Friday Four Play: The “Captain Obvious” Edition

Riddle me this, Great Ones…

If a company benefits greatly from a once-in-a-lifetime event, should you expect those benefits to continue beyond the event?

The answer, which we all know, is “No.”

No, you shouldn’t. I mean, the answer is in the question itself: “once in a lifetime.” It’s kinda spelled out right there.

Well … duh, Captain Obvious!

I know, right? But try telling that to Wall Street.

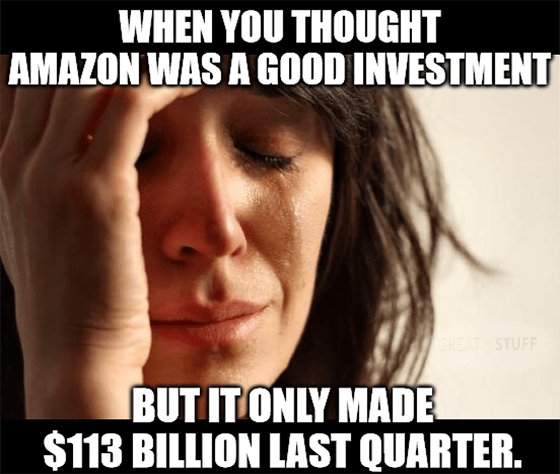

Amazon (Nasdaq: AMZN) just reported its third-consecutive $100 billion quarter, but that just wasn’t good enough. Here are official numbers for those who like that kinda thing:

- Earnings per share: $15.12 reported, $12.22 expected.

- Revenue: $113.08 billion reported, $115.06 billion expected.

- Amazon Web Services revenue: $14.81 billion reported, $14.18 billion expected.

OK, here’s the situation…

Your parents went away on a week’s vacation?

Amazon benefitted greatly from the COVID-19 pandemic, especially the lockdowns. Unable to leave their houses, consumers flocked to the world’s largest e-commerce retailer … and Amazon made bank.

Wall Street analysts piled on with bullish forecasts, presumably driven by the fact that consumers were flush with government cash.

Clearly, those estimates were set too high. As you can see, revenue missed the consensus estimate for the second quarter … even though Amazon killed it on every other measure. Prime subscribers topped 153 million at the end of June — up 25% — and advertising sales soared 87% to $7.92 billion.

The problem is that, during the second quarter, consumers started going outside again. It was bound to happen, and yet Wall Street’s estimates don’t appear to have accounted for that clear fact.

This becomes even more evident when we look at Amazon’s third-quarter guidance. For the quarter ending in September, Amazon looked at the reopening around the country and said it expects revenue of $106 billion to $112 billion on operating profit of $2.5 billion to $6 billion.

Wall Street expects revenue of $118.7 billion on earnings of $8.11 billion. Under normal circumstances, this discrepancy could indicate that Amazon faces issues that Wall Street doesn’t know about. Right now, however, analysts are more than aware of the COVID-19 pandemic.

Given that COVID-19 infection levels are practically the same as they were at this point last year —and rising — Wall Street might not be off base. Amazon might be playing the situation conservatively.

If — and that’s a big “if” — COVID-19 infections come under control and the economy continues its reopening path, Amazon is likely right on its third-quarter guidance. Lower revenue for Amazon is just par for the course as more people go outside and spend money traveling.

However, if the COVID-19 situation continues as it has for the past month … expect more lockdowns to follow the reinstituted mask mandates. And expect Amazon’s revenue to rise well above its current third-quarter forecasts if customers are forced to only shop online once again.

Right now, Great Ones, I’m leaning toward the latter scenario — the lockdown situation. There’s still way too much resistance to masks and vaccines, and that’s going to exacerbate the problem … likely for months to come.

But the good news — for investors, at least — is that AMZN’s roughly 7.5% decline today is a potential buying opportunity … well, if you can stomach buying a stock for $3,350 a share, that is.

Editor’s Note: Big Tech Is Investing In THIS

Amazon, Apple, Google and even the U.S. Army are all investing in a new tech. That’s a lot of billionaires and tech companies making the same play.

But while everyone else is betting on artificial intelligence, genomics, crypto, 5G and electric vehicles, they’re missing out on this growth industry.

Watch this video to find out what it is…

And now for something completely different! Here’s your Friday Four Play:

No. 1: Welcome To Wall Street

In its debut listing on Thursday, trading app baron Robinhood (Nasdaq: HOOD) fell 8.4% from its $38 IPO — reportedly the “worst debut session ever by a U.S. IPO of its size.”

HOOD shares gave up another 1.7% this morning but ended the session up nearly 5%.

So, what happened? According to Bloomberg: “It was supposed to be a triumph for today’s memeified markets — a validation for all those amateurs who took on the Wall Street pros.”

I mean, didn’t “David” retail investors flock to Robinhood to buy meme stocks like GameStop and AMC to take on the Wall Street “Goliath?”

Anyone who believes that steaming pile hasn’t been paying attention. But Great Ones know that the HOOD has been doomed since January. That’s when Robinhood limited and even outright blocked trading on said meme stocks. It left a very, very … very bad taste in retail investors’ mouths. Let’s add one more “very” for good measure.

Unfortunately for Robinhood, its unconventional IPO process — selling a majority of its shares to Robinhood users — relied heavily on retail investors. The same retail investors that Robinhood $#@^ed over back in January.

In a way, HOOD’s IPO was a triumph “for all those amateurs who took on the Wall Street pros.” As a top post on Reddit’s WallStreetBets forum put it: “Is it me or does anyone else get pleasure from watching Robinhood’s stock burn to the ground?”

To many retail investors, Robinhood is no longer a band of merry men taking on the establishment … it is the establishment. Robinhood is Prince John.

Now, Robinhood will likely be just fine for a while. HOOD’s price will eventually stabilize. But the company really needs its direct on-app, IPO-listing model to work to really rake in the cash. To do that, the company must regain the trust of retail investors.

And that, Great Ones, is going to be a long and bumpy road.

No. 2: Money Talks … Even In Klingon

If you happen to be an investor who likes IPOs that don’t suck, well, look no further than Duolingo (Nasdaq: DUOL).

Shares of the language-learning app company surged 36% in their debut yesterday, giving Duolingo a roughly $5 billion market cap. Take that, Robinhood!

In case you aren’t familiar, Duolingo is a language-learning app that can teach you everything from Spanish and Japanese to Swahili and, surprisingly, Klingon.

The Duolingo app is free to use, but the company makes money by charging for more intensive lessons.

The model worked well during the pandemic lockdowns, as users flocked to the app to make productive use of their downtime (at least when they downloaded the app). While the pandemic has boosted subscriber levels, cofounder Luis von Ahn believes Duolingo’s active users will remain above pre-pandemic levels once COVID-19 is gone.

Personally, I learned a little Japanese on Duolingo during the pandemic lockdowns … which I won’t embarrass myself by trying to share with you.

Anywho, Duolingo has plans to expand into children’s literacy programs as well as math lessons.

The company has solid prospects but is still in the red when it comes to earnings. In the March quarter, Duolingo said it lost $13 million on revenue of $55 million. In the same quarter last year, the company lost just $2.2 million on revenue of $28 million.

What ya gonna do? Costs gonna rise as growth continues. That’s the way the IPO do. It’s still more exciting than Robinhood, though. I mean, is Robinhood gonna teach you Navajo? I don’t think so.

No. 3: Vacuum Bots, Assemble!

Roomba if you want to — Roomba around the world.

Without wings, without wheels, vacuum robot maker iRobot (Nasdaq: IRBT) sputtered into the earnings confessional this week. You ever see a Roomba try to “clean up” pet accidents? Yeah … that’s kinda how iRobot’s report went.

OK, maybe it wasn’t that bad: Earnings still sucked for the floor-based robo-vac company, missing by about $0.04. But revenue is actually up 31% year over year, coming in at $365.6 million and beating estimates for $355.1 million.

Considering iRobot can hardly fulfill orders right now … this ain’t too shabby.

But then iRobot brought some extra negativity to the conversation, and Wall Street did not appreciate the buzzkill (see also: Amazon). iRobot considerably lowered its earnings and revenue guidance for the full year, on account of everyone’s favorite chip shortage.

iRobot’s setbacks are no mystery: The company is still heavily reliant on Chinese manufacturing for basically all of its operations. That lack of supply chain diversity dampens iRobot’s ability to fulfill orders, and the company is just now “qualifying new alternative suppliers.”

IRBT investors out there, I’m not going to dress it up: Outside of the revenue growth, iRobot’s earnings were hot garbage. But — and there’s always a “but” — this is probably the best outcome for any of you out there riding the Roomba romp.

We saw companies report glowing double-beat-and-raises all earnings season long only to wash up against the rocks. Following its stinker of a report, IRBT sank about 9% after hours Wednesday … and then immediately rebounded yesterday. It’s up another 2% today.

At a time when flawless earnings reports are met with pummeling sell-offs, iRobot got off easy. For once, Wall Street was able to put down its overly giddy expectations … and throw IRBT investors a bone for once, even if it’s just an earnings sell-off buying opportunity.

If you got into IRBT when we recommended it for Great Stuff Picks, you’re up about 12% right now. I’m keeping an eye to see just how iRobot handles its manufacturing problem … and how well its expectations bode with a potential pandemic resurgence.

Sike, I’ve always been too lazy to vacuum … and I’m still not going outside.

Don’t Buy Another Stock Until You Watch This…

In his newest video briefing, Paul breaks down the three stocks set to dominate the next decade.

Just one could return 3,900% in the next five years. Click here or on the picture below to learn more.

No. 4: Jumping The Loan Shark?

Finally! Another option to borrow money that doesn’t involve begging from family or negotiating percentage points with some sketchy dude in the corner booth at Applebee’s. Now I can choose the interest rate I get hosed on all through a mobile app — nifty!

For those of you just joining us, LendingClub (NYSE: LC) is one of these funky fresh fintech companies that offers peer-to-peer lending. You can take out personal or business loans (with a dollar-limit cap, so no crazy borrowing here) as well as refinance auto loans.

As it turns out, lots of people need to borrow money right now — who knew?

In its latest report, LendingClub’s revenue shot up over 400% year over year and reached $204 million, beating estimates for $129 million. Per-share earnings were even better: While pessimistic analysts expected a loss of $0.40, LendingClub’s earnings reached a surprise profit of $0.09.

The lending firm also boosted sales guidance for the full year, with its new revenue predictions beating analysts’ own targets by about $200 million. The thing is, no one expected all that much from LendingClub’s earnings anyway … until the personal banking fire nation attacked.

The company now offers an exclusive high-yield savings account — my heart’s pounding already, I tell you. Banking services are a whole new world of actually profitable operations, as CEO Scott Sanborn was sure to note: “Our first full quarter operating a digital bank was the most profitable quarter in LendingClub’s history.”

Why am I not surprised? You’re a bank now. Just like Robinhood … you are now the institution, congrats! This is the story of virtually every fintech startup recently.

You start out boasting about “we’re not like banks” mottos and samey “this is finance but personalized” mission statements. You offer some exclusive and revolutionary service, say money-transferring for Venmo or peer-to-peer lending in LendingClub’s case here. And things are hunky dory … but slow-growing.

Then, a bold moment of clarity presents itself … hopefully. You quickly realize that the only way to maintain growth is by offering more services. More products. More ways to attract new accounts.

And that’s why virtually everyone you see now offers personal banking, stock investing, money transfers. Essentially … they turn into banks … the very thing these fintechs swore to destroy.

Anyway, don’t let my cynicism bring you down — there’s no shortage of upsides to LendingClub’s report, and I fully expect its newfound love for interest income to seriously boost the company’s bottom line.

Even if that means LendingClub is becoming more and more like the “real banks” it’s trying to compete with.

When You’re Here, You’re A Great One

You made it! The weekend is fast upon us. But don’t think you’re getting out of here without a lil’ homework… (It’s not more math, I promise.)

This weekend, you have a breather from our usual Saturday rambling. This time around, I want to hear from each and every single one of you — especially you out there, thinking you could get by without writing in to us. Whenever the market muse calls to you, drop us a line!

GreatStuffToday@BanyanHill.com is where you can reach us best. We’ll even get the conversation started right here, right now:

- Is Wall Street too optimistic about Amazon’s earnings with COVID-19 resurging?

- Does Robinhood’s IPO crash have you rejoicing with schadenfreude?

- How do you feel about space stocks? You know … rockets, satellites and whatnot?

- Have you ever used Duolingo? If so, what language(s) are you learning and why?

- Peer-to-peer lending: Big shebang or big sham?

- What … is your quest?

Riddle me this, these questions six, and you shall avoid the Gorge of Eternal Peril! Or, more likely, we might feature your email in next week’s edition of Reader Feedback. So go on, whatever you feel like ranting about, we want to hear it!

In the meantime, here’s where you can find our other junk — erm, I mean where you can check out some more Greatness:

- Get Stuff: Subscribe to Great Stuff right here!

- Our Socials: Facebook, Twitter and Instagram.

- Where We Live: GreatStuffToday.com.

- Our Inbox: GreatStuffToday@BanyanHill.com.

Until next time, stay Great!

Joseph Hargett

Editor, Great Stuff