“It’s been an ideal period for investors: A climate of fear is their best friend.”

That quote comes from Berkshire Hathaway’s 2009 annual report.

This report, written by Warren Buffett, came just months after the end of a massive stock market crash.

It contained some timeless advice:

Those who invest only when commentators are upbeat end up paying a heavy price for meaningless reassurance. In the end, what counts in investing is what you pay for a business … and what that business earns in the succeeding decade or two.

Buffett even went so far as to pen a rare New York Times Op-Ed titled “Buy American. I am.”

He told the world he was buying American stocks, and he wasn’t waiting for the market to bottom out.

Just over a year later, Buffett famously bought America’s largest rail company — Burlington Northern. At the time, it was Berkshire’s biggest deal. It paid off — to the tune of $8.8 billion in profits in 2021 alone.

Buffett wasn’t the only one going all-in amid the crash either.

John Paulson became an investing legend when he made $15 billion shorting the housing bubble. Then, starting in 2009, he made billions more by betting big on bank stocks as they bounced back.

JPMorgan CEO Jamie Dimon earned much of his $1.8 billion net worth by investing in shares of his own bank after the crash. Those shares have more than tripled from that year’s lows.

I realize that these success stories may be the last thing you want to hear right now.

The S&P 500 is 15% off its highs. Rising rates have wreaked havoc on the bond market with the worst sell-off in 70 years. (Higher rates are hitting the housing market, too, which I wrote about on Sunday.)

And with all this, inflation is still running rampant on American savers…

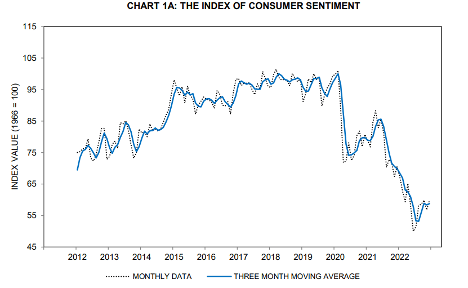

It’s no wonder the University of Michigan’s Consumer Sentiment Index is barely above its lowest point in history:

Consumers are the most nervous they’ve been in over a decade.

It’s a scary time to be an investor … a homeowner … and a saver.

Three things that describe most middle-class Americans.

But there’s a light at the end of the tunnel.

Right now, we’re reaching a critical turning point in this bear market…

Sentiment often sets new lows shortly before the market bounces back.

In other words … it’s always darkest before the dawn. And things tend to turn around much faster than most investors expect. Following bear markets, stocks return an average of 42% in the first year.

Like Warren Buffett quipped as he bought stocks before they bottomed out: “If you wait for the robins, spring will be over.”

So instead of waiting for stock market bottoms, I’m going to show you which stocks will lead the next recovery…

I’ll also tell you which stocks won’t be “coming back” to their previous highs — and why.

It all starts with…

The Most Valuable Thing About Bear Markets

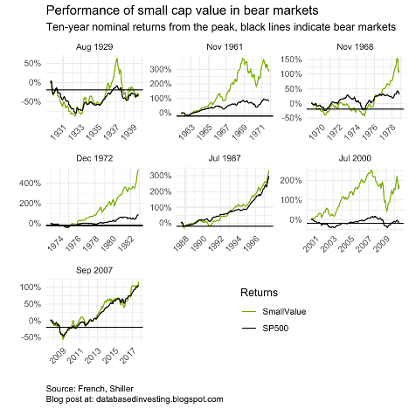

Since the Great Depression, we’ve witnessed 26 bear markets. During each of those, we’ve seen a consistent pattern in how stocks perform.

Namely, small-cap value stocks are nearly always the best bet.

Just take a look at the years that followed seven of the biggest bear markets of the last century:

As you can see, small-cap value stocks almost always outperform in the years that follow bear markets.

The same is true for recessions. That’s important because most economists now expect we’ll face a recession in 2023. (As you well know, I agree with them.)

In 9 out of the last 10 recessions, small-cap stocks have outperformed — delivering an average return of 17% during the second half of each recession and over 27% a year later.

That means time is of the essence.

To quote Anchor Capital: “We believe recessionary environments are favorable times to contemplate investment in small-cap stocks, as history indicates small caps tend to outperform larger caps before an economic recession ends.”

We saw plenty of examples of this play out after the bear market of the early 2000s.

Take Meritage Homes Corporation, for example. It’s a real estate development company.

From March 2000 to October 2002, it saw a massive 632% return.

Chico’s, a small-cap stock at the time, also saw a similar swing up. Over that same time frame, share prices went up 581%.

Likewise with Medifast, a nutrition company. It soared 484% by the end of the bear.

Of course, that’s not to say all small caps are created equal.

The Critical Ingredient for Small-Cap Success

Small-cap stocks are often the biggest victims of bear market fear. They’re also the most likely to lead the charge as markets recover.

But while some of today’s most beaten-down stocks deserve to be priced far higher — some could stand to be beaten down a little more.

Take Nikola, for example. This electric truck battery manufacturer was a darling of electric vehicle investors.

After going public in June of 2020, shares rocketed up 500%. Industry insiders talked about the company becoming the next Tesla.

The company just had one problem: It didn’t have any revenue.

And while share prices were soaring, Nikola was also burning through cash. A billion dollars a year, to be precise.

Not to mention that it was caught rolling a prototype truck down a hill for a promotional video.

Once all this came to light, investors realized the company would need to raise more capital to get things moving. Nikola’s shares tanked soon after.

Shares are now down over 95% from their high, worth less than $3.

If you haven’t guessed it yet, the one critical component for small-cap success: revenue.

The best small caps right now are the ones making money, or those that will in the near future.

Without one or the other, small caps will have trouble performing in these markets.

I know. There are plenty of exciting companies with promising technology out there. But in today’s environment, small caps need to show investors the cash.

Thinking in these terms can help when it comes to…

Spotting a Small-Cap Landmine in Your Portfolio

According to CFA and Goldman Sachs alum John Morrison: “Small companies with high stock prices that lose money or generate little profit may be holding back your small-cap portfolio.”

Morrison pointed out that the five biggest detractors from the Russell 2000’s return all posted negative profits compared to the year prior.

All five also sold at price-to-book ratios in the top quarter of the market.

Once again, they’re not necessarily bad investments. They’re just bad for this market.

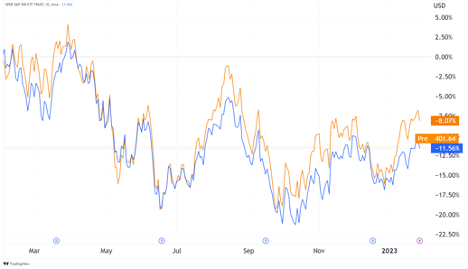

Even as the broad market soared to new highs in 2021, small-cap stocks with low profitability bombed. And things only got worse for those stocks in 2022.

But on the whole, small caps are still outperforming. Over the last year, the Russell 2000 has edged out the S&P 500:

And once markets hit bottom, we can expect this trend to continue.

Which leaves us with just one question…

Should You Buy Small-Cap Stocks Right Now?

I’ll keep it simple: The answer is yes.

I can think of five reasons small caps should be in your portfolio today:

- Unrivaled upside — Quality small-cap companies that are already turning a profit can deliver consistent returns … even before a market bottom.

- Perfect for rebuilding portfolios — With small caps’ rapid earning potential, you can earn gains in a 5- to 10-year time frame.

- More immune to global turmoil — Unlike global large-cap companies, small caps often deal with an all-American market, allowing you to avoid global unrest.

- Value matters — You can’t dispute the sheer value in small caps right now. The Russell 2000’s price-to-earnings ratio is down by double digits in the last year.

- Almost everyone started small — Today’s biggest stocks started out as small companies. It’s true that not all succeed. But it’s a fact that some go on to become massive companies.

But I’ll be frank. I expect the first quarter of 2023 to be rough — real estate crumbling, certain stocks crashing and unemployment spiking.

So now is not the time to be wading into the “blood in the streets” by yourself.

That’s why my team and I just put the finishing touches on a presentation called the Middle-Class Massacre. Here, I lay out all the details for you on what to expect the rest of this year — and one stock I expect to soar even as the American middle class gets squeezed.

If you’d like to see this video for yourself, I encourage you to click here and watch the entire presentation.

Regards, Ian KingEditor, Strategic Fortunes

Ian KingEditor, Strategic Fortunes

Read Strategic Fortunes reviews from real subscribers here!

Market Edge: The Middle-Class Real Estate Massacre

The typical American has about 70% of their net worth tied up in their home.

Now, a good bit of this can be explained by the bubble in- home prices that Ian mentioned on Sunday. When homes go up more in two years than they did in the previous 20, your home equity ends up making up a larger percentage of your net worth than you might have planned for.

And unlike a 60/40 stock and bond portfolio, where you can generally rebalance your portfolio in a matter of minutes when your weights get out of line, it’s not practical to rebalance your home equity. (If I told my wife we needed to sell our house and downgrade to something smaller to rebalance our portfolio, she would assume I’d gone mad.)

This means the vast majority of Americans are overexposed to the single-family housing market … putting them at risk of what Ian calls the “Middle-Class Massacre.”

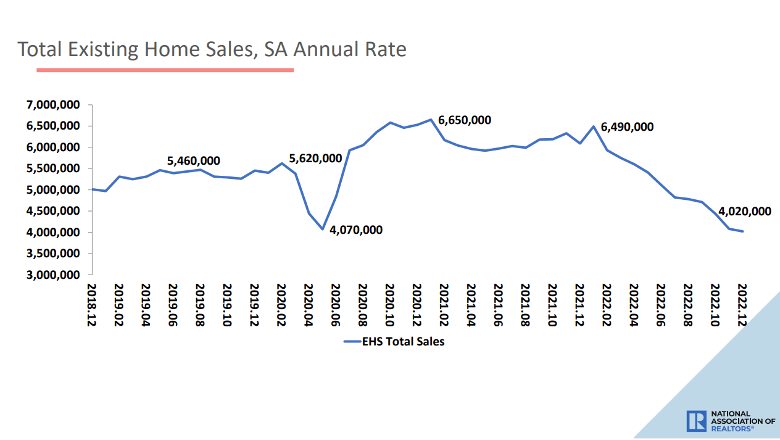

This theory plays out in the numbers. Take a look at this chart:

Existing home sales are down by close to 40% over the past year, and there is no sign of the trend turning around.

Economists tend to focus on new home starts and sales because it’s a better indicator of economic growth. That may be true, but existing home sales are more critical to the financial health of the typical American. Your home is an existing home, after all.

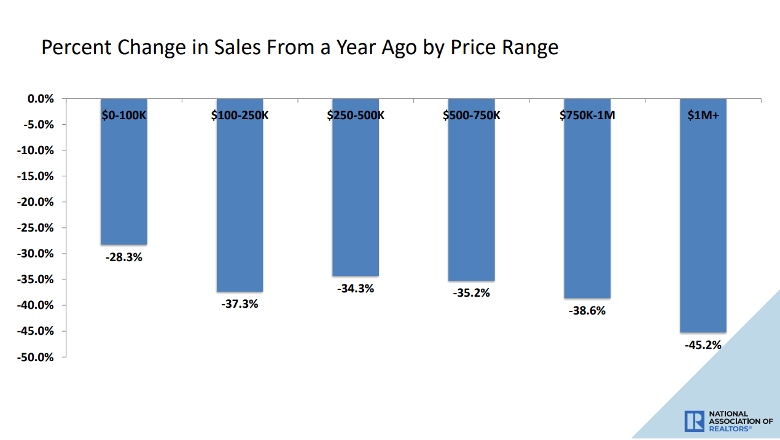

So, sales are down. Now, let’s look at which parts of the market that’s hitting hardest:

As we can see, sales declines are distributed pretty evenly across property prices.

Houses in the million-plus range have seen a larger decline in sales, which isn’t terribly surprising. High-end properties tend to take longer to move, and the owners often have the means to wait for the price they want.

But even at the mass market level, we’ve seen a massive slowdown in home sales. And the single biggest reason is the cost of financing.

The explosion in high property prices in 2020 and 2021 was made possible by record-low financing costs. But with mortgage rates now twice as high as they were a year ago, buyers can’t qualify for financing.

The housing market is effectively frozen. But it can’t stay that way forever. Eventually something has to give. Either home prices have to fall, mortgage rates have to fall, or some combination of the two.

This is something that should be scary to every homeowner. But as Ian mentioned today, you don’t have to be caught unprepared.

There are still great opportunities to be found in small-cap stocks and other pockets of the market that will be the first to come out of the bear.

Ian created a report called How to Survive & Prosper the Middle-Class Massacre with a full game plan for the coming housing crisis — as well as what’s happening with inflation and the stock market.

For the full details on how to get your copy, click here.

Regards, Charles SizemoreChief Editor, The Banyan Edge

Charles SizemoreChief Editor, The Banyan Edge