposure to the risky commercial real estate market. That sector is facing numerous headwinds right now with the rise of remote work and higher interest rates… Refinancings are coming due in the next two years while demand for office space has scarcely been lower.

The underwater Treasury exposure, and even more so commercial real estate, overwhelmingly impacts small regional banks. That imbalance is fueling the trend of “bigger is better.”

All else equal, the odds there will be fewer reputable banks in the U.S. 10 years from now is materially higher than the odds there will be more.

And two methods come to mind for investors to prepare for such a scenario:

No. 1: Focus on buying big banks. As I said, big banks don’t have much standing in their way of getting bigger right now.

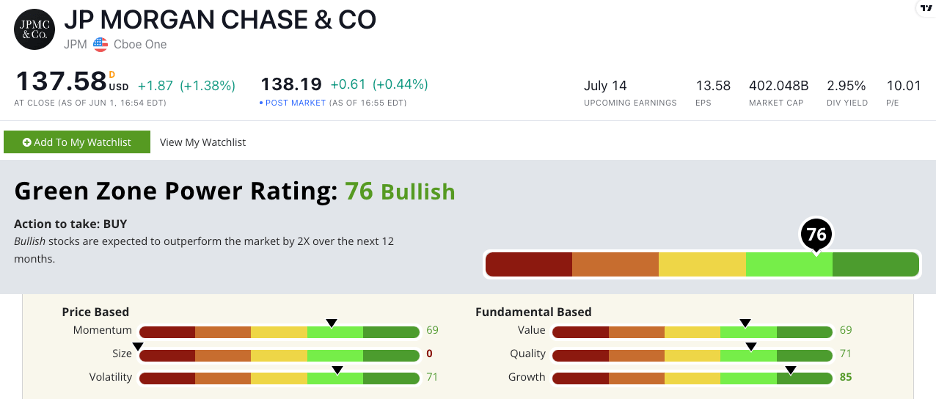

Take JPMorgan, for example. It’s the largest bank in the U.S. — commanding over $400 billion in market capitalization and holding over $2.3 trillion in deposits.

It’s the granddaddy of the banking sector. But is it a good buy?

To answer that, let’s look at Adam’s proprietary Green Zone Power Ratings system…

JPM Green Zone Power Rating in June 2023.

JPM stock throws nothing but green flags on every factor but size — which is to be expected for the $400 billion behemoth. Nonetheless, stocks that rank this well tend to outperform the market considerably over the next 12 months.

Now, JPM may well be the best big bank stock you can buy today. But, say you don’t want to buy a large-cap banking stock. I wouldn’t blame you for that. You could do fine with JPM shares … but it may take years to see significant gains.

Here’s a more short-term idea for you. One that Adam and I both believe could provide 100%, 200% and even higher gains in the months, not years, to come…

No. 2: Short regional banking stocks. The $8 billion in profitable hedge fund positions from the start of the banking crisis doesn’t lie. Right now, regional banking stocks are a toxic asset to own.

We can get a good gauge of their quality, once again, with the Green Zone Power Ratings system. While my model doesn’t track exchange-traded funds, we can look at some of the top holdings in the SPDR S&P Regional Banking ETF (NYSE: KRE) to get a sense of the weakness.

Four of the five top holdings in KRE score a 36 or worse on Adam’s ratings system. At best, we can expect these stocks to underperform the market over the next 12 months.

That means, just like the hedge funds that cleaned up over the past few months, there’s a ton of money to be made in trading against them.

To be clear, unless you’re the type who rubs elbows with hedge fund traders yourself, we don’t recommend shorting stocks over at Money & Markets. When your maximum gain is 100% in the unlikely event a stock goes to zero … and your potential risk is unlimited … the ratio just doesn’t wash out for a small everyday investor.

But what we do recommend is the method Adam O’Dell explains in detail right here.

It’s a way for you to benefit from a continued fall in regional banking shares with none of the risks that come with shorting.

You buy one specific ticker in your brokerage account and sell it once it hits your profit target. Simple as that.

Also in this link, Adam shares four financial stocks he thinks could be the “next shoe to drop” in the ongoing banking crisis.

If you have your deposits, loans or retirement assets at any of these four banks, I strongly urge you to consider your relationship with them. And if you own the stocks, they’re a no-brainer to sell today.

The prospect of less competition and more monopolizing of the financial sector is scary. Nonetheless, it is the path laid out before us.

In times of great volatility as we live in now, it’s critical that you cut past the noise and speculation and find ways to turn the tide in your favor.

Right now, buying high-quality large banks and shorting low-quality small banks is the move to make. Until that changes, that’s exactly what I’ll recommend you do as well.

Safe trading,

Matt Clark, Chief Research Analyst, Money & Markets