“These returns are pathetic,” my 92-year-old grandmother complained.

It was 2012, and she was referring to the bonds and CDs her local advisor pitched her on during their last meeting.

She lamented: “I’m in a real pickle.”

And then she, and her friends, began to recall the glory days of 15% bonds that they were able to get back in the 1980s…

She had held on to many of those bonds, relying on them for a steady income.

But now, 20 and 30 years later, they were coming due. And every $1,000 she made from those bonds was cut down to about $100.

A 90% pay cut put many people in a bind.

Interest rates were in a long-term decline and there wasn’t much anyone could do about it.

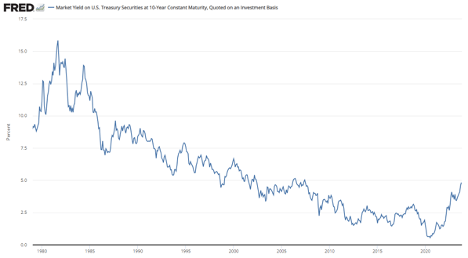

This is a chart of the 10-year Treasury yield.

For much of the last four decades, the 10-year Treasury paid over 5%. Which is why bonds were a very important part of every portfolio. The 60/40 portfolio (60% stocks, 40% bonds) truly made sense.

But, as yields fell, especially after 2010, the attraction fell too.

Thanks to the Federal Reserve keeping interest rates SO low for SO long, there has been no alternative to the stock market for the past 20 years.

The lame, single-digit returns from boring old bonds just didn’t compare to the flash and dazzle of stock market gains, particularly technology shares.

And let’s face it, nobody has ever started off a conversation in a bar with: “Let me tell you about this new bond I just bought.”

So, millions of Americans, with their billions of dollars, were forced to put their retirement into the stock market. So the stock market soared.

Over the last decade, it went up 100%. Then 200%. Then 300%.

And stock investors made a lot of money.

But now … for the first time in 20 years … many retail investors are taking a look at bonds again.

Vanda Research shows that inflows into the 20-year Treasury, as measured by the popular bond index fund TLT, hit $1.2 billion in the last quarter — the highest since 2010.

That followed a $746 million net inflow in the second quarter.

A lot of the urgency is coming from institutional investors. Think pension funds, seeking to lock in 5% returns.

All of this activity is quite logical.

Again, why invest in stocks, take on 100% risk and hope for an 8% to 10% annual return when you can take on 0% risk and get 5% in T-bills, plus the upside potential?

After all, bonds are guaranteed by the U.S. government.

Perhaps you are interested in buying bonds as well, especially as the stock market wavers week in and week out.

Yet, you are hesitant … because some of the news may seem conflicting.

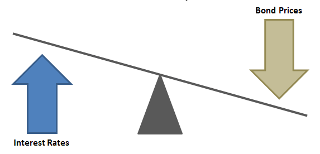

While yields are high, you’re simultaneously seeing headlines stating that bond funds are getting crushed.

That’s simply because as yields rise, bond prices, in the secondary market (where we trade them), fall.

Why?

Well, let’s say I bought a bond back in 2020. I would’ve paid $1,000 for the bond and received a 1% return. Sounds crazy, but that was the deal back then.

And let’s say I wanted to sell that bond today. Well, who would want to buy that now? Nobody. They can buy a new bond for $1,000 and get 4.9% a year.

So, I would have to drop the price of that bond down several hundred dollars in order for someone to be interested.

That’s why some “safe” bond funds, like the Vanguard Long-Term Treasury Fund (VUSTX), have fallen over 50%.

Ouch.

This is part of the reason I don’t like long-term bond funds. If interest rates keep going up, the price of the bond fund goes down.

The yield also lags in these bond funds. VUSTX only pays a 3.6% return, while the current 30-year Treasury pays a little over 5%.

I prefer buying the bond directly. Right now, the 10-year Treasury bond pays 4.9% … risk-free.

And it has 20% upside potential.

How does it have that much upside?

Well, bond prices go UP when interest rates go down.

For the 10-year Treasury, every 1% drop in interest rate results in a 10% increase in the bond price (roughly).

So, right now, you can lock in a 10-year Treasury with a 4.9% yield…

The worst-case scenario … you collect 4.9% a year for the next 10 years.

The best-case scenario … you collect the 4.9% a year, Jerome Powell lowers interest rates 2% and you make 20% profit to boot.

A Side Note: Anyone who followed last week’s recommendation to invest in the preferred shares of Office Property Trust (IPINL) saw the benefit of this. Such as Dave, who said he’s in for 200 shares. Good job Dave. You’re up about 10% already. Not shabby for one week! Well done!

But will the Fed lower the rate?

Big-name investors think so…

Bill Ackman, the founder of Pershing Square Capital Management, recently made a $200 million profit betting that bond prices would fall. But last week he closed that trade, stating that “the economy is slowing faster than recent data suggests.” In other words, expect interest rates to down.

Ackman is not alone in this thought. Jeff Gundlach at DoubleLine Capital now recommends “long-term Treasury bonds for the short-term trade going into a recession.”

And Bill Gross, the “Bond King,” states that “regional bank carnage and recent rise in auto delinquencies to long-term historical highs indicate U.S. economy slowing significantly … recession in the fourth quarter.”

Point is, if a recession comes, the Federal Reserve will stop raising rates and may even cut them.

How can the expert investors … Bill Gross, Bill Ackman and Jeff Gundlach … be so certain a recession is coming?

Probably because they’re looking at the data … and we should too.

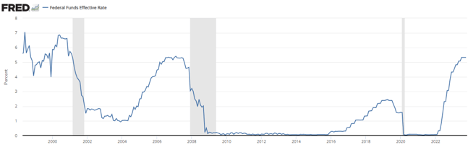

This is a chart of the Federal funds rate.

See the gray areas?

Those are recessions.

Every time the Fed increases rates sharply (2000, 2006, 2019), a recession follows.

And then, they cut interest rates:

- In 2001 they cut it 7%.

- In 2008 they cut it 5%.

- In 2020 they cut it 2%.

This is not rocket science, folks.

Managing recessions is the reason the Fed exists, after all.

If the Fed were to panic over, say, a deep recession, it might vote to cut rates by a cumulative 2% over a few months.

That 2% cut in rates implies a 20% gain for holders of 10-year bonds.

That’s on top of the regular 4.9% interest it pays out.

It’s a win-win.

I know people have taken it on the chin in the last year or so thanks to heavy bond weightings in their portfolios.

A QUICK NOTE: As I was writing this article, a friend sent me this troubling note…

My wife has a separate retirement account, an old 401(k) that we self-direct. She’s more risk averse than I am, so we set it to a basket of investments that essentially follows the 60/40 rule — 60% bonds, 40% stocks.

I knew her account would be down a fair bit due to rate hikes and the impact on bond prices, but, I was a little surprised at just how much the 60% bond portion had actually fallen.

I began to seriously ponder, how … or even if … there was any way I could regain that ground without having to wait two, five, 10 or even 15 years for bonds to recover.

Many of you may be in the same position. If so, it underscores the importance of paying attention to the insight we provide at Banyan Hill. We have never recommended bonds in the last decade. Not once. Not until, today … read below to see which bond I just purchased.

Again, that’s why I don’t like bond funds.

Instead, I prefer to own bonds directly.

I recently purchased a bond, CUSIP 91282CHV6. It pays 5% and matures on August 31, 2025.

I consider this a Zone 3 opportunity.

Low risk, low reward.

But very close to a low risk, high reward.

Worst case scenario: I make a 5% annual return and collect a small premium when the bond matures.

Best case scenario: Powell lowers interest rates and the price of my bonds go up 10% to 20%.

What About You?

Are you investing in bonds? If so, what kind?

Let’s start a conversation. Send me an email at AaronJames@BanyanHill.com.

Next week, I’ll address a real hot topic: bitcoin.

As you may have heard, bitcoin recently surged amid speculation about Blackrock’s approved exchange-traded fund … rising about 100% over the last year.

Before I start writing, I’d like to know your thoughts. Are you investing in bitcoin, or taking a pass? My team set up this simple poll for you to take so you can share your opinion.

Aaron James

CEO, Banyan Hill Publishing and Money & Markets

P.S. One of my team members, Michael Carr, just released his Apex Profit Calendar. It leverages AI to analyze and follow the “seasonality” of stocks — to help you buy the right stock at the right time. Want to get his next Apex Alert?