The first time I ever heard of digital currency was at an Occupy Wall Street protest.

You might remember the movement’s rallying cry of “we are the 99%!”

The initial event brought an army of angry and frustrated Americans to camp out in New York’s financial district in 2011.

They were protesting the government’s massive bank bailouts. And the equally oversized bonuses paid to top bankers.

Thousands spent two months camped out at Zuccotti Park.

So I walked down with some colleagues to see what the fuss was all about.

The place was anarchy.

Since many of the protestors were self-proclaimed anarchists, that part made sense.

Upon seeing me in a suit, they couldn’t wait to tell me what was wrong with Wall Street.

They had plenty of stories about why our current financial system wasn’t good enough.

But few of them seemed to have any meaningful solutions.

Until someone told me about bitcoin.

I’ll admit, I was skeptical at first. It sounded a bit like a libertarian fantasy.

Then a few years later in 2014, I read the whitepaper for Ethereum.

After that, I was hooked.

I’ve been tracking the sector ever since.

Cryptocurrency took off like a rocket after those initial Occupy protests over a decade ago.

It surged from obscurity to become a new trillion-dollar marketplace.

Bitcoin has soared from less than $30 to over $67,000 at its all-time high.

According to market research, there could be more than 320 million crypto owners by the end of 2022.

But there’s another new “digital currency” spreading all over the world.

And today, I’ll show you how this new currency could spell the end of privacy, prosperity and freedom as we know it…

Digital Currency: Crypto vs. CBDCs

This new kind of digital currency is nothing like crypto.

In fact, as you’re about to see, it has more in common with the dollars we already use.

It’s called a “central bank digital currency” (CBDC).

You’ve probably never even heard of it.

But governments and central banks all over the world are fast-tracking these new CBDCs.

There are currently 110 in development all over the world.

You can follow their progress on the Atlantic Council’s CBDC Tracker. As you can see, CBDCs are everywhere:

![]()

Despite the rush to get CBDCs up and running … there’s still not a clear answer on what we can expect.

The Bank for International Settlements (BIS) admits the term isn’t well defined, but that it’s “a new form of central bank money.”

CBDCs would be designed from the ground up to work with our high-tech financial system.

They’d be fully digital.

Unlike paper cash, which can be spent anonymously, digital currency could be fully traceable.

This means central banks could monitor, block or censor transactions.

Central banks argue that CBDCs are necessary to combat money laundering, fraud and financing terrorism.

White House officials claim a CBDC would enable “greater access to the financial system, boosting growth.”

The Fed says CBDCs would “level the playing field” and streamline transactions.

But is that really true?

After all, CBDCs would put the next generation of currency into the same hands that engineered record inflation and plundered the dollar’s value.

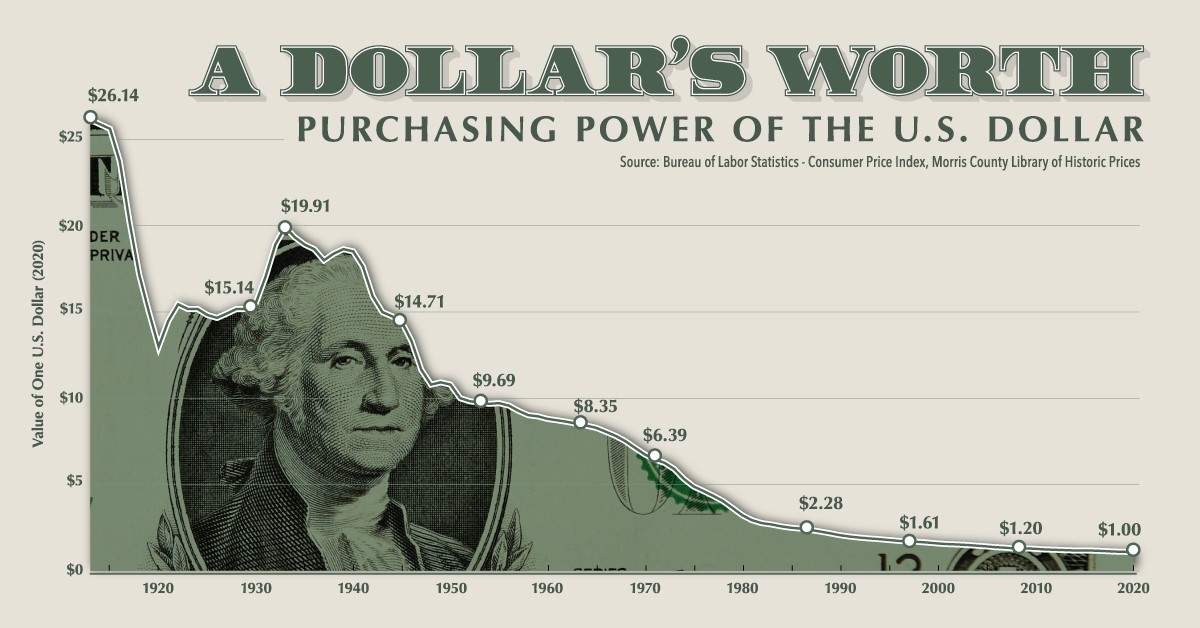

Remember, since the creation of the Federal Reserve in 1913, the U.S. dollar has lost over 96% of its purchasing power:

As you’ll see in just a moment, CBDCs would put even more power into the hands of central bankers.

That’s why experts at the Cato Institute are ringing the alarm bell.

They recently warned: “Central Bank Digital Currencies are incompatible with freedom.”

“The real danger in CBDCs,” they continued, “is that there is no limit to the level of control that the government could exert over people if money is purely electronic and provided directly by the government.”

The Manhattan Institute’s N.S. Lyons argues CBDCs “could represent the single greatest expansion of totalitarian power in history.”

Even credit unions and bank trade groups agree.

In a joint letter about CBDCs, seven of the industry’s biggest trade groups warned of the “devastating consequences for the cost and availability of credit for consumers.”

I realize this all might sound a bit alarmist.

But once you realize what’s possible with a CBDC, you’ll see why these experts are so worried…

The 3 Biggest Problems With CBDCs

As I’ve said before, our traditional banking system is embarrassingly outdated.

The same goes for our money.

Yet our current system, though outdated, has its advantages.

Because it limits the control central bankers have over your buying decisions.

Earlier this year, inflation was on the rise.

So Jerome Powell and co. cranked up interest rates to cool down spending and keep inflation under control.

If the Fed wants you spending money instead, it’ll start reducing rates.

So that leads me to the first big problem with CBDCs:

-

With a CBDC, central bankers have complete control over your dollars.

The Fed would instantly become the middleman for all your transactions, savings and investments.

All in the name of protecting you from fraud and bad actors, of course.

The Centre for Economic Policy Research (CEPR) says this would create “the temptation for authorities to steer credit directly.”

But with a CBDC, central banks have a whole world of options…

They could just put an expiration date on your “digital dollars.”

Either spend your money by a specific date — or lose it forever.

Sounds crazy, right?

It’s already a reality.

China’s new CBDC includes a programmable expiration date.

What about privacy?

Traditional cash is anonymous. Remember the phrase “paying under the table”?

You can forget about that with digital dollars.

Because…

-

CBDCs give governments a whole new level of tracking and visibility on how you spend your money.

![]()

Imagine giving Washington a digital database with all the serial numbers on your money. Then giving it the power to track those dollars through the economy.

That’s what a CBDC would do.

And it would give governments a treasure trove of data on spending and investments.

Earlier this year, we saw a glimpse of what the government might do with this new power.

It was back in January, during the “Freedom Convoy” protests in Canada.

Prime Minister Trudeau wanted the protestors gone.

So he announced he’d start freezing their assets.

Then his administration went even further — freezing the bank accounts of any donors to the protest.

At one point, a Canadian single mother even had her account frozen after chipping in just $50.

CBDCs would give lawmakers even more ways to invade your personal life.

To quote The New York Times: “As cash disappears from the economy, privacy disappears with it.”

And as some economists gleefully point out, CBDCs would allow for taxes on every transaction.

So paying your neighbor $100 for housesitting would suddenly be taxable. The $50 you loan your cousin at the game. Or the allowance you pay your kids. All of it.

And the last major problem with CBDCs…

-

There will be no way CBDCs hold their value.

CBDCs will still be controlled by central banks, just like fiat currency.

And just like fiat currency, you can expect them to lose value over time.

Because there’s no limit to the number of dollars the government might “print.” No limit to the bailouts or the stimulus packages.

There’s also what DoubleLine Capital calls the “Pandora’s Box” of CBDCs — runaway inflation.

According to DoubleLine, CBDCs could unlock high levels of liquidity. At the same time, it would increase the velocity of money.

That adds up to a one-two punch that “could bring about far more inflation than central bankers bargain for.”

So just to recap, a CBDC could:

- Give central bankers total control of your money.

- Destroy your financial privacy.

- Destroy your savings’ value.

Yet despite failing on all these fronts…

CBDCs Are Already Starting to Take Over

Like I mentioned, there are already 110 different CBDC projects rolling out all over the world.

Seventy-two are in research and development.

Fifteen are in the pilot phase.

And 11 CBDCs are already up and running.

The Bahamas’ “sand dollar” is one of them.

It accounts for less than 0.1% of all Bahamian cash though.

The IMF pointed to weak cybersecurity as a major liability for the new CBDC.

The organization also pointed out Bahamians have “limited avenues to use the sand dollar.”

Ultimately, the Bahamas’ project looks more like a publicity stunt than anything else.

Nigeria’s CBDC, on the other hand, was a matter of survival for those in power.

The African country’s residents are deeply distrustful of banks and governments.

Forty percent of them don’t even have bank accounts!

So when citizens started flocking to cryptocurrency, the government rushed to set up an “alternative” with the CBDC eNaira.

Nigerians have used the CBDC for $10 million worth of transactions since it launched last October.

We already talked about China’s CBDC, which is easily the world’s largest.

According to an Atlantic Council report from October 2021, there are 123 million individual wallets and 9.2 million corporate wallets.

The system is already faster than Visa. It can reportedly process up to 10,000 transactions per second.

Despite the impressive numbers, Atlantic Council is quick to point out: “It is still miles behind payment giants like AliPay and TenPay when it comes to scalability and speed.”

But it might still be enough to spark a CBDC revolution.

Experts at CEPR believe:

“With China already headed down the CBDC road, others now view it as too late to resist — even with full knowledge of the risks, they feel compelled to prepare.”

America isn’t that far behind either.

On March 9 of this year, President Biden signed Executive Order 14067.

This order lays the foundation for a new Fed-controlled CBDC.

So we could see “digital dollars” here in America sooner than you might expect.

In fact, work is already underway at the Federal Reserve on “Project Hamilton.”

There’s too much for me to go into here. That’s why I created a special, extended video report on CBDCs and Project Hamilton.

It’s going live tomorrow — so make sure to keep an eye on your inbox for more!

Would You Embrace a Central Bank Digital Currency?

How would you feel about doing away with cash forever and switching over to “digital dollars?”

It’s a big leap to take — and a question you might need to answer in the next few years.

I’m eager to hear what you think.

Send an email to WinningInvestorDaily@BanyanHill.com to let me know!

I’ll feature selected responses in this week’s issue of RAD on Saturday.

Regards,

Ian King

Editor, Strategic Fortunes