Banks face existential challenges. That’s partly due to their business model.

They take deposits, which can be withdrawn at any time. They use those deposits to make loans that are repaid over years. There’s an obvious mismatch there.

If interest rates rise, depositors might want higher rates on their deposits. If the bank won’t pay them, they’ll move their money.

That’s a problem because banks don’t keep all the deposits in cash. They use deposits to make loans. The banking system lends out about $3.18 for each dollar they hold in cash. This means banks can cover withdrawals as long as they are less than a quarter of total deposits.

If depositors all want their money back quickly, the bank won’t have the cash. This leads to failures like Silicon Valley Bank.

Bank runs were common before the Great Depression. When there were rumors of problems, depositors lined up to withdraw their cash. They knew that if they waited, the bank could run out of cash and depositors suffered losses. That’s why deposit insurance was created.

That system worked well for most of the past 90 years. But technology means bank runs are back.

You see, depositors don’t need to stand in line anymore. They have an app for that. Now, we are at risk of electronic bank runs.

The government has protected depositors in recent failures. But the next round of failures could be too big for a bailout. It could start at any moment. And the trigger will be commercial real estate.

Commercial Real Estate: A Crash as Bad as 2008

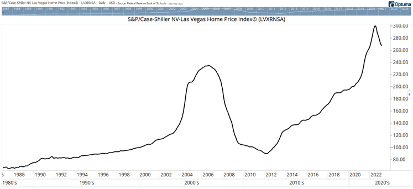

Right now, commercial real estate is positioned for a fall like the one we saw in the housing market in 2008. Home prices fell almost everywhere. But Las Vegas may have seen the worst of the decline.

The chart below shows the S&P Case-Shiller NV-Las Vegas Home Price Index. As you can see, prices fell more than 61% from their 2006 peak.

The decline was quick at first. That makes sense. As prices fell, homeowners owed much more than the home was worth. They lost hope of recovering their investment and many walked away. Defaulting, they gave the home to the bank. This led to a glut of cheap homes that banks needed to sell off.

Getting back to breakeven in home prices required a 160% gain. It takes time for a gain like that to occur. In Las Vegas, it took almost 15 years for home prices to recover their losses. That was three times longer than the decline.

Declines are sudden because all it takes is a few sales at lower prices to reset the market. When a few homes sell at lower prices, appraisers assign lower valuations to other homes. Distressed sellers need to take any price and accept low offers. This creates a doom cycle, which we see in all kinds of crashes.

Residential real estate is still in a relatively good place. But commercial real estate’s doom cycle is ready to begin. And that will be the second shoe to drop that crushes the banking sector.

Wave of Loan Defaults and Electronic Runs Will Crush Banks

According to The Wall Street Journal, a 22-story building at 350 California Street in San Francisco was worth around $300 million in 2019. That building just sold for about $65 million. That’s a 78% decline in four years.

The building is about 75% empty. On average, San Francisco offices have seen occupancy fall to about 45% since the pandemic.

The new owners will fight for new renters by charging lower rents. Rents were as much $90 per square foot in San Francisco before the pandemic. With a lower cost to service debt, the new owners could charge $45, or even less. Other owners will need to match those rates or lose clients.

As rents fall, buildings will lose value. Like in 2008, some owners will simply stop paying mortgages on the buildings. That’s bad for banks, but especially problematic for small banks.

Banks with less than $10 billion of deposits have lent an average of 40% of their assets on commercial real estate.

That’s not a problem as long as borrowers repay the loans. But if the mortgage is $300 million and the building is only worth $65 million, it makes sense for owners to walk away. That makes commercial real estate the bank’s problem.

And it’s a bigger problem to have than the one in 2008. Common sense tells us there won’t be the same demand at foreclosure auctions for office space as there was for houses. Fewer people need offices in general, and they need them less than ever before.

For the next three years, banks will be asking borrowers to refinance $270 billion worth of loans a year. Borrowers will do the math and cut their losses. Banks don’t have that option.

Depositors will also do the math. As bank problems become clear, electronic runs will become common.

I doubt the government can spend trillions supporting banks. This crisis might just be the big one that the Fed has fought so hard to prevent.

Here at The Banyan Edge, we’re keeping a finger on the pulse of the commercial real estate sector as it unravels. We’ll be watching to share with you the next big opportunity to profit from times like this.

Regards, Michael CarrEditor, One Trade

Michael CarrEditor, One Trade

Can Investing in Your Health Lower Your Tax Bill?

I have absolutely nothing new to say about the debt ceiling debacle that hasn’t already been said 1,000 times.

We’ll know soon enough whether our leaders are able to function like adults and hammer out a deal.

They will or they won’t. And there’s nothing we can do about it either way.

But while we wait for this theater of the absurd to play itself out, there are some other moves we can make to lower our tax bills.

Every dollar not paid in taxes is as good as a dollar earned in the market.

Actually, it’s better. Because that dollar earned in the market is subject to taxes!

At any rate, one of the most underutilized savings vehicles is the health savings account (HSA).

HSAs are special tax-advantaged accounts designed to help Americans pay for health expenses.

Similar to a traditional individual retirement account (IRA), contributing to an HSA account lowers your taxable income. If you are in the 24% tax bracket, you “earn” 24% in saved taxes on every dollar contributed.

When Does an HSA Make Sense?

If you have a lot of out-of-pocket health expenses, it makes sense to fund an HSA first.

Think about it. If the doctor’s bill is $100, that’s $100 gone that you’ll never see again.

But if you put that $100 in your HSA, you’ll at least get a tax break on it first.

Yes, you’re still shelling out $100. But you’ll at least get $24 back in saved taxes (assuming a 24% tax bracket.)

But even if you’re as healthy as a horse, an HSA can be a fantastic place to park cash because excess HSA funds can be invested in mutual funds or other investments.

If you’ve already maxed out your IRA or 401(k) for the year, you can turbocharge your tax-exempt savings by stuffing every penny you can into an HSA.

I call this a “spillover” IRA.

That’s not a legal term, and you’ll never see it in a financial planning pamphlet. But that’s how I personally use my own HSA account.

Once I’ve maxed out my actual retirement accounts for the year, I stuff any remaining cash into the account.

I should mention that the rules are a little different when withdrawing from an HSA.

For example, you can pull cash out of an IRA without penalty starting at age 59 and a half, whereas the age for penalty-free HSA withdrawals is a little higher at 65. But I would hardly call that a dealbreaker.

In 2023, Americans with high-deductible health insurance plans can only put up to $3,850 in an HSA plan, or $7,750 for family plans.

Now bear in mind: You can’t get rich through tax avoidance alone. You need real returns for that.

But every dollar you save in taxes is a dollar that is now available to invest, and get you closer to your financial goals.

Regards, Charles SizemoreChief Editor, The Banyan Edge

Charles SizemoreChief Editor, The Banyan Edge