Now that the Federal Reserve has hiked interest rates by 4.5% since early 2022, taking them to its highest level in 13 years…

Everyone I talk to these days asks: “Should I just buy bonds now?”

Short answer … not really.

Longer answer … not really, because buying bonds still won’t make you money.

Look, I get why everyone’s considering bonds right now, especially the “risk-free” Treasury bonds and bills. Prices are down and yields are up.

But Treasury yields are still below the rate of inflation. Buying Treasurys may be better than keeping your money at the bank, but that doesn’t mean it’s protecting your purchasing power.

You can’t forget that the point of income investing is to generate income. When you lock yourself in to a negative real return, you’re not doing that. You’re losing income.

That’s why I’ve been telling everyone I know to consider high-quality dividend stocks instead of Treasurys.

The income you can get from them is both more robust to high inflation, and further interest rate increases, than bonds. Many quality dividend-paying stocks offer yields well above the rate of inflation.

But the kicker to owning these assets is they offer even more upside through capital gains.

With a volatile stock market, plenty are eager to question me on that.

So today, I’ll continue to make the case against parking your money in Treasury bonds — even at the highest yields we’ve seen in quite some time.

I’ll also share one stock from my Green Zone Fortunes portfolio that’s stable, offers an enticing yield and is primed for growth all at once.

The Limitations of Bond Investing

While discussing why I prefer dividend-paying stocks over bonds, a colleague recently asked me: “Why would I buy a stock, when I could get all the ‘legal protections’ bonds offer?”

He was pointing to the fact that when you buy a bond, the issuer is legally obligated to make agreed-upon interest payments and also give you your principal back at maturity. He’s right about that.

It’s also true that when a company goes bankrupt, whatever assets can be sold for cash are used to pay bondholders first. Equity investors only get paid if there’s anything left after that.

These are attractive qualities … especially during a bear market.

But there’s a reason I’ve been busy building a portfolio of strong dividend-paying stocks for my Green Zone Fortunes readers … and recommending zero bonds.

And that reason comes down to adaptive investing.

Adaptive investing is the core of what I do. It allows me to adjust for changes in the macroeconomic picture.

Stocks are great for this flexibility. Bonds, on the other hand, are not.

When you buy a 30-year Treasury bond with a 3.8% yield — that’s what you get … 3.8% a year for 30 years.

Those terms simply can’t adapt to long periods of high inflation. If inflation stays above 3.8%, you’re locked into a negative real yield and your purchasing power erodes over time.

Not to mention, selling a bond before maturity often carries a penalty that can erode your wealth even further.

Meanwhile, a high-quality dividend-paying stock presents none of these issues.

Companies, unlike bonds, can adapt in a world of sustained higher prices. It can pass along higher input costs to its customers, who adjust to paying higher prices over time.

In turn, the high-quality company maintains its profit margin and keeps generating earnings and cash flows. It keeps paying, and in many cases raises, its dividend for shareholders (more on that in a minute.)

Then there’s interest rates…

The relationship between a bond’s price and changes in interest rates is practically set in stone: When rates go up, bond prices go down. So a bondholder is at the mercy of interest rate changes, for better or for worse.

Meanwhile, higher interest rates don’t necessarily hurt the prospects of high-quality companies.

When a company holds little debt, or has its debt locked in at low rates for many years … higher interest rates don’t affect it all that much.

And if the company’s customers continue to show strong demand for its product, they’ll buy just as much in a high-rates environment.

And this is the biggest way dividend-paying stocks benefit: growth.

High-quality companies tend to grow their revenues, earnings and cash flows over time. If management is shareholder-friendly, it will also increase the dividend.

A bondholder in Company ABC will get the exact same income payment each year … while shareholders of the same company may get $1 per share in Year One, $1.20 in Year Two, $1.44 in Year Three … and so on.

That’s dividend growth, which is sweet on its own. But even sweeter is the fact that stocks can give you capital gains.

Yes, a bond’s price will increase if interest rates go down. You can sell the bond before it matures for a profit, giving you a capital gain. But the upside potential in stocks is almost always greater than in bonds.

To prove it, let me share one stock from my Green Zone Fortunes Income Portfolio…

An Inflation-Beating Yield in a Strong Energy Stock

I don’t normally do this … but I think it’s important to illustrate the kinds of opportunities you may be passing up by focusing on Treasurys right now.

A few months back, I recommended Enterprise Product Partners (EPD) to my Green Zone Fortunes subscribers.

EPD is one of the largest and best-run energy infrastructure companies in the world. Its 50,000-plus miles of pipelines carry natural gas, LNG, crude oil and refined products. It also manages billions of cubic feet of natural gas storage capacity and 19 deep-water docks.

Basically, the company moves critical fossil fuel resources across the U.S. for various service providers. It makes about 80% of its money from fee revenue for this service.

It’s a rock-solid business that isn’t going anywhere, anytime soon. As I’ve told you many times before, demand for U.S. oil and natural gas is only accelerating. Service providers will need to keep up with that demand by using companies like EPD to serve their customers.

So EPD has an important tailwind in the form of the Super Oil Bull mega trend that I’ve been pounding the table on all this year.

But what really makes this a compelling stock to own is its dividend yield of 7.2%.

That dividend, paid quarterly, beats anything you can find in the Treasury market. And it also handily beats inflation.

You should also know that EPD is a master limited partnership. That’s a different type of corporate structure that essentially allows the company to pay zero income taxes — leaving them more cash on hand to pay out dividends.

That tracks with its dividend history. EPD has 23 years of consecutive dividend growth and counting, and hasn’t missed a dividend payment in any 1 of those 23 years.

Of course, EPD isn’t risk-free like Treasurys are. As such, you should do your own research and make sure it’s the right kind of stock for you to own.

But remember that a “risk-free” return carries its own limitations and costs. EPD offers both an inflation-beating yield and a strong business that’s set to continue delivering its yield for years to come — and capital gains along the way.

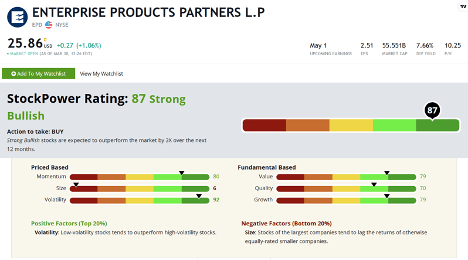

And the Stock Power Ratings system agrees, ranking it a Strong Bullish 87:

The only ding we can call out on EPD is its size. At a $55.5 billion market cap, this is not necessarily a stock you can expect a multibagger return out of.

But with that size also comes lower volatility — which is exactly what you want out of a stock with a strong yield.

Now, why would I go out on a limb and share EPD with you, especially considering it’s within the price guidance I recommend to my Green Zone Fortunes subscribers?

Because I want to give you an idea of what’s possible with income investing once you open your mind to opportunities outside of the U.S. Treasury.

And especially when you filter out only the greatest dividend stocks with my Stock Power Ratings system.

EPD is one of 17 other dividend stocks in my Green Zone Fortunes portfolio, designed to help you outpace inflation and grow your capital at the same time.

Your chief editor, Charles Sizemore, actually helped me design this portfolio a few months back. You can learn more about this project straight from Charles right here.

Regards, Adam O’DellChief Investment Strategist, Money & Markets

Adam O’DellChief Investment Strategist, Money & Markets

Fix the “Little Problems” Before They Become Big Ones

I got a cortisone injection in my right shoulder yesterday. It hasn’t really kicked in yet, and the doctor said it might take a few days. But it really can’t happen soon enough because my shoulder is throbbing, and I’m utterly miserable.

It seems that at some point over the past 20 years, I partially tore a ligament in my rotator cuff. And, like a typical man, I just ignored the occasional flare ups, assuming the pain would fade.

And it did … until the next time I lifted something too heavy. Tried to shoot too many three pointers. Or attempted to throw my now 90-pound son into the pool.

And then I was right back where I started, with an inflamed shoulder I could barely move.

After I finally went to a specialist, I got good news: I won’t need surgery. Had I seen a doctor years ago, though, my physical therapy would have been much less intensive. Time would have been on my side. But I let this drag on for too long, and my shoulder is a real mess as a result.

I tell this sob story for a reason: Managing your portfolio can be very similar.

How to Prevent Small Missteps

You will make mistakes, and things will break. It’s inevitable, and it happens to every investor. But if you correct your problems early, you can limit the damage.

Stop losses (and risk management in general) are a great solution here. Implementing a stop loss on a position will allow you to minimize risk and set a price at the beginning — on what you’re willing to lose in a trade.

You can recover from a 10% loss a lot faster than a 50% loss.

But risk management goes a lot deeper.

Consider your investment style. Perhaps you’re making decent money, but because of a few inefficiencies in your trading, you’re earning a few percent less than what you could be making.

In a single year, it really doesn’t matter. Making 5% versus 7% isn’t going to radically change your life. But over a 30-year window, it matters.

For example: $1,000 invested at 5% over 30 years grows to $4,321.

At a 7% rate, it grows to $7,612, a full 76% more. And again, that’s from a 2% improvement in annual returns.

This is why I’ve always loved the way Adam O’Dell trades.

He never rests on his laurels. He’s always looking to build that proverbial “better mousetrap.” And he’s gotten better at his job every year in the decade that I’ve known him.

Adam mentioned Enterprise Products, which is one of my all-time favorite income stocks. I’ve personally owned it for years, letting the quarterly distributions average me into new shares.

If you enjoy hunting for income stocks like these, I’ll send you:

- A 1 “sure thing” dividend stock play.

- A 6% “bulletproof” income stock play.

- My top three dividend booster

You’ll get these five recommendations for free with your subscription to Green Zone Fortunes.

And for even more investing resources, check out Adam’s Stock Power Ratings system at Money and Markets. It’s a free tool.

You can type in any ticker of any stock trading in the United States (and plenty trading overseas!), and it will give you a score for that stock based on its value, momentum, growth, volatility, quality and size.

Do yourself a favor and play with it over the weekend. You might find that next Enterprise Products to fund your retirement.

Regards, Charles SizemoreChief Editor, The Banyan Edge

Charles SizemoreChief Editor, The Banyan Edge