How we think impacts our investment returns.

Some investors are rather surprised by this. They believe profits result from buying low and selling high. But it’s actually their thinking that determines whether prices are low or high.

As an old trader once told me: “Prices are numbers on a screen. They aren’t high or low. We trade trends, not price.”

This is a simple market truth. But many of us fight it. We want to believe we know when prices are high or low. That’s due to our biases about market action.

Last week, I wrote about anchoring. This psychological bias influences buy decisions. You may see a stock trading at a new 52-week low and think it’s cheap. Your impression of value is anchored at the 52-week high.

Convinced that price is low, you buy. The stock keeps falling. You hold your shares. Now you are trying to avoid the pain of a losing trade, which I wrote about two weeks ago.

These interesting ideas may appear impractical at first.

But when we look more carefully, we see they really do have practical applications to the market. How investors feel is the most important factor defining stock prices. And there’s even a formula that explains exactly how this works…

Investor Opinions Set the Price

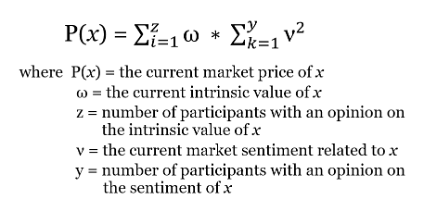

In the formula shown below, price (P(x)), is equal to the intrinsic value of a stock multiplied by the square of bullishness or bearishness of the average investor. Squaring the opinions makes that the most important factor in the equation.

This formula makes sense. If sentiment is extremely bullish, we may be in a bubble with prices completely disconnected from fundamentals. In environments where sentiment is extremely bearish, everything might look like a bargain, although it seems like no one is buying.

Let’s look at a specific example. Say a stock has an intrinsic value of $42.08. You know that because you completed a discounted cash flow analysis of the company. You estimated sales, operating costs, the cost of capital, interest rates and many other variables. Your work looks sound.

But the stock’s not trading at $42.08.

It might be trading at $29.04. That’s a 31% discount to the intrinsic value. This means the stock is undervalued to you, so you buy.

Notice that phrase “to you” in the previous sentence. The intrinsic value is your opinion. Other investors have a different opinion. It’s safe to say the majority believe the value is lower than $42.08, otherwise the stock would be priced higher.

Before buying, you should ask a very important question: Why is the stock undervalued?

Some investors never ask this. They buy undervalued stocks and watch the stock get more undervalued. They think of this as a buying opportunity. But if the stock keeps falling, it’s not worth buying.

Or the stock just doesn’t move. That’s also bad. A stock that doesn’t move is “dead money.” It’s money that’s not earning money. Since most of us have limited capital, so we can’t afford dead money. We need to own stocks that are going up rather than stocks that should go up.

Simply thinking about why the stock is undervalued could help avoid some losses or dead money.

Follow the Market Sentiment to Profits

The formula above helps us understand the reason why stocks are undervalued.

A large number of investors have a bearish opinion on the stock. They aren’t buying that stock, so that makes it impossible for the price to go up.

Remember, in that formula, opinions are squared. This makes feelings about the stock the dominant factor determining a stock’s price. Until opinions change, an undervalued stock can’t go up.

On the other hand, if opinions are bullish, the stock could be overvalued.

You may look at a stock’s price and know it’s not worth that much. Yet it keeps going up. In these cases, you’re right — the stock is overvalued.

But you aren’t making money in that stock because you allowed your opinion to overrule the market action.

With these simple examples, you see that opinions really are the most important factor in pricing. That’s a crucial investment lesson.

In July 2007, Charles Prince III (then CEO of Citigroup) explained how his bank was handling the obvious bubble in subprime mortgages. He said: “When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing.”

In stocks, market sentiment is the music. Whether it’s bullish or bearish, you should listen to the market’s music and dance like no one’s watching.

Regards, Michael CarrEditor, Precision Profits

Michael CarrEditor, Precision Profits

The Best Time to “Buy and Hold”

The S&P 500 is up around 20% this year. That’s a fantastic run, particularly after a brutal 2022.

You know me. I’m never going to tell you not to trade. If you think you can make money, go for it. That’s what markets are for.

But I’ll repeat that this is a trader’s market. By all means, ride this thing higher. But don’t buy, hold and pray.

And here’s why:

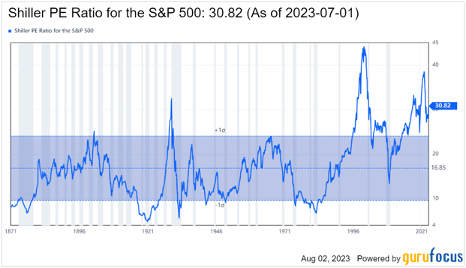

The cyclically adjusted price/earnings ratio (CAPE) is most certainly not a market timing model. If you are looking for an indicator that will tell you when to get in or out of a market trade, this isn’t it.

But the CAPE is effective at giving you a “quick and dirty” estimate of what to expect from buy-and-hold returns over the next 8 to 10 years.

When the CAPE is near the bottom of the blue zone, or ideally, below it, stocks are priced to deliver fantastic returns. This is when you really can buy and hold with confidence.

But when the CAPE is priced above the blue zone you see in the chart, returns over the following decade tend to be weaker. And today, the CAPE is well outside of those bounds. The good folks at GuruFocus ran the numbers, and calculated that returns in the ballpark of 3.5% per year are what we should expect at starting valuations like these.

Now, I don’t believe for one minute that returns will be exactly 3.5%. This is a broadsword, not a surgical scalpel. Meaning, this assumes that valuations revert to something resembling the long-term average. Perhaps returns end up being a few points better than that … or maybe significantly worse. Only time will tell.

But in my opinion, this is not an ideal time for a buy-and-hold strategy. When the expected return on stocks is actually lower than what is currently available in risk-free bonds, it suggests there are better alternatives.

My advice?

If you have a core of long-term stock holdings you intend to keep for years or even decades, you don’t need to run out and sell them. But keep a close eye on your lower conviction holdings and know when you plan to get out.

And with the bulk of your portfolio, consider being more active — such as with a short-term trading strategy.

Now, a short-term trade isn’t guaranteed to outperform. But let’s just say I like your odds better in an active approach, at least until market valuations come down a little.

If you want to learn more about the most effective short-term trades for your portfolio, this is where Mike Carr can guide you. Check out what he’s doing in his Trade Room right now.

Regards, Charles SizemoreChief Editor, The Banyan Edge

Charles SizemoreChief Editor, The Banyan Edge