Article Highlights:

- Over the last 40 years, the share of income going to wage earners has declined dramatically.

- Slow economic growth is starting to influence profits … which will eventually hit stock prices.

- Instead of addressing the problem, everyone’s crying for the Federal Reserve to save them.

My relationship with capitalism has long been conflicted.

I’ve spent decades in developing countries. I’ve seen the horrific effects of poverty and economic exclusion firsthand.

Years of analysis for clients such as the World Bank and the United Nations Development Programme convinced me that much poverty was avoidable … as it was the result of political interference to tip the scales in favor of the rich.

But rather than rejecting capitalism, I concluded that as long as the game is played fairly, it’s the only game in town.

“Played fairly” means governments don’t support specific firms. They don’t prevent bad companies from failing.

And they don’t prop up distorted economies. They fix them.

So, as a possible Federal Reserve rate cut approaches — in the face of rising wages, strong consumer spending and an unemployment rate at 50-year lows — it’s a good time to ask whether the game of capitalism is being played fairly here in its spiritual home, the United States of America.

And if it isn’t, understanding why can help you protect yourself … and profit.

Playing a Rigged Game

Capitalism is supposed to work like this:

Entrepreneurs start businesses to provide things they think people will buy.

They hire people and buy materials to make those things.

If they can make and sell their products profitably, their employees and suppliers get money to spend, which fuels demand for the company’s goods.

And entrepreneurs get to keep some of that money as profit, which they can reinvest to grow their current business or start another one.

If the economy is competitive, workers earn enough money to buy the products that they and employees of other companies produce.

If the economy is competitive, capitalists earn enough profit to justify continued investment.

But eventually, competition keeps the level of profit the same for everyone. There are no “excess profits.”

Of course, this isn’t how things work in practice.

Employers try to drive down wage levels. They use political influence to weaken employees’ bargaining power and make it difficult for them to switch jobs. They strip away benefits and make jobs temporary and unstable.

They earn excess profits through market manipulation, interference with government policy and other rent-seeking stratagems.

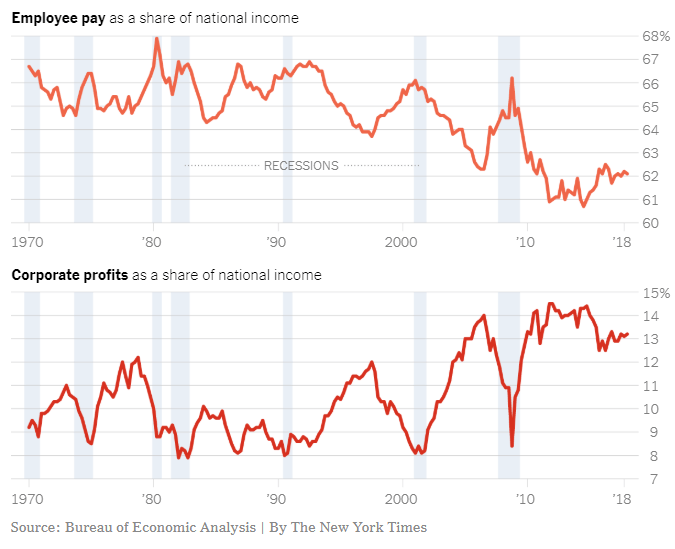

The result is that over the last 40 years or so, the share of income going to wage earners has declined dramatically. The proportion of business income going to owners of capital has skyrocketed.

The result is that, despite the rosy statistics we hear about the strength of the U.S. economy, it’s growing much more slowly than in years gone by.

And as this quarter’s earnings season shows, this is starting to influence profits … which will eventually hit stock prices.

Everybody’s waiting for somebody to come in and save capitalism for them. That’s why Wall Street is waiting anxiously for the Fed’s July rates decision.

All this has happened before.

Déjà Vu All Over Again

Many compare the 2008 global financial crisis to the Great Depression.

But a more accurate comparison is the Japanese economy during the 1990s and 2000s, when a debt-fueled bubble in asset prices burst in 1991.

Unwilling to allow Japanese banks to fail, the government propped them up. Its primary policy objective was to allow the banks and corporations to pay down their debts.

But this came at a cost to everyone else.

Between 1991 and 2007, the Japanese economy contracted by 20%. Corporate investment fell by 22%. Wages fell by 5%. Prices stagnated.

People couldn’t afford to consume the potential output of Japanese industry. Japanese businesses focused on paying down debts rather than investing.

Protected by the government, insolvent firms continued to operate. That prevented others from coming in, buying up their assets in bankruptcy and starting new businesses.

So while there were plenty of available workers and potential capital, the Japanese economy sacrificed trillions upon trillions of dollars’ worth of potential growth.

The Bank of Japan Saves the Day — Selectively

As the Japanese slump extended year after year, the Bank of Japan (BOJ) adopted radical monetary policies:

- It aggressively purchased Japanese government bonds to compensate for the loss of tax revenue and stabilize the yen. Today, the BOJ owns around 50% of Japan’s government bonds. By comparison, the Fed holds about 10% of U.S. government bonds.

- The BOJ bought Japanese stocks and corporate bonds to directly prop up insolvent companies. The BOJ now owns around 80% of shares in the country’s exchange-traded funds.

- The BOJ seeks to hold 10-year yields near 0%, overriding the free market in bonds. It was the first central bank in the world to introduce negative interest rates.

As a result of its rampant interference in the free market, the BOJ holds over $5 trillion of assets on its balance sheet. That’s more than Japan’s gross domestic product. The country’s outstanding public debt is more than five times the size of its economy.

And it was all done to protect Japanese capitalists from the consequences of their own mistakes.

I Think We’re Turning Japanese, I Really Think So

After 2008, the Western economies repeated the Japanese experience to a T.

Instead of allowing insolvent banks to fail because of their reckless lending, the U.S. government, the Fed and authorities in Europe did what the Japanese had done — focused on saving the banks from themselves.

And just like in Japan, real investment in the economy has withered away. Companies have sought returns through financial engineering tactics such as stock buybacks and financial investments rather than new investment.

That’s why, up until this year, employment growth has been tepid. Even now, wage growth remains far below the level most economists predicted.

Everyone keeps looking for inflation that never arrives … because wages just aren’t growing much.

Of course, many in the business and financial communities didn’t worry about wage stagnation. After all, it helps to prop up profits and share prices.

But now, there are concerns about profits … which could lead to a correction in the stock market.

And so, none other than BlackRock CEO Larry Fink is calling for central banks in Europe and the U.S. to buy stocks directly in order to prop up their prices … just like the Bank of Japan did.

Not the Rules We Agreed to Play By

My analysis is that the economies of the Western world are fundamentally unbalanced.

Over the last 40 years, an alliance of corporate leaders and politicians has rigged the rules to ensure that owners of capital get more than everybody else.

That means everybody else can’t afford to spend as much as they used to.

And without robust consumer demand, the financial engineering tricks that have kept U.S. profits high on paper for the last decade are starting to falter.

But instead of addressing this problem head-on — by correcting the imbalance between the returns to capital and labor — everybody’s crying for the referee, in the form of the Fed, to tweak the rules to keep the game going.

That’s not capitalism — at least, not the way I understand it.

It’s pleading for special treatment for some at the expense of others.

If you rely on the general level of stock prices to grow your wealth, eventually the game is going to break down and wipe out your gains.

Unless, of course, you follow an investment service like my Bauman Letter … which is designed specifically to help identify companies that play by the rules of real capitalism: Make things people want, sell them for a profit and reap the rewards.

After all, anything else is just plain cheating.

Kind regards,

Ted Bauman

Editor, The Bauman Letter