Article Highlights:

- Big Tech companies made 1,000%-plus returns over the last decade.

- Those days are finished … but there’s a new breed of tech giants.

- Their advantages give them a “moat,” in Warren Buffett’s terms.

My best friend from high school has a business that explains my approach to stock picking.

He makes goose calls.

They’re hollow wooden tubes about nine inches long, fitted with a resonator similar to a saxophone reed. In the hands of an expert, they sound like a goose, which attracts geese … so hunters can shoot them.

My pal started making calls at school. Years later, he popped up on the TV in my hotel room in New Delhi, India, on a CNN International feature about goose calling.

Over a barbeque a year later, he said the first years were tough. He focused on perfecting his design and marketing it to local hunters and outdoor retail chains such as Dick’s and Cabela’s.

His growing reputation led to a massive increase in sales over the next few years. But he had automated, so his revenue grew faster than his production costs.

And since he had excellent relations with outdoor retailers, his marketing strategy was checking his email every day. They just kept sending bigger orders.

My friend’s business now has a huge market share, an unbeatable brand and minimal marketing and production costs.

His profits grow by double digits every year. If his company was listed, I’d buy stock in a heartbeat.

It isn’t … but you can buy companies with the same great business model if you know where to look.

Profitable Investments Have Moats

Like my friend’s goose-call business, this decade’s big growth stocks have a strong business model.

Google, Facebook, Amazon, Apple and Netflix share five things in common:

- They were the first (or an early) mover in their market.

- They developed an innovative product that addressed potentially enormous markets.

- These products were a “platform” with a natural growth dynamic — Facebook’s social connections, Google’s search engine and so on. The more market share the platforms gained, the more value users got from them … and the more difficult it was for them to switch to a competitor.

- They had deep-pocketed initial investors willing to lose billions for several years to help these companies achieve the “tipping point,” after which they became unassailable monopolies.

- It would take tens, even hundreds of billions of dollars to build up viable competitors to Amazon’s e-commerce platform or Google’s advertising monopoly. It makes more sense to invest in Amazon rather than fund a potential competitive startup.

For the Big Tech companies, these five qualities add up to a formidable competitive advantage, Berkshire Hathaway CEO Warren Buffett’s favorite corporate quality:

The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage. The products or services that have wide, sustainable moats around them are the ones that deliver rewards to investors.

In Buffett’s “moat” analogy, it takes more than a great product to get his investment — a company also needs something that protects it from competitors.

There’s an App for That

If you’d bought into one or more of the Big Tech companies a decade ago, you’d have made massive returns.

Nowadays, their price-to-earnings ratios are sky-high. They remain profitable investments, but the days of 1,000%-plus returns are over.

There’s a new breed of company that’s doing what tech giants of the last decades did … albeit in a market space most people miss.

These are cloud computing companies that provide critical management services to other companies.

Instead of having expensive and bloated in-house management systems, companies can outsource management of human resources, customer relations, supply chains, inventory and overall enterprise planning to highly specialized software hosted on remote servers.

This allows them to reduce their middle management head count by up to 80% and achieve tremendous efficiency gains at the same time.

Just as there was an app for every need when the iPhone came out, cloud computing companies are providing an app for every management function in the corporate environment.

Competitive Advantages

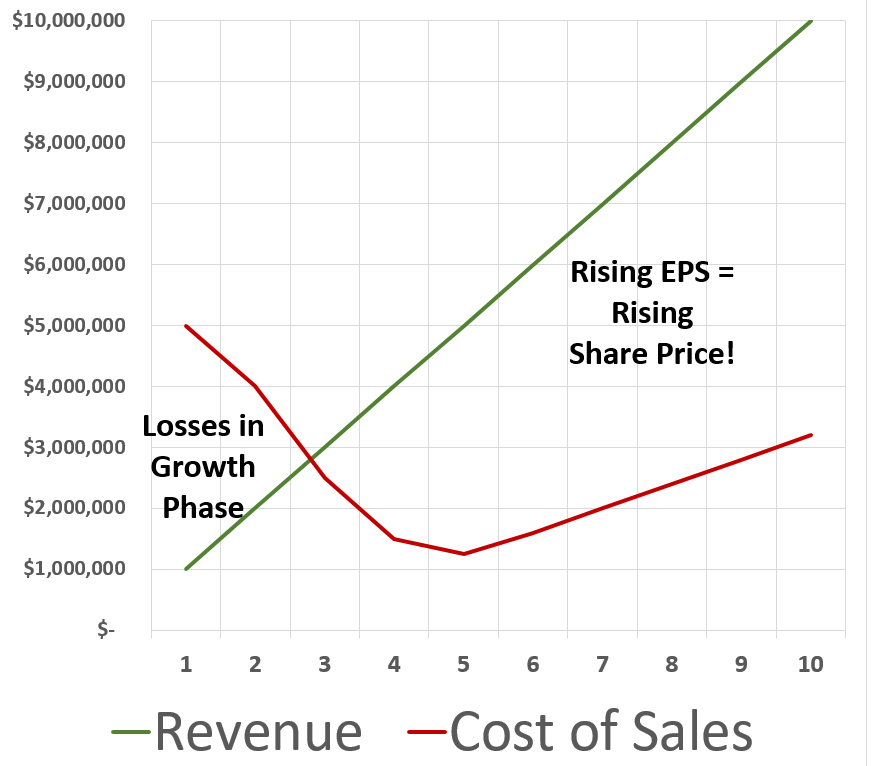

Cloud companies are characterized by low capital intensity and labor costs, rapid recovery of startup costs, lots of recurring revenue based on subscriptions and a low marginal cost of sales.

That means — after a brief period of losses as it builds its product platform — if a company is successful, it can experience runaway growth in revenue with much slower growth in costs.

And that means it experiences consistently rapid increases in earnings per share, which translates into an increasing share price. Its growth path looks like this:

Of course, not every one of these companies is a winner.

That’s why my research team and I spend hours analyzing companies that have a combination of competitive advantages that gives them a “moat,” in Warren Buffett’s terms.

We found a bunch of them, and I’m going to be talking more about them at this week’s Total Wealth Symposium in Amelia Island, Florida.

If you won’t be able to attend the event in person, you can still watch my presentation on our live-stream.

Cloud companies may not make products as simple as goose calls … but the business model is just as solid, and so are the profits.

Kind regards,

Ted Bauman

Editor, The Bauman Letter