Article Highlights:

- German government 10-year bonds are currently yielding -0.51%.

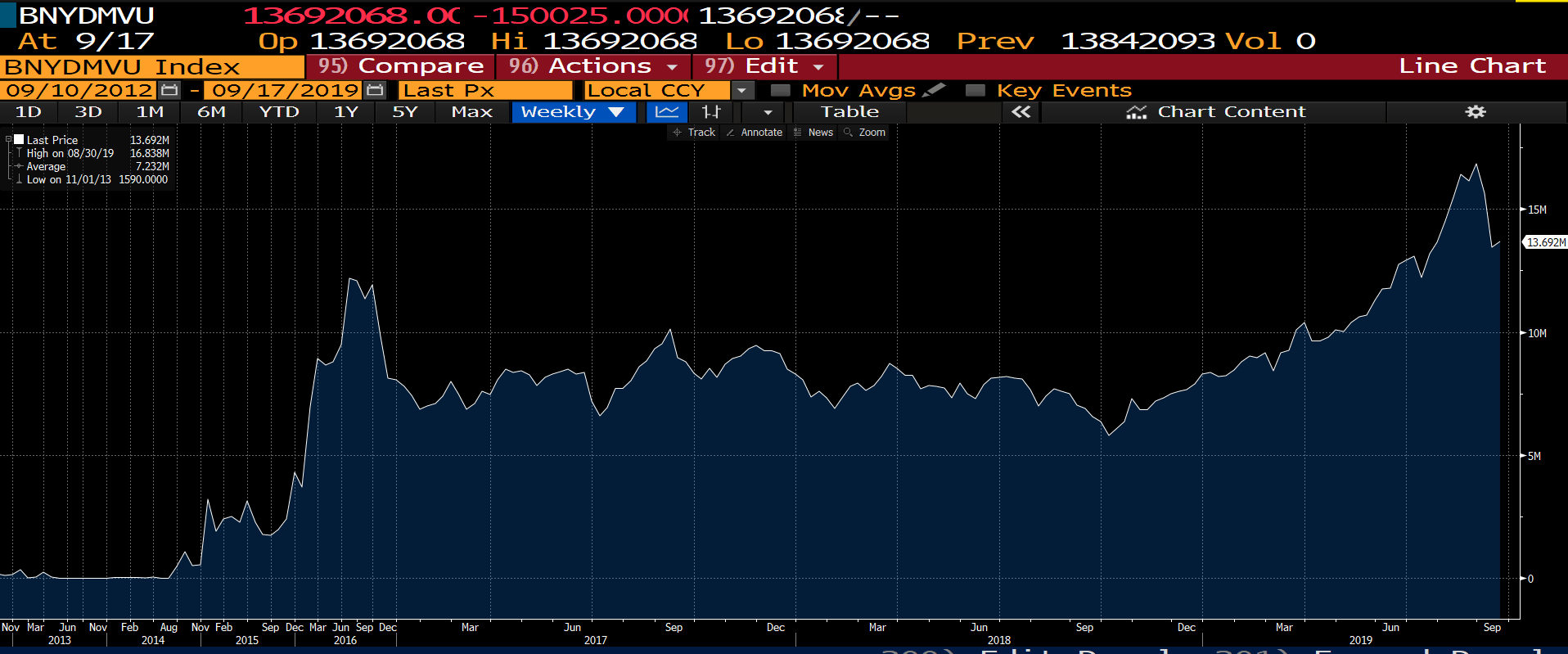

- Currently, $13.7 trillion of global bonds are trading with yields below zero.

- Capital-appreciation buyers follow the “greater fool theory” of investing.

Can you imagine a friend borrowing money from you and then telling you that the longer it takes him to pay you back, the less money he owes you?

He’s likely to quickly lose some friends that way.

But that’s exactly what’s happening in global bond markets.

This is the crazy idea that when you buy a bond, not only do you get no interest, but you lose a little bit of your principal the longer you hold it.

You see, if there’s more demand than supply for that bond, the price will go up. That’s just how the market works.

And if the price of the bond goes up, you have to pay a higher price to get the same coupon rate. When that happens, the coupon stays the same, but the bond’s yield falls.

If the price of the bond goes up high enough, the yield could fall into negative territory. This means that you lose money for allowing the borrower to hold your capital.

For instance, German government bonds with 10 years to maturity are currently yielding -0.51%.

If you lend your money to the German government for 10 years, it takes a small slice of your invested capital on an annual basis.

What’s happening right now in global bond markets has no historical precedent.

What Tools Does the Fed Have Left?

Currently, $13.7 trillion worth of global bonds are trading with yields below zero. That’s up 128% from September 2018’s tally of $6 trillion.

Central bankers don’t seem to see anything wrong, as global bond markets from Germany to Japan slide into negative-yielding territory.

In 2016, former Federal Reserve Chairman Ben Bernanke penned an op-ed titled: “What Tools Does the Fed Have Left?” In it, he wrote:

The idea of negative interest rates strikes many people as odd. Economists are less put off by it. … The anxiety about negative interest rates seen recently in the media and in markets seems to me to be overdone. Logically, when short-term rates have been cut to zero, modestly negative rates seem a natural continuation; there is no clear discontinuity in the economic and financial effects of, say, a 0.1 percent interest rate and a -0.1 percent rate.

And here’s where the former Fed head gets it wrong. In the bond world, there are two types of buyers:

- Yield buyers. These are your pension funds, insurance companies and mutual funds. Large institutional buyers looking to match their assets with their liabilities.

- Capital-appreciation buyers. These are your risk-parity hedge funds, speculators and macro tourists. Basically, anyone looking to make a quick buck in the latest bond rally.

Yield buyers don’t buy negative-yielding bonds. They can’t. They need positive yields to balance an asset/liability sheet.

They won’t pay the bank to hold their money while they owe payments to pensioners and insurance contracts on the other side of the ledger.

Capital-appreciation buyers will buy negative-yielding bonds if they think someone else will come along and pay a higher price. This is also known as the “greater fool theory” of investing.

The Greatest Fools

When bond markets sell off and yields rise, yield buyers don’t sell their bond portfolios. They’re willing to hold, as they’ve already locked in an attractive yield.

On the other hand, capital-appreciation buyers are like fickle teenagers trying to keep up with the latest trend.

If the bond that was purchased at a negative yield is now selling off, then the investor is losing money on both invested capital and the negative yield it bought. For speculators, this is a double whammy.

As the amount of global debt trading at negative yields increases, more of these capital-appreciation fools pile in. It becomes a self-fulfilling cycle.

The problem is the $13 trillion of such debt in the hands of investors betting on higher prices (and further drops in yields).

They’re not buying for income. They’re buying because they believe they can sell to someone else at a higher price. In other words, they’re looking for a “greater fool.”

And this scheme works as long as growth throughout most of the world continues to remain sluggish.

The only way for this cycle to reverse is if yields rise on positive growth and inflation prospects. At some point, bond yields are low enough that they convince investors to buy that new home or car while credit is cheap.

In that way, negative yields stimulate demand for credit, the lifeblood of the economy.

At some point, lower rates — even negative ones — will lead to global economic growth.

When this happens, the capital-appreciation buyers will all head for the exits at the same time. And they might all suddenly realize the greatest fool was in the mirror all along.

Regards,

Ian King

Editor, Automatic Fortunes