Article Highlights:

- In May, the Nasdaq dropped 10% into correction territory.

- Expectations for rate cuts in 2019 have dramatically increased.

- But monetary policy isn’t a financial panacea. I explain why in today’s article.

In January, I wrote an article for Sovereign Investor Daily about the biodome.

No, not the terrible Pauly Shore movie from the ’90s.

The biodome was a science experiment performed from 1991 to 1994. Researchers created a perfect living environment in the desert for human, plant and animal life.

This clear glass dome in Arizona housed an artificial, controlled environment with purified air and water. Fertile soil and filtered light were added to simulate perfect growing conditions for plants and trees.

Humans lived in the biodome, sometimes for many months at a time. But there was one major problem…

When the trees reached a certain height, they would topple over, sometimes narrowly missing the structures built to house the humans.

That’s when an astute scientist realized they forgot to add the natural element of wind.

Healthy trees require wind to blow against them because it forces their roots to grow deeper. This supports the tree as it grows taller.

When I wrote the article back in January, I was referring to the December sell-off as the hectic “weather” the market needed to continue to new highs.

And so far this year, that thinking has been correct. The S&P 500 Index rallied 21.3% from its December lows.

However, when May arrived, the S&P 500 dipped 6.6% for the month. And volatility, as measured by the CBOE Volatility Index, surged once again.

The Nasdaq Composite Index fared even worse, dropping over 10% into correction territory.

So I wasn’t the least bit surprised when the financial media once again featured the bears on TV talking about the trade wars and rerunning segments called “Markets in Turmoil.”

But here’s why nothing has really changed…

A Broken Record of Bearish Hits

It’s been a decade since the end of the Great Financial Crisis (GFC).

In that time, I’ve watched one “scary” reason or another cause a short-term blip in the markets.

In a typical instance, the bears build a wall of worry for a few weeks or months. Then the Federal Reserve says something dovish, and the market climbs this wall of worry to new highs.

In each instance, the market became more stress-tested and grounded. It was as if the roots underpinning the rally had gotten deeper.

The past events can either be sung to the tune of Billy Joel’s “We Didn’t Start the Fire,” or you can read them like an ad for “AM Radio’s Greatest Hits of the ’70s”:

- European bond crisis.

- Flash Crash.

- Grexit.

- U.S. sequestration.

- China credit crunch.

- Government shutdown.

- Fiscal cliff.

- Russia annexes Crimea.

- Fed taper tantrum.

- Oil crash.

- Brexit.

- Trump election.

- French election.

- North Korean missiles.

- China trade war.

- Hawkish Fed.

- Mexican tariffs.

Perhaps I missed a few events. But I think you get the idea.

In the time that all of these events have happened, here’s what the stock market did:

SPDR S&P 500 ETF (NYSE: SPY) Since 2009

Each little downdraft in the market over the last 10 years was a result of an aforementioned event.

And every time one of these events hit the stock market, the Fed’s response was to add more monetary stimulus.

I don’t blame it. That’s the only thing the Fed knows how to do.

But monetary policy isn’t a financial panacea.

A Blunt Instrument

My favorite way to describe monetary policy is how former Federal Reserve Chairman Ben Bernanke referred to it: a “blunt instrument.”

The Fed eases interest rates to lift asset prices. But it’s never sure if rising stock, real estate and bond markets will have the intended impact of growing the economy.

We do know, though, that it raises asset prices.

And when investors headed for the exits in May as the S&P 500 sank 6.6% and the Nasdaq touched 10% correction territory … guess what happened?

They turned to the Fed, and expectations for rate cuts in 2019 dramatically increased.

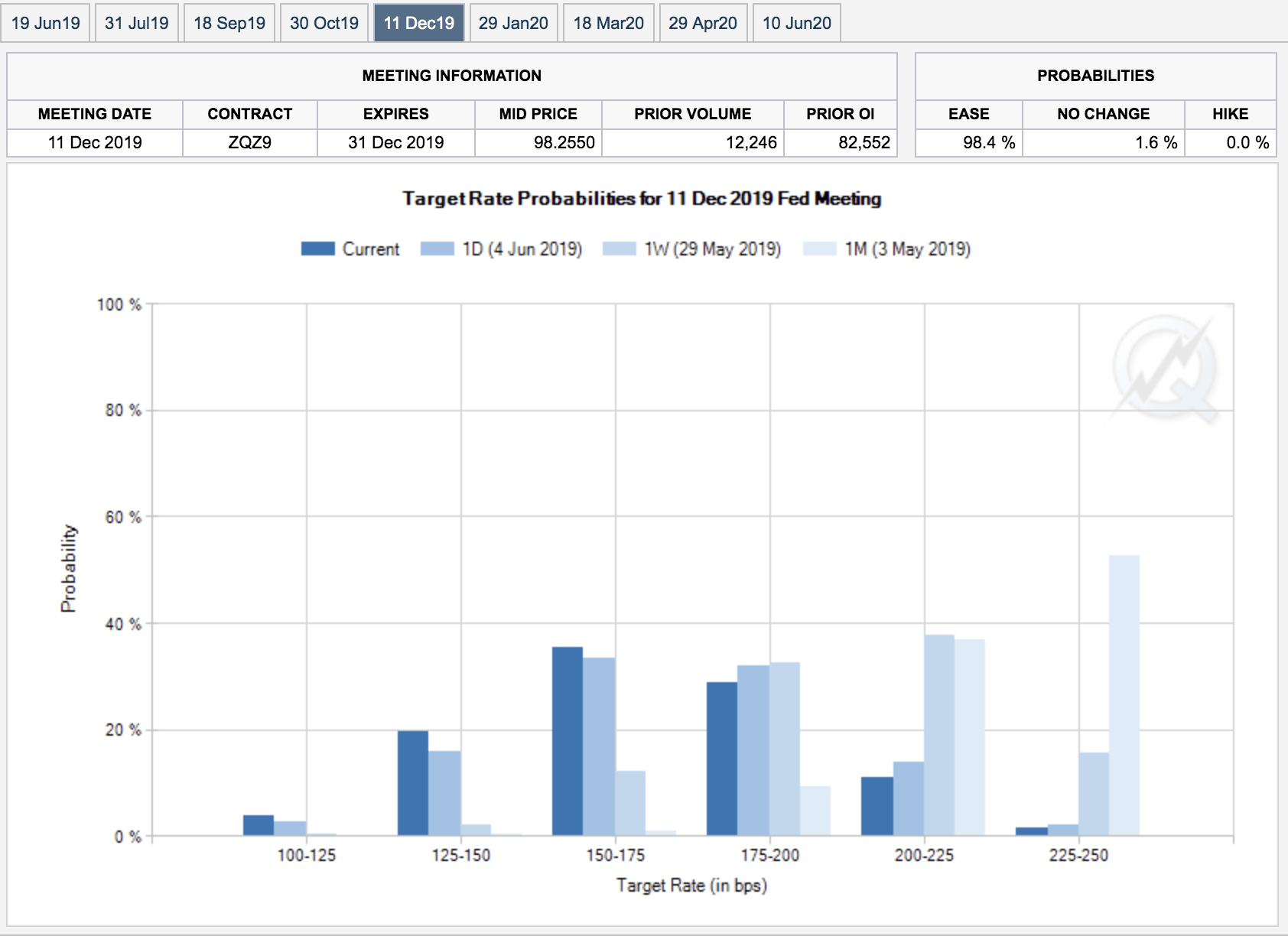

Here’s a chart of rate odds for the December 2019 Fed meeting:

Going into May, there was about a 50% chance that rates would be on hold all year (as seen in the light blue bar all the way on the right).

But the current reading shows the highest probability for 75 basis points of easing in 2019 (as you can see in the dark blue bar in the 150 to 175 basis point range).

How the Fed Restored Trust in Monetary Policy

Let me remind you, the market tells the Fed what it should be doing, not vice versa.

The Fed always listens because this is how it maintained transparency after the global financial crisis.

Its belief is that it’s better to do what the market expects rather than surprise investors, who might still be nervous another financial panic is right around the corner.

Listening to the market is what has restored trust in monetary policy.

And right now, the biggest odds in 2019 are for a 50- to 75-basis-point cut.

Fed Chairman Jerome Powell is even talking up rate cuts, saying of the recent trade disputes with China and Mexico: “We are closely monitoring the implications of these developments for the U.S. economic outlook. And, as always, we will act as appropriate to sustain the expansion, with a strong labor market and inflation near our symmetric 2% objective.”

The market is predicting it. The Fed-heads are now saying it. And we don’t live in a biodome where trees inexplicably fall down.

Something tells me the bears are going to feel another blunt instrument to the side of their heads soon.

Regards,

Ian King

Editor, Automatic Fortunes