Say you have a child or grandchild who just graduated high school.

He applies for a student loan for college, but he needs a co-signer because his credit score and income are low.

You offer to be that co-signer. It’s no big deal, right?

The next thing you know, you’re on the hook for tens of thousands of dollars in student loans.

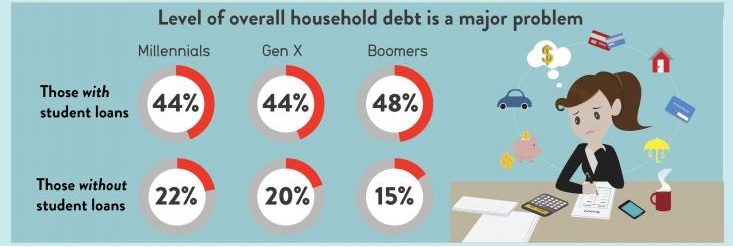

This scenario is more common than you think. The Federal Reserve reports 2.8 million Americans over the age of 60 have student debt.

And unlike other kinds of loans, you don’t get out of these by declaring bankruptcy.

The Trillion-Dollar Student Loan Crisis

The Association of Young Americans (AYA) and AARP recently did a joint study on the crisis of seniors stuck with student debt.

They found that 32% of seniors with student debt had to use their retirement savings to help pay off the loans. Thirty-one percent couldn’t buy a new home because of student loan debt.

Nine percent couldn’t even afford health care because of student debt.

“The trillion-dollar student loan crisis is clearly having a tangible impact on all Americans across all generations,” said AYA Founder Ben Brown.

(Source: AYA and AARP)

The average student debt is more than $40,000. And according to the Consumer Financial Protection Bureau, 37% of borrowers age 65 or older have defaulted on their student loans.

“It’s a really devastating phenomenon. And I’m seeing it destroy, literally wreck families across the country,” said Alan Collinge, creator of the advocacy group Student Loan Justice.

Risks of Co-signing Student Loans

If you’re a senior who defaults on a federal student loan, the government will find a way to get your money.

That can mean withholding tax refunds you’re entitled to. Or cutting a big chunk of your Social Security payments.

And defaulting on student debt wrecks your credit score. That makes it much harder for you to get a credit card, rent an apartment or apply for a home or auto loan.

So before you co-sign anything, please make sure you know what you’re getting yourself into.

Get all the details from the loan servicer. Learn what all of your options are for making payments. Remember that interest can cause loans to quickly spiral out of control.

And most importantly, if you aren’t sure if you can pay off the loan yourself, you need to have a plan. Talk with your child or grandchild about their expectations for paying off the loan, and don’t be afraid to discuss less-expensive options.

You shouldn’t have to work well into your golden years because student loans deny you the retirement you deserve.

Regards,

Jay Goldberg

Assistant Managing Editor, Banyan Hill Publishing