In my final Bauman Daily video of last year, I described the stock market’s “perpetual motion machine.”

I’m convinced it’s going to be a key factor in how the market performs this year.

To see why, let’s start with a startling statistic.

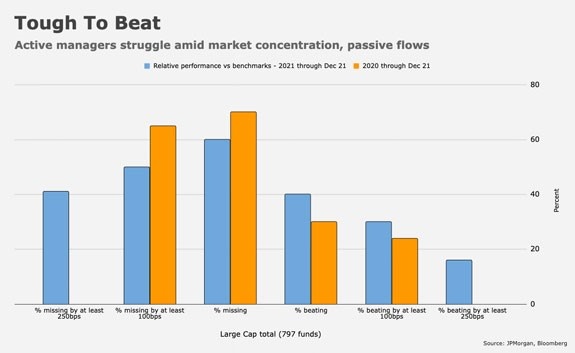

In 2021, only 40% of active fund managers beat the market. The figure was even lower for 2020:

(Click here to view larger image.)

“Active managers” are hedge and mutual funds that constantly trade in and out of stocks to outperform the market.

The opposite of active management is (you guessed it!) passive management, also known as indexing.

An index fund holds stocks from a specific segment of the market, or index. Each stock is held in exact proportion to its weight in that index.

The most common form of indexing is exchange-traded funds (ETFs). If you want to invest in the S&P 500, for example, you buy the SPDR S&P 500 ETF Trust (NYSE: SPY). As the index performs, so the fund performs.

If active managers are supposed to be so good, why do they keep underperforming the market and passive index funds?

And what could change that?

The answer will surprise you…

Chicken or Egg?

There are a couple of important differences between active and passive management.

One is that active management is more expensive. You gotta pay the talent to make all those trading decisions, after all.

Passive management is cheap. You buy whatever is in the index and adjust those holdings periodically to match their index weight. That doesn’t require any skill. That cheapness is why they’re increasingly popular.

But the biggest difference is that passive management moves markets … in the direction they’re already headed.

Take Tesla (Nasdaq: TSLA), for example. At the end of July 2021, at $699 a share, the company was 1.5% of the S&P 500. By November 30th, at $1,089, it was 2.4%.

That raises the classic chicken vs. egg question.

Something caused TSLA to rise, starting in August. As its share price increased, so did its weight in various indexes. So, managers of funds targeting those indexes had to increase their holdings of TSLA accordingly.

That buying would make Tesla’s price rise even more. And retail investors, noting that, would buy even more of the stock. And so on.

A perpetual motion machine … chickens and eggs.

Passive Becomes Aggressive

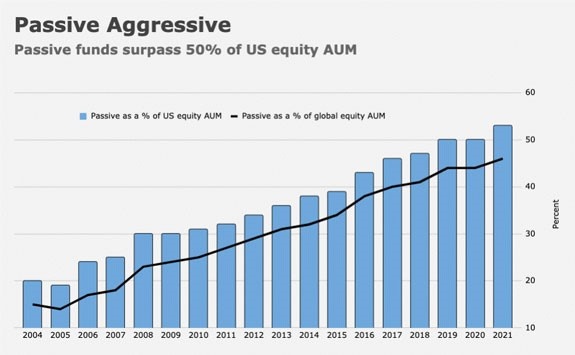

At the time of the great financial crisis, passive funds held about 30% of U.S. stocks by value.

By 2019, that figure had increased to 50%.

In 2021, for the first time in history, passive funds held most U.S. stocks by value:

(Click here to view larger image.)

This is an enormous change in market structure.

It may well be the most important development in the stock market in the last two decades.

You can think of it as a type of unintentional leverage.

Let’s say some big investors — 10% or 15% of market buying power, like hedge funds and college endowments — start to buy a particular group of stocks.

Maybe they like low volatility. Perhaps they’re looking for a pattern of earnings growth.

Most likely, they’re looking at recent momentum and chasing that … buying what’s going up.

Whatever the starting point, once that institutional buying starts, those stocks are going to rise. Automatically, that means index ETFs and mutual funds must buy them as well.

That pushes their price up even further, which leads to more buying, both by the institutions that started the trend, and by retail investors … and then, again, by the passive crowd.

The result is that that 10% to 15% of market demand ends up leveraging a bigger rise in the price of the target stocks than would be the case otherwise.

Passive Concentration

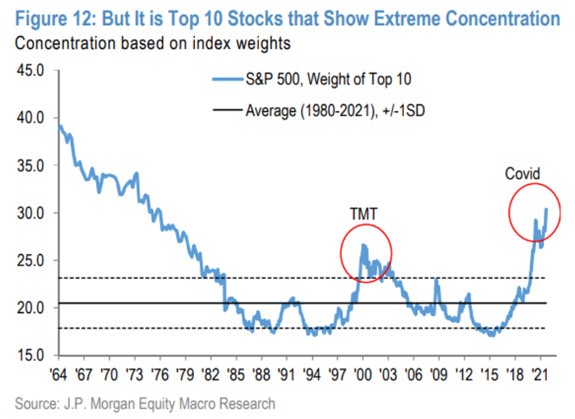

You can see the impact of the huge growth of passive index funds by comparing market concentration in the dot-com era to today.

In the last few years of the dot-com boom, a small group of market favorites enjoyed rapid gains, such as Intel, IBM, Cisco, Oracle and Microsoft.

Passive strategies helped to amplify that trend … but since they only owned around 15% of stocks by value, the “perpetual motion machine” played a much smaller role than today:

(Click here to view larger image.)

The upshot is that, as passive investing has become bigger, the leveraging effect of the perpetual motion machine has become so big that it determines the direction of the whole market.

But that effect is even more powerful when most stocks are trading sideways or declining.

If all stocks are going up, the index weight of individual tickers doesn’t necessarily change.

But if most of the market is flat, money flows out of the laggards and into those still growing. That means the perpetual motion machine’s leverage of those stocks’ prices becomes extremely powerful.

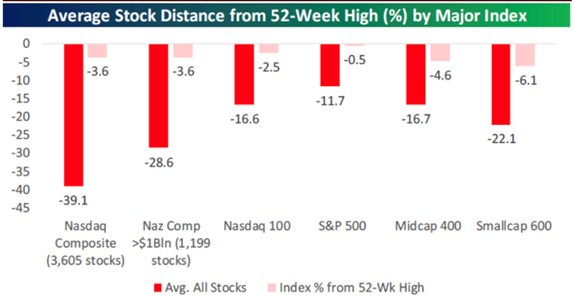

That’s exactly what we saw last year. In 2021, the average stock in every major U.S. market index saw declines of between 12% and 40% from its previous 52-week high. In the S&P 500 — on track to see annual gains of nearly 28% — the average stock is down nearly 12% from its 52-week high:

(Click here to view larger image.)

If the average stock is that far down, the only way the index can be doing better is if a small handful of firms at the very top are seeing massive outperformance. And that’s exactly what happened:

What Goes Up…

The current massive outperformance of mega cap technology stocks benefits from passive indexing’s “perpetual motion machine.” The faster these tickers rise relative to the rest of the market, the more passive funds buy them, which makes them rise even faster.

But that process also works in reverse.

If something were to sour investors on these stocks, we could see a wave of selling from index funds as they sought to keep them in balance with the rest of the index. The same leveraging effect that worked on the way up could work on the way down.

Rising interest rates … increasing regulatory pressure … an economic slowdown … whatever the origin, the perpetual motion machine would shift into reverse.

But that just means all the other stocks would start to gain.

That’s something I would certainly welcome in 2022!

Kind regards,

Ted Bauman

Editor, The Bauman Letter

{kind=link}

{kind=link}

{kind=link}

{kind=link}