You’ve heard it all … from the Federal Reserve’s interest rate hikes, the war in Ukraine to China’s COVID concerns.

Despite all that, the market’s doing alright. But what if that could change in an instant?

In today’s update, I give you the insider knowledge on what Wall Street won’t tell you. I have five ways the stock and bond markets might tip toward a BIG crash and what you can do today to protect yourself.

Click here to watch this week’s video or click on the image below:

Transcript

You remember the movie The Big Short? It was about the mortgage-backed security market. It was about what happened during the subprime crisis. There was a great scene in that movie when Ryan Gosling is explaining to a hedge fund manager that the bond market was like a Jenga stack. Well, I’m here today to tell you that based on my recent observations, I think the Jenga stack is the stock market.

Now, my name’s Ted Bauman. I’ve been doing stock market analysis for a long time. I’ve been on TV shows. I’ve been on Bloomberg News. I’ve been quoted in Forbes. I’ve been quoted all over the place. I predicted the collapse of 2008. I predicted the pullback in 2020, even though I didn’t predict COVID. I did say that the market was ripe for a pullback and I was right. Well, this time, I think we’re ripe for a pullback again. And this time, I think a lot of people are discounting it just like they did in the subprime crisis.

Before I go on, I want you to do three things. First, I want you to like this channel so you can keep up with what’s going on, because I’m going to be reporting on this issue throughout the year. No. 2, I want you to comment. I want to know what you think. If you don’t like me, fine. Go ahead and say it. If you do like me, tell me that too. I just want to be engaged. The last thing I want you to do is click on the little “I” above my left shoulder. That is where you can get access to my favorite investment for 2022.

It’s a special report that tells you exactly how to protect yourself from that. Now, today, I’m going to show you five things that could trigger a stock market collapse. I’m not saying when they’re going to happen. All I’m saying is that the odds are mounting. But the fifth reason is one that is probably going to get me in a lot of trouble with my friends from Wall Street. They’re probably going to ask me not to talk about it. It wouldn’t be the first time.

Things may be dire, but I don’t want you to sell all your stocks. I don’t want you to liquidate everything and stuff money under your mattress. You can’t afford to do that in an inflationary environment. As you’re going to see, one small tweak in your strategy could flip the script on your financial future and turn you from victim to victor. Trust me, I’m an economist. I’ve been watching this stuff for a long time. I’ve got people following me from Morgan Stanley, Merrill Lynch, JPMorgan, but I’m also a husband and a father so watch on and I’ll show you the step I’m taking to protect my wealth. Now, let’s start by talking about how bad things are…

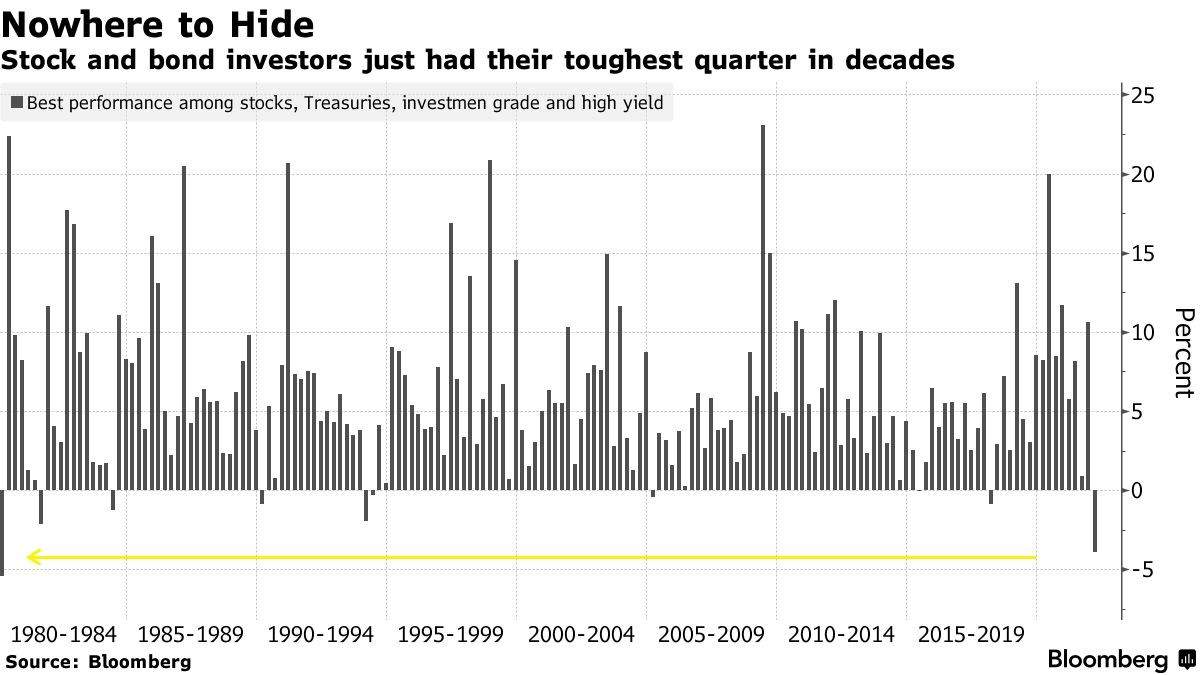

Did you know that more than $3 trillion was erased from bond and equity values in the first quarter of this year as the Federal Reserve raised interest rates for the first time since 2018. Here’s a chart that shows exactly what happened:

The yellow line shows you the relationship between the current pullback and the last big one we had. You have to go back to the 1980s to see a pullback as big as we’ve had in that quarter. Now, how would you feel if I told you that despite all of that, assets are still overpriced, hence they still have a lot further to fall?

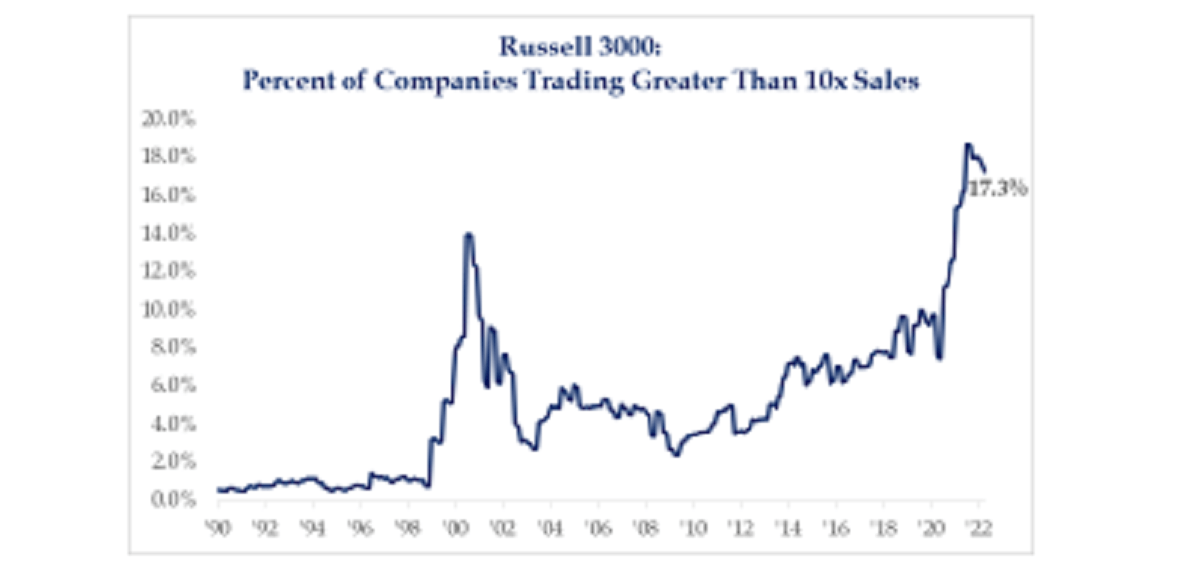

The problem is that the yield on both stocks and bonds is negative for the first time in recent history. When you factor in 8.5% inflation, you’re losing money at the index level. Let me explain why. Right now, the S&P 500’s earning yield, which is basically the inverse of the price to earnings ratio, it’s telling you how much earnings you’re getting per dollar that you invest, is only 4.4%. That’s one of the lowest it has ever been. So, basically, the earnings that you’re getting from the stock market in relation to the prices that you’re paying for stocks, even now, even after the first quarter collapse, is still higher than it’s been for a long time. One out of every five companies in the Russell 3000 is trading at more than 10 times their revenues. That’s even worse than the dot-com era. Here, look at the chart:

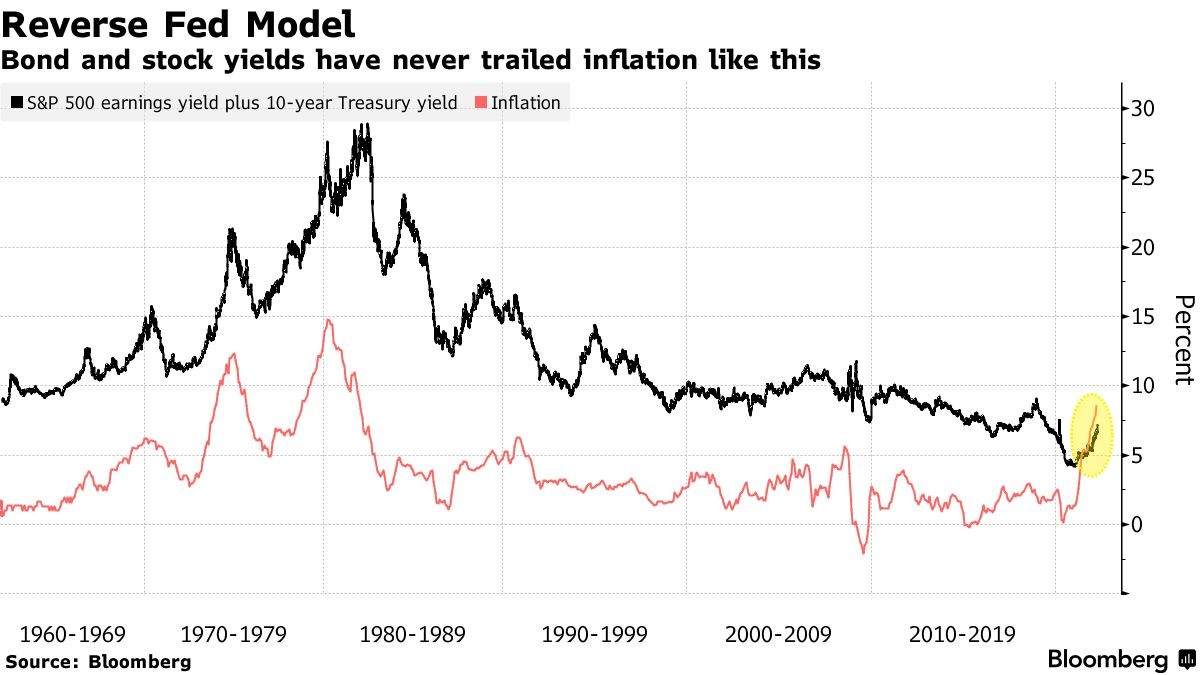

17.3%. If you go back to the dot-com period, it was only 14%. So we got a real overvaluation problem here, and on top of that, even after the recent Treasury bond yield hikes or the Federal Reserve hikes and the associated increase in the Treasury yield, it’s still less than half of its historical trend. Now, when you put those two together, let’s say that you’re an investor who’s got 50% in stocks, 50% in bond, not something I’d recommend, but it works out for the math. Here’s a chart that shows you the way this works:

This chart shows the S&P 500 earnings yield plus the 10-year Treasury yield and it compares it to inflation. It’s never been this low relative to inflation. Inflation is higher than the earnings yield that you are getting from the S&P 500 and the potential yield that you’d be getting if you were holding bonds. There’s basically nothing you can do if you’re just playing at the index level. So the bottom line here is that stocks and bonds are still overpriced despite the pullback in the first quarter.

The only thing that’s keeping them elevated is the muscle memory for more than a decade of Fed market manipulation. There are still people out there who believe that this is just a temporary glitch, who believe that the Fed’s going to ride to the rescue if things get really bad. They still believe that stocks only go up even despite the results of the last year or so. I’m here to tell you that’s just not the case. Stocks are waiting to be pulled back to a more reasonable leveled evaluation and so are bonds. Now, we know that the Fed is tightening dramatically and it’s not going to stop on behalf of the stock market. Here are five things that could tip both stock and bond markets into a big crash. Now, after that, I’m going to tell you how you can protect yourself. The first thing is that the Fed causes a hard landing. Everybody talks about the Fed raising interest rates, but doing so in a way that prevents the economy from tipping into recession.

Now, it’s true that the economy is going pretty great guns right now despite inflation. In fact, the rate of growth of the economy is one reason why inflation is so high. Most people don’t think the economy is doing well because they only focus on prices, but if you look at the big picture, like I do, you can see we’re getting dramatic increases in production, in GDP growth. We’re seeing labor market hiring at the fastest clip we’ve seen in a long time. We’re down to unemployment rates that we’ve only seen once before, just before the COVID crisis. That means the economy’s going great guns. But if the Fed over tightens, if the economy gets spooked because interest rates are rising, it could go into recession. If it goes into recession, all of a sudden, all bets are off because we haven’t seen a real recession, IE. a recession that wasn’t caused by a big crisis like the Subprime Crisis or COVID for a long, long time. So a lot of investors don’t know how to deal with it, and when they find out, they’re going to panic and sell.

The second trigger is if the war in Ukraine gets worse, then what’s Europe going to do? Well, they only have one other card to play and that’s to cut off all energy imports from Russia. If that happens, that would cause an energy crisis and tip Europe into recession. That would spill over into the global economy, which would in turn drag down the United States as well, not to mention the European financial system, which still has a lot of banks that are struggling, not just from the recent problems in Russia and the sanctions against them, but also historically being weak, really going back to the Subprime Crisis. The third potential trigger is if rising mortgage rates lead to a collapse in the housing market. The additional pressure on the rental market, people fleeing or not buying houses, but rather going into rental will cause rents to soar even further than they have. Rents have been up on an average about 16% in the last year. In some places, they’re up over 35% just in the last year.

What happens when that happens? Well, it reduces disposable incomes and that means that people no longer have enough to spend. That means that, all of a sudden, boom, the economy doesn’t have the gas that keeps it going and we go into recession. The fourth potential crisis or trigger that could cause the Jenga step to collapse would be if rising interest rates trigger a credit crisis in the junk bond sector. Now, when interest rates are really low, as they’ve been since 2009, it encourages companies to load up on debt. That in turn makes them more susceptible to damage from rising interest rates. Already, we’re seeing signs of stress in the junk bond sector, those companies rated Triple B or less, where effectively their repayments on interest are rising at the same time that their potential earnings are going to fall if we go into recession. That in turn could trigger a credit crisis, which in turn could lead the economy as a whole to contract as banks hold back like what they did in 2008.

But the fifth one is the most dangerous of all, and this is what Wall Street doesn’t want you to know. Declining bond yields lead to a spiral in liquidity because nobody wants to be the one to buy the bond on its way down. So everybody waits for the bonds to fall as far as they’re going to go. Everybody hangs back. They don’t buy. All the big bond traders hang back waiting for yields to fall again. But that in term becomes a self-fulfilling prophecy and the Fed is no longer the buyer of last resort. In fact, the Fed is planning to sell its own bonds. All of that could lead to an uncontrollable spike in yields, sending the financial system into a crisis that would make 2008 potentially look like a walk in the park. The big question is, will the Fed ride to the rescue this time or will it just accept that, that is the price of putting the economy back onto a “sound footing”? Well, maybe the economy would on a sound footing at least to go forward, but what about your portfolio?

Now, remember, the problem here is that there’s no safe asset in this scenario. Events like this can cause cross asset contagion. When the overall system gets stressed like this, there’s an evaporation of liquidity from all markets as people try to scramble to dump other assets to raise cash. That means crypto, even gold, at the beginning of a crisis is not a good haven because everybody’s selling it to raise cash. So the big question is, if one of these things were to happen, and keep an eye on this channel because I’m going to be keeping an eye on all five of these things all year, is to move your money into investments that are going to thrive in this environment. Now, I believe that the safest investments, and I’ve been saying this for a while, are those companies that have strong balance sheets, strong income, that are recession resistant, and that can protect themselves from this kind of collapse. Not just because they’re going to carry on making money, even in a recession, but because other investors are going to flee to them as safe assets once they realize what I’m talking about.

Now, I’ve already got a portfolio already made for you if this is interesting to you. It’s called Endless Income. It’s doubled the market’s price performance in the last year. In the last six months alone, my Endless Income Portfolio has outperformed the stock market by a factor of eight. That’s right, your returns in the last six months from that portfolio, and this is just prices, this doesn’t include dividends, is 800% higher than the stock market. Now, on top of that, the cumulative dividend yield of my portfolio is 7.75%. That’s enough to compensate you for inflation. That doesn’t even include the increase in prices, which as I said, has beat the market in the last six months by 800%. Now, when you put those two together, you’re in a position to beat the market hands down this year while everybody else will be like one of these Jenga pieces, boom, down.

Now, if that sounds like something you’d like to be part of click on the link below or click on the little “I” above my left shoulder to access my special report on my favorite investments for 2022, which tells you exactly how to do what I’m doing to protect my wealth and the wealth of those who subscribe to my Bauman Letter.

This is Ted Bauman signing off. I’ll talk to you again next week.

Kind regards,

Ted Bauman

Editor, The Bauman Letter