![[4-Question Checklist]: Ensure High-Quality Stocks for Retirement](https://banyanhill.com/wp-content/uploads/2023/04/shutterstock_512665549-440x264.jpg)

Let’s play a game…

When you look at these 10 companies, what first comes to mind?

- American Airlines

- AT&T

- Goldman Sachs

- Ford Motor Co.

- Boeing

- Wynn Resorts

- Walgreens

- Allstate

- Kraft Heinz

- Wells Fargo

If you associate these 10 companies with the S&P 500, you’re correct — each is included in the world’s most watched and owned stock index.

And if you said “household names” — correct there, as well. These are global giants with name recognition the world over.

But if “high-quality” came to mind, that’s where I’ll stop you.

Because, according to my stock rating model … each of these 10 stocks are low quality.

At best they’re rated “bearish.” Some are rated “high-risk.”

Is it alarming that such low-quality stocks command nearly $700 billion in value combined … and are a stalwart in many Americans’ retirement accounts?

You betcha, it is!

I said last week that “value” boils down to what you get for the price you pay.

And with stocks, the quality of a company’s earnings, cash flows and balance sheet is what determines the “what you get” of this equation.

So today, I’ll show you exactly how to find high-quality companies (and avoid low-quality ones).

And in the process, I’ll help you understand why some of the blue-chip stocks you know and trust, and likely make up a huge portion of your retirement account, aren’t as safe as you may think…

Finding Quality: A 4-Question Checklist

When you want to determine a stock’s quality, there are four key questions you need to start with:

- What are the company’s gross and net profit margins? Are they “razor” thin, or “fat” and robust?

- How does the company’s net profits compare to the size of its assets, or equity?

- How much free cash flow does the company generate, and is it increasing or decreasing?

- How much debt does the company hold, relative to its cash and relative to the amount of income it has to service the debt?

There are plenty more questions you can ask about the quality of a company, but these cover the basics.

So, let’s ask these questions about American Airlines (Nasdaq: AAL) — the top airline in the U.S. on market share, passengers flown and fleet size … but actually one of the lowest-quality stocks you can buy.

- AAL’s gross and net profit margins are 23% and 0.3%, respectively — the latter of which is the very definition of “razor” thin. Any hiccup and the company’s profits evaporate, as they did in 2020 and 2021.

- The company owns a lot of assets, but its return on those assets (ROA) is a paltry 0.2%.

- A look at AAL’s free cash flow shows another red flag — it was $292 million in 2021, but plummeted to negative $733 million last year.

- And finally, the company’s debt position also paints a troubling picture. It has $43.7 billion in total debt and only $9 billion in cash. All it takes are these four questions to understand why American Airlines is low-quality.

What’s more, the stock doesn’t deserve the sky-high valuation it goes for — with its 66 price-to-earnings ratio versus the industry’s average of only 8.9.

(Even its biggest competitors, Delta Air Lines and Southwest Airlines, trade at more reasonable P/E ratios of 11.2 and 37.5.)

My stock rating model confirms that conclusion — the stock rates 21 out of 100 on my Quality factor, and a dismal 12 overall — placing it in the High-Risk category.

And so, at this point, I bet you’re hoping you don’t own any shares of the company, right?

But that’s the thing … I’m all but certain you do.

Why Your Retirement Is Trapped in Low-Quality Stocks

You own shares of AAL by way of that ultra-low-cost Vanguard mutual fund you likely have lurking in your 401(k).

Maybe you’re paying a pittance in fees to Vanguard each year, but it’s costing you a whole lot more in terms of the drag that the low-quality S&P 500 stocks have on your total investment returns.

See, Vanguard promises to put you into the most popular U.S. stock benchmark at low cost. It does not, however, promise to put you into the best high-quality stocks, nor into only the individual stocks that are trading at favorable valuations.

I actually did an “x-ray” scan of the individual stocks currently held in S&P 500 ETFs and mutual funds, whether sponsored by Vanguard, State Street or any other provider.

What I found is something you may find shocking…

Almost half of them rated neutral/bearish to “high-risk” on my model’s Quality factor.

Only a minority of the individual stocks in the S&P 500 earn the “Strong” Quality rating I look for when I recommend stocks to my readers.

Frankly, the S&P 500 may be a collection of the BIGGEST and most recognizable stocks on the market … but it is by no means limited to the BEST stocks you can buy.

Far from it.

That’s why I’ve made it my mission to show investors better opportunities, often in smaller, overlooked stocks that others have passed on.

And today is my latest, greatest step towards that goal.

Today, I aired a brand-new presentation which details a group of small, overlooked stocks that aren’t just flying under the radar of everyday investors … but multibillion-dollar financial firms.

These stocks are all extremely high-quality, while also presenting an unmissable growth opportunity that’s exclusive to us.

You see, these stocks all trade below $5 per share — which puts them in “off limits territory” for the big trading houses. An SEC rule effectively prevents them from touching these stocks whatsoever.

And that’s an incredible opportunity for us… Because it means we buy up these stocks at incredibly attractive prices and valuations long before these firms can take multimillion-dollar positions.

Anyone that signed up to watch this presentation already got access to a list of 39 overlooked, high-quality stocks that are set to outperform the market by 2x or even 3x in the next year.

But what I’m sharing with my 10X Stocks subscribers today could do much better.

In fact, I’m targeting gains of 500% in the next year, and potentially much more. And these stocks are in sectors you may not realize are in strong uptrends right now.

Oil & gas … precious metals … emerging markets … all of these are huge mega trends on my radar, and my top $5 stock picks cover all these bases and then some.

Not to mention, each of these stocks are rated a 95 and above, making them among the most promising stocks in this niche, $5 category that you won’t find anywhere in the S&P 500.

To learn more about 10X Stocks, click here now and check out my latest research.

To good profits,

Adam O’DellChief Investment Strategist, Money & Markets

Adam O’DellChief Investment Strategist, Money & Markets

Is the Big Mac “Recession-Proof?”

I mentioned yesterday that strong branding was critical to the success of Coca-Cola and Pepsi.

I don’t know if there’s a brand more recognized than the red Coca-Cola logo, though the Nike swoosh, Disney’s Mickey Mouse ears and Apple’s silver apple certainly deserve honorable mention.

If there is one corporate logo that can match Coke in terms of sheer recognizability, I’m going with McDonald’s’ golden arches.

I had that on my mind this morning as I was reading through the McDonald’s earnings release for the first quarter.

This is a tough operating environment for Mickey D’s. With the labor market as tight as it is, finding enough good workers at a good price is hard if not actually impossible. Inflation has been brutal as well, as higher food prices have been far worse than overall consumer price inflation.

McDonald’s hasn’t been immune, of course. Its customers are suffering from inflation along with everyone else. Yet the fast-food company managed to keep its margins strong by raising prices, effectively passing on its own cost hikes to its customers.

I don’t eat at McDonald’s often. I actually value my health. But I have been known to buy the occasional bag of cheeseburgers on a road trip, and I actually like some of their coffee drinks (don’t judge me!).

What impresses me is that, even after raising prices, McDonald’s is still cheaper than virtually all of its competition. It’s even cheaper than eating at home most of the time.

This is why, even when times are tough, McDonald’s tends to do just fine. Even when money is tight, you can generally afford a Big Mac.

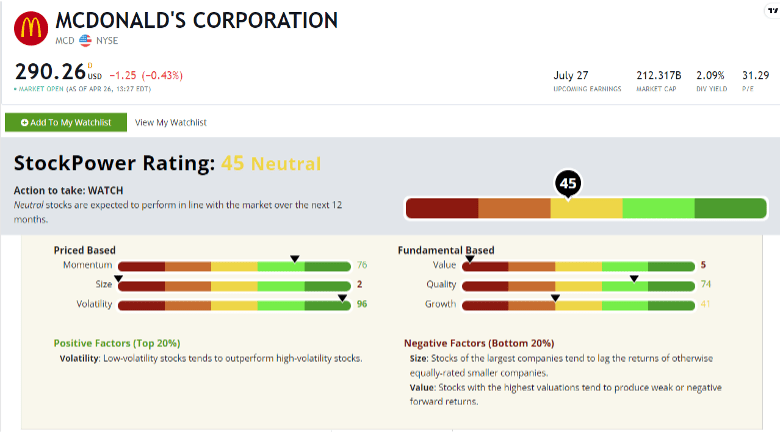

But since Adam O’Dell brings up the topic of quality, let’s take a look to see how McDonald’s stacks up.

McDonald’s rates a 74 on Adams’ quality factor, putting it ahead of nearly three quarters of all traded companies. The numbers confirm what I know to be true just from observation.

McDonald’s is a high-quality company that uses its unrivaled branding to generate consistently solid profits.

That’s great!

Of course, it also rates a 2 on size. With a market cap well over $200 billion, this is hardly a stock that will fly under the radar. But it also rates 5 on value, meaning that the stock is far from cheap.

This is a clear case of investors paying up for a high-quality name they know and trust. (Again, you’re paying for the brand.)

Overall, McDonald’s rates a neutral 45 on Adam’s Stock Power Ratings system, suggesting it should roughly return in line with the S&P 500 over time.

There’s nothing wrong with that, of course. But we can do better than that. And one way is via Adam’s focus on smaller companies trading for less than $5 per share. Today, you can find out which of his recommended small-cap stocks are ready to soar — up to 500% or more this year.

Regards, Charles SizemoreChief Editor, The Banyan Edge

Charles SizemoreChief Editor, The Banyan Edge