The Blue Chip Blues

Well … it’s flooding down at Walmart (NYSE: WMT). All of the inventory is marked down.

Yeah, it’s flooding down at Walmart. All of the inventory is marked down.

I’ve been tryin’ to buy food for my baby. Lord, and I can’t spare a single dime…

Oh! Let me guess… “Texas Flood”?

Got it in one, Great Ones. Wall Street has the blue chip blues today, and Walmart certainly didn’t help matters.

Heck, Walmart wasn’t even supposed to be here today!

It isn’t on the earnings schedule until August 16.

But when you know your results are gonna be ugly, I guess it’s better to rip the Band-Aid off early and give your investors time to prepare.

Bright and early this morning, Walmart slashed its Q2 and full-year earnings guidance.

Specifically, Walmart now expects Q2 earnings to fall between 8% and 9% from 2021, with full-year 2022 earnings to plunge between 11% and 13%. Previously, the retail giant called for 2022 earnings to be down only about 1%.

That’s some Jason Voorhees kinda slashing.

Here’s how things are playing out at Walmart right now: Food costs are rising — duh — and that means customers have less money to spend on other things, like clothing and other durable goods.

The company noted that while food inflation is driving top-line growth, said inflation is “requiring more markdowns to move through the inventory, particularly apparel.”

What’s more, Walmart also said that customer focus on food and consumables is “negatively affecting gross margin rate.”

In short, Walmart is saying out loud what many of us already know: The cost of basic necessities has gone up so much that discretionary spending is falling like a rock.

I mean, it’s hard to justify buying that new air fryer when the cost of french fries is going through the roof. Just sayin’…

Remember, kids … when the Federal Reserve looks at inflation, it doesn’t look at food, energy or rent costs.

Yet here we are with Walmart directly saying that inflation on these specific goods is driving down demand for literally everything else.

To combat this scenario, Walmart is pulling a Target (NYSE: TGT). Remember back in June when Target said it was marking down overstocked inventory left and right just to get it out the door?

Well, that’s exactly what Walmart is doing now. I have to tell you, Great Ones, that this does not bode well for the retail sector at all. If both Walmart and Target are signaling that inflation is killing their customers, it’s only a matter of time before the rest of the retail sector follows suit.

Instead of the retail sector … or Walmart … or even Target, what you should look into isn’t a stock at all.

It’s “wiretapping.”

Wiretapping?

Wire. Tapping.

Andrew Keene has been killing it this year. In a year where the S&P has dropped 18%, and the NASDAQ has dropped 28% … his portfolio has produced 72% winning trades.

Using his “wiretapping” system, Andrew can see exactly where the smart money is going the moment they place their trades.

He shares these signals with members of the exclusive Trade Room. And by following them, members have seen one-hour gains as high as 100%, 230% and 250%.

The Good: Generally Shocking

Y’all know it’s a weird week when General Electric (NYSE: GE) — of all companies — is the best the market has to offer. I mean, remember when we all thought GE was on the verge of going under?

Now look at it … reporting a 95% surge in Q2 earnings to $0.75 per share, with revenue rising 1.75% to $18.6 billion. Both figures beat Wall Street’s expectations, with earnings nearly doubling the consensus estimate for $0.38 per share.

In this market, that’s kinda impressive.

But we all know that last quarter doesn’t mean much anymore. It’s all about guidance and expectations now. And General Electric came as close to a beat-and-raise quarter as we’re likely to see this earnings season.

Looking ahead, GE reiterated its full-year guidance of earnings between $2.80 and $3.50 per share — albeit targeting the lower end of that range now. Additionally, GE said that free cash flow would be down by about $1 billion. So yeah … costs are piling up at GE just like everywhere else.

GE stock gained more than 5% on the day.

The Bad: The Song Remains The Same

If you are looking for something other than “supply chain woes” and “rising costs,” I’m sorry to tell you that you won’t find it in General Motors’ (NYSE: GM) Q2 earnings report.

The American auto giant missed Wall Street’s earnings target, posting a profit of $1.14 per share and coming up $0.06 short of the consensus estimate. Revenue rose to $35.76 billion, however, blowing past expectations for $33.58 billion.

The problem is that strong revenue isn’t enough when you’re struggling to get parts and watching your margins plummet from 11.2% in Q1 to just 6.6% now. GM said it has about 100,000 incomplete vehicles just sitting there waiting to ship once … you know … it can get semiconductors again.

“We have been operating with lower volumes due to the semiconductor shortage for the past year, and we have delivered strong results despite those pressures,” said CEO Mary Barra.

Despite these hurdles, GM reiterated guidance for net income of between $9.6 billion and $11.2 billion for 2022. The company believes that once it can complete those thousands of vehicles waiting on chips, everything will be just hunky dory.

Now, I’m not saying there isn’t pent-up demand for GM vehicles. New cars have been a bit hard to come by due to the supply chain crunch. What I am worried about is GM’s optimism that all it has to do is “build it and they will come,” so to speak.

Go look at Walmart’s report again and then tell me that GM will still hit this year’s sales targets. I’m bullish on GM’s long-term growth, but even I can see the writing on this wall.

But you don’t have to wait for GM to get its … umm … stuff together. According to Charles Mizrahi, this groundbreaking technology is going to make gas guzzlers obsolete. But it has nothing to do with EV manufacturers, lithium-ion batteries or recharging stations.

This is the investment opportunity of a lifetime, but I won’t spoil the surprise.

Click here for the full story.

The Ugly: What!? I Can’t Hear You!

OK, so 3M Company (NYSE: MMM) should probably be in today’s “The Good” slot, if you’re just looking at the company as an investor.

Earnings and revenue both topped Wall Street’s expectations, and 3M announced that it is spinning off its health care business — in which 3M will retain a 20% stake.

All three of these things are excellent news for the company and investors.

Heck, 3M even lowered its full-year expectations less than expected — dropping earnings to a range of between $10.30 and $10.80 per share from prior guidance of $10.75 and $11.25 per share.

As a result, MMM stock closed up more than 6% on the day.

Investors are happy. Wall Street is happy. What’s stuck in your craw, Mr. Great Stuff?

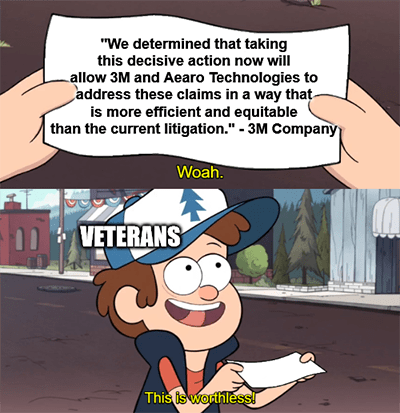

I’ll tell you, since you asked. 3M subsidiary Aearo Technologies is voluntarily filing for Chapter 11 bankruptcy. Why? Because some 235,000 U.S. armed forces veterans have filed suit against the company due to hearing loss because of faulty Aearo Combat Arms Earplugs.

3M maintains that these ear plugs are perfectly fine when used as directed but, just in case, Aearo Technologies is reorganizing under Chapter 11 to … well, y’all already know why. We’ve seen this dog and pony show before, haven’t we?

3M has set aside $1 billion to fund a trust to resolve all 235,000 claims. According to 3M, it’s allowing the bankruptcy and setting up the fund to “address these claims in a way that is more efficient and equitable than the current litigation,” which could take years or decades to resolve.

The thing is, filing for Chapter 11 will shield Aearo from potentially considerable monetary liability … possibly more than the $1 billion that 3M has dedicated already.

Now, I know that 3M is walking a fine line here to both support our troops and make sure investors are taken care of. As an investor, I can appreciate that.

But as a U.S. citizen, I just think that taking care of the men and women that put their lives on the line to serve and protect our country should be more important than shareholder value. And if that makes me a “bad” investor … so be it.

Sound Your Barbaric Yawp!

So what do you think, Great Ones?

Is Walmart’s warning another brick in the recession wall?

Is 3M doing enough to make things right with veterans?

Will GM’s flood of finally-finished vehicles keep it from cutting guidance?

Is General Electric the real deal?

Inquiring minds want to know!

That’s me. I’m “inquiring minds.” Drop us a line with your thoughts at GreatStuffToday@BanyanHill.com.

Once you’ve shared your thoughts, here’s where else you can find us across the interwebs:

- Get Stuff: Subscribe to Great Stuff right here!

- Our Socials: Facebook, Twitter, Instagram and TikTok.

- Where We Live: GreatStuffToday.com.

- Our Inbox: GreatStuffToday@BanyanHill.com.

Regards,

Joseph Hargett

Editor, Great Stuff