When was the last time you paid in cash? Counted the discarded pennies in your car’s cup holder? Asked to break a $20 bill in the checkout line?

Digital money transactions, or “contactless payments,” have taken over — both e-commerce and in-person shopping.

According to a recent Gallup poll, 64% of adults say the U.S. will be cashless in their lifetime.

From mobile wallets to digital currencies, digital transactions are sparking a contactless sales boom.

And this goes far beyond MasterCard, Visa or AmEx.

This game-changing financial technology (fintech) is a huge market. And it’s expected to soar by 100% in the next five years.

What Do I Mean by Digital Money?

When I say “digital money” and its payment transactions, I’m talking about:

- Mobile wallets: like PayPal, Apple Pay, Android Pay and Samsung Pay.

- Cryptocurrency & central bank digital currencies (CBDCs): digital currencies that are either decentralized (crypto), or are run by a central bank (CBDCs).

- Point-of-sale (POS) systems: that retail businesses everywhere are using to streamline the checkout process.

I’m sure you’ve noticed a change at your local restaurants, grocery and retail stores, even that taco truck on the side of the road. There’s now less cash and more digital payment transactions.

During a recent trip to the grocery store, I noticed not a single customer ahead of me in line paid with cash.

Most paid with their credit card, debit card or, of course, their smartphone.

There are three major ways digital money has become the future of business and finance. And I’m also going to tell you the best way to lock in real money from the digital money takeover.

Here’s how…

-

Mobile Wallets

If you’re unfamiliar with how quick mobile wallet payments work, Shopify, a popular online retailer, put it this way:

A mobile wallet is a digital wallet that holds credit, debit, ID, gift, membership and rewards cards on a mobile device.

Mobile wallets let consumers make payments using their mobile device, smart watches or tablet instead of using a physical card.

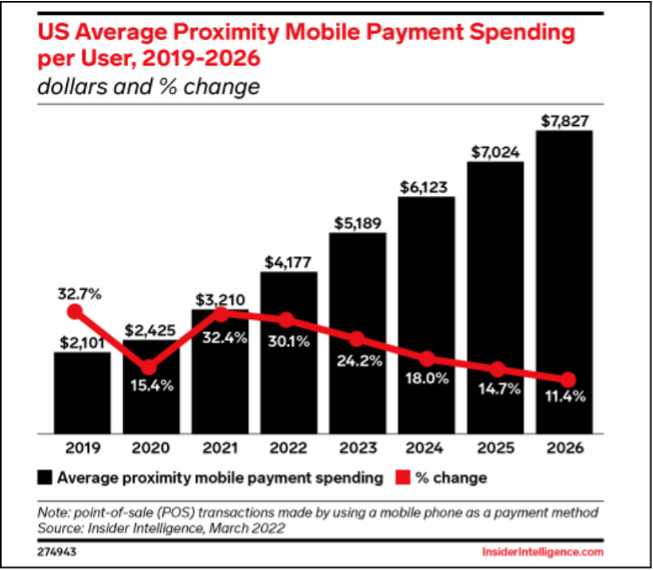

The use of mobile wallets is on the rise. In the U.S., per-user proximity mobile spending will nearly double to reach $7,827 in 2026, as customers shift toward mobile wallets and away from other payment methods.

With mobile wallets gaining in popularity, that means that in our 2.0 tech world, all you really need is your smartphone to make almost any purchase.

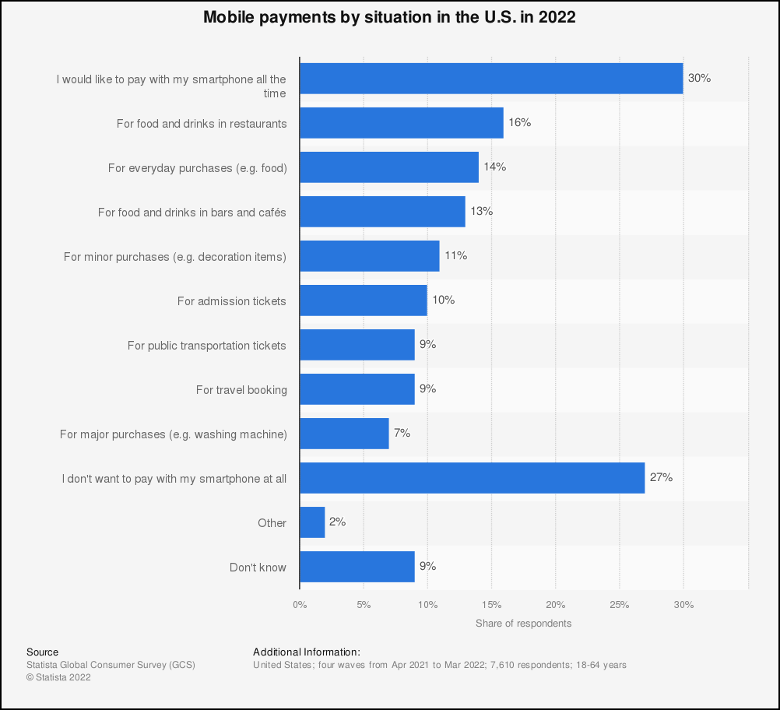

A Statista survey found that 30% of mobile wallet users like to pay with their smartphone all the time.

Wow. 30%! That’s a significant number.

And it’ll only grow from here, because 2.0 tech companies like PayPal and Tesla are leading a “new money revolution.”

PayPal & Tesla Are Steering Into Digital Moneymaking

With Black Friday and Cyber Monday less than 50 days away, overstuffed retailers are set to pull out all the stops to unload excess inventory.

High inflation and too much stock in their inventories are prompting retailers to offer steep discounts on their products.

A notable percentage of holiday purchases this year will be made using mobile wallet digital payments.

But it’s not just during the holidays.

For the last few years, PayPal has established itself as an industry 2.0 leader in the digital payment market.

Back on May 1, 2020, PayPal experienced the “largest single day of transactions in the company’s history — bigger than both Black Friday and Cyber Monday of 2019.”

And as for car sales, one of our model portfolio favorites — Tesla — is easily a front-runner adapting to this evolution in e-commerce.

Tesla’s online sales technology and seamless contactless deliveries are leading the future of automotive sales.

Tesla buyers have the option of “Express Delivery” or “Tesla Direct.” Both services are contactless and can be completed with no direct, face-to-face human interaction.

All that’s needed is payment through Tesla’s app on your smartphone.

This quick mobile checkout technology is growing by leaps and bounds. And it means big profits for us…

-

POS Systems & Contactless Payments

Also per Shopify: “With contactless payments and tap-to-pay becoming more popular in a post-pandemic world, accepting mobile wallet payments has gone from a bonus payment option to an essential.”

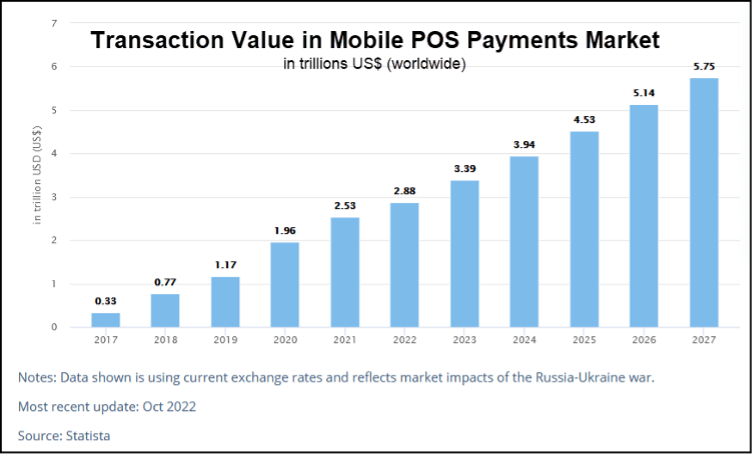

The transaction value of the global mobile POS payments market is projected to reach $5.8 trillion by 2027 from $2.9 trillion this year. This is a compound annual growth rate of nearly 15% and a 100% jump.

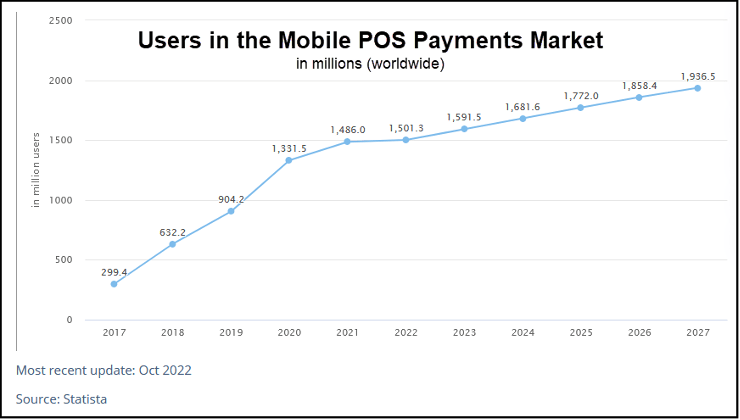

The technology is so popular that the number of people using it worldwide has more than tripled since 2017 — from 299 million users to 1.5 billion users.

By 2027, it’s projected that the mobile POS payments market will have 1.9 billion active users:

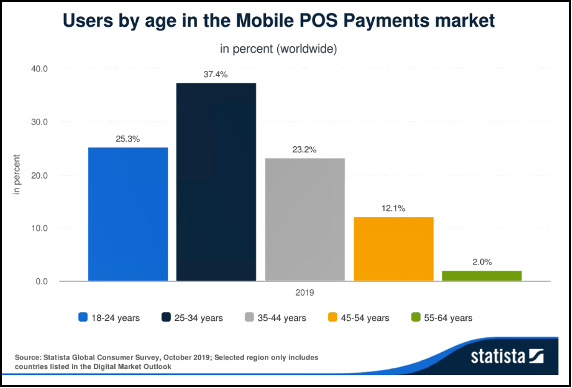

And remember: The mobile POS boom has legs to run for years to come. Millennials, the biggest 2.0 cohorts, use this emerging technology the most.

Currently, millennials account for 37.4% of mobile wallet POS transactions, followed closely by Gen Z users at 25.3%.

Our current global situation is accelerating the use and need for quick mobile checkouts and contactless sales transactions.

-

Cryptocurrency & CBDCs

We can’t talk about “digital money” without talking about one big divisive topic…

Cryptocurrencies like bitcoin, Ethereum and Solana are digital currencies. They’re secured on online networks called blockchains.

Cryptos are decentralized, meaning they aren’t regulated by any government entity or central bank.

This has made cryptos increasingly popular over the past 10 years, both as digital currencies and as investment assets.

On the other hand, central banks don’t want to be kept out of the loop. This is where central bank digital currencies, or CBDCs, come in.

The basic concept is:

- Less reliance on paper money.

- Reduced banking costs.

- A stable digital currency backed by the government.

Even the U.S. Federal Reserve is exploring the possibility of replacing the U.S. dollar with a CBDC.

The U.S. isn’t the only country taking this idea seriously, but Ian King and I are watching the Fed’s potential CBDC actions closely.

Why?

CBDCs sound like a good idea in theory. But a government-controlled digital currency would benefit the U.S. central bank more than it would benefit us.

According to our research, it would actually give it more control over your finances. And it could pose significant risks to your wealth and assets.

**Special Note: If you want to learn more, Ian is hosting a special webinar event on CBDCs this Thursday, October 13 — online for free. He’ll show you three ways you can protect your money from a U.S. central bank digital currency.

If you’d like to watch this event on Thursday (for free!), subscribe to the Winning Investor Daily newsletter today! We’ll send you an email with exclusive access online.

The Takeaway: Digital Payment Tech Is Here to Stay

Companies like PayPal and Tesla see that. They’re leading America in innovative, contactless sales with new-world technology front and center.

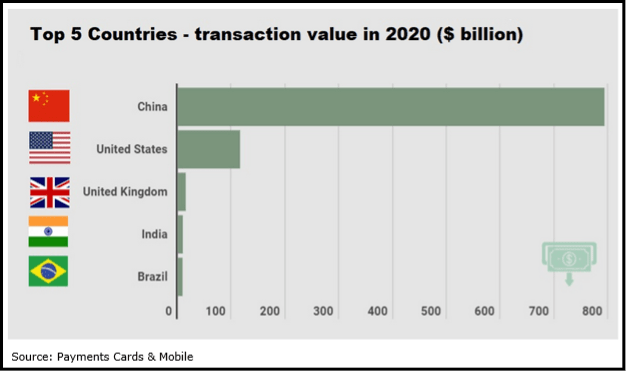

Right now, China leads the global mobile wallet movement. But not for long.

As industry 2.0 unfolds, the U.S. will gain market share. And companies fully embracing this technology stand to reap the profits.

Want to Invest in the Digital Money Trend?

To be part of this digital revolution, I suggest buying shares in the ARK Fintech Innovation ETF (NYSE: ARKF).

ARKF is an exchange-traded fund (ETF) that invests in domestic and foreign equities. These companies rely on (or benefit from) the introduction of new tech products or services.

These are the companies that can potentially revolutionize how the financial sector works.

If you have more questions about mobile wallets, cryptocurrency or even CBDCs, let us know in the comments below. Or send us an email at WinningInvestorDaily@BanyanHill.com!

Until next time,

Director of Investment Research, Strategic Fortunes

Disclaimer: We will not track any stocks in Winning Investor Daily. We are just sharing our opinions, not advice. If you want access to the stocks in our model portfolio with tracking, updates and buy/sell guidance, please check out Strategic Fortunes.