You know what really gets my goat?

Plenty of things, to be honest.

But the goat-gettingest thing of all is deliberate, self-interested spin masquerading as “research” on critical issues.

Energy is a case in point.

Recently, The Wall Street Journal published an article blaming a lack of investment in U.S. oil production on the Biden administration’s “hostile rhetoric, anti-energy legislative proposals, and oppositional regulatory policies.”

In this telling, one of the country’s biggest and most politically influential industries is afraid to make easy money because “anti-energy” politicians say nasty things about it.

Many U.S. political leaders want to move on from fossil fuels as quickly as possible and say so.

But to say their bullying determines investment decisions is horse hockey.

As an investor and as a concerned citizen, I try to base my decisions on facts.

When it comes to energy, facts are increasingly overwhelmed by self-interested rhetoric. That makes investing in energy a tricky business…

American Oil: Roller-Coaster Ride

Let’s start with some history (it’s kinda my thing).

Here’s the oil price over the last 20 years:

Oil averaged between $20 and $30 a barrel until the late 2000s boom sent it soaring. Just a few years later, the great financial crisis sent it plummeting.

Oil prices then stabilized between $90 and $110 a barrel. That coincided with the rise of the U.S. shale fracking industry. The new technology allowed U.S. oil producers to double output. In a few short years, the U.S. went from an oil importer to the world’s biggest producer:

Then it all collapsed. Fortunes made during the fracking boom vanished.

U.S. energy policy played a role in this reversal. But it had nothing to do with pro-green bias.

After the Arab oil embargoes of the 1970s, Congress made exporting U.S. oil almost impossible. So as the fracking boom gathered pace, it could only be used domestically. That pushed U.S. energy prices below global levels. The U.S. stopped importing more expensive oil from other nations, leading to a global glut.

But in late June 2014, the U.S. government agreed to U.S. oil exports. At the same time, Libya reopened export terminals closed by civil war. That upset the equilibrium in global markets, which were starting to soften as the recovery from the global financial crisis lost steam.

Sensing an opportunity, producers in the Persian Gulf decided to cut prices to push U.S. shale frackers out of business. In September and October of 2014, oil prices dropped 40%, finally stabilizing below $50 a barrel.

At that price, U.S. fracking production was uneconomical. U.S. companies, having borrowed heavily to expand their rig counts, went bankrupt by the dozen. The Wall Street lenders that financed the fracking boom took a painful haircut.

Energy investors were crushed.

Thanks, but No Thanks

Eventually, oil prices stabilized at around $55 a barrel. But that was still too low to restart the U.S. fracking boom.

Then COVID crushed global demand. Global oil output in December 2019 was 10.3 million barrels a day. By the second quarter of 2020, it had fallen to 9 million barrels. Prices began to slide precipitously.

In late March 2020, Saudi Arabia and Russia started a price war to capture market share and prevent a rebound in U.S. shale production. In one week, prices fell by 40%. On April 20, 2020, the price of West Texas Intermediate briefly went negative.

Oil prices recovered during 2021 as COVID vaccines rolled out. But after a brief dip in December on recession fears from U.S. interest rate hikes, oil rose rapidly as Russia threatened Ukraine.

Oil soon jumped above $100 a barrel. The average cost of U.S. gasoline surpassed $4 a gallon, then $5.

U.S. shale producers have a breakeven oil price close to $30 a barrel. But U.S. domestic oil output remains stuck 15% below the pre-pandemic high. U.S. oil rig count is 25% below March 2020.

Why isn’t American supply responding to price signals from the global market? Are they “anti-energy?”

Wall Street Remembers…

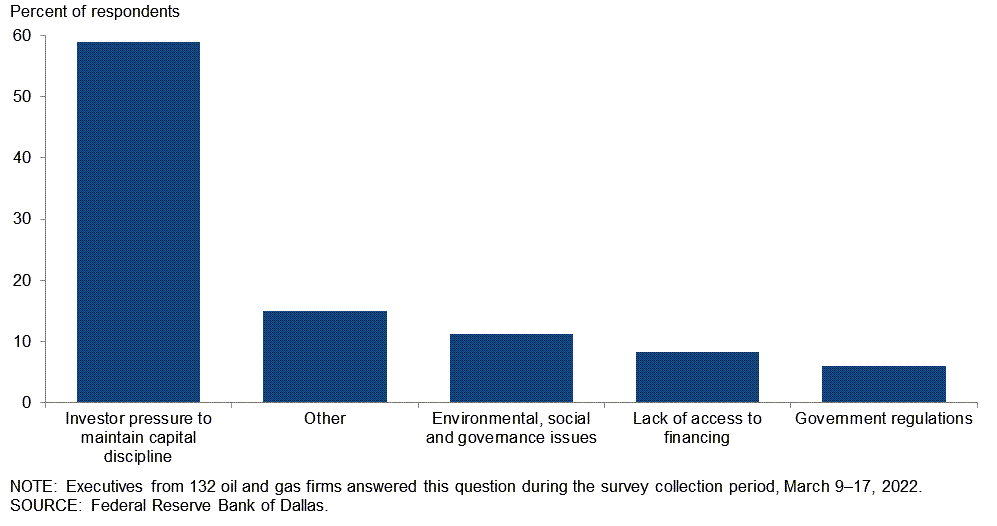

The Dallas Federal Reserve recently asked oil company executives exactly that question. Here was their response:

Why American oil companies aren’t taking advantage of soaring prices.

(Click here to view larger image.)

The “green” issues The Wall Street Journal tells us “have succeeded in driving capital away from the industry” turns out to be a relatively minor concern.

The biggest problem is that Wall Street has a memory of getting burned in 2014. They don’t want a repeat of that.

They vastly prefer that U.S. oil producers use temporarily higher prices to buy back shares and pay dividends rather than invest in new production capacity that could easily be wiped out the next time the market turns.

So, it turns out that U.S. energy policy is driven too much by markets, not too little.

But you’re not going to hear that from The Wall Street Journal.

The U.S. needs more government intervention in energy markets, not less. It’s precisely because the government doesn’t intervene more forcefully that energy prices are so volatile.

But I see a light at the end of the tunnel … which is why my team and I are working on exciting new energy investments that will ride the upcoming energy revolution all the way to the top!

Kind regards,

Ted Bauman

Editor, The Bauman Letter

{kind=link}