Fourteen months ago, the headlines for General Electric Co. (NYSE: GE) were terrible.

Too much debt.

Ineffective leadership.

No growth.

But sometimes a stock’s real story isn’t so obvious at first glance. You have to dig a lot deeper.

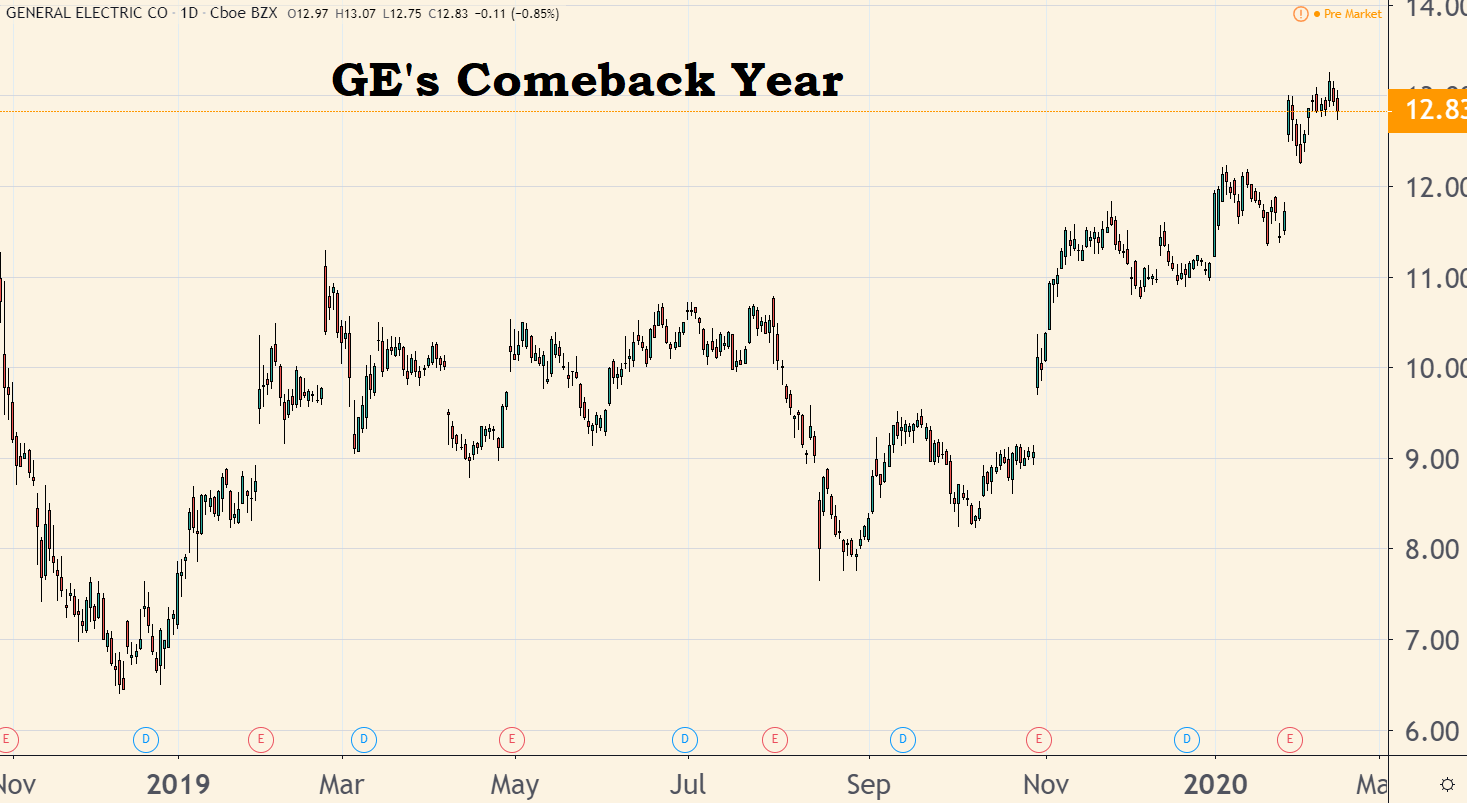

That’s why, back when the stock was at $7 and change, I said shares were a good buy.

Since then, GE is up more than 80%.

(Source: TradingView.com)

Its gains outpace nearly every stock of similar market cap, including Microsoft (70%), and are almost equal to Apple’s huge move (85%).

I suggested buying the stock several more times since then, even as recently as December.

With the stock up 22% in the past two months, I still think you should buy shares if you don’t yet own them.

That’s because I expect GE to rise another 30% over the next 18 months. And I have four reasons why.

Reason No. 1: We Need More Power

In GE’s latest earnings report, there’s evidence the company’s underperforming power division is finally turning the corner.

The unit managed to post an operating profit of $386 million in 2019, after posting an $800 million loss in 2018.

And according to veteran utilities analyst Hugh Wynne of Sector & Sovereign Research, there’s a huge new purchasing cycle just ahead.

That’s because annual global power plant new capacity is set to nearly double between now and 2035.

Reason No. 2: Our Aircraft Fleet Is Aging

With Boeing’s 737 Max remaining out of service and a slowing global economy, you’d think GE’s jet engine unit would have troubling 2019 numbers.

Yet the division posted a 5% increase in operating profits compared to 2018 levels.

Looking to the future, there’s a legion of aircraft out there now reaching the end of its 20- to 30-year lifetime.

After so many years, these jets need to be taken out of the fleet and sent to a desert boneyard.

Researchers at Alton Aviation Consultancy predict that the number of yearly plane retirements will roughly double over the next decade, from less than 600 annually now to around 1,100 by 2028.

And with 28,000 aircraft in service right now, the same researchers expect the overall size of the global fleet to grow nearly 4% a year, reaching over 44,000 in the next decade.

Reason No. 3: Plenty of Cash

These two developments are having an impact where it really counts — in GE’s free cash flow.

More cash means the ability to pay down more debt. It also means GE can raise its dividend down the road, after cutting it to almost zero in 2018.

GE posted a free cash flow of negative $3.5 billion in 2018, meaning the company didn’t generate enough revenue to supports its business.

But last year, its free cash flow improved to positive $1.2 billion.

Wall Street analysts expect that metric to more than double this year to $3.1 billion, rising still further to $4.3 billion in 2021.

Reason No. 4: GE Is Returning to Its Glory Days

Lastly, another way to measure if a turnaround company has actually started to turn around is by looking at its gross profit margins.

This measures the percentage of money a company retains from each dollar of revenue after subtracting its costs.

According to GE’s latest results, its gross margins reached 26.45%, after bottoming out at 23.8% in 2018.

Yes, it’s still a long way from GE’s glory days, when it posted gross margins in excess of 50%.

But the company’s turnaround is really only a year old. Analysts expect its gross margins to continue rising into the mid-30s in the next two years.

The point is, GE’s turnaround is for real.

All it takes now is buying the stock — and patience to let its story play out.

Best of Good Buys,

Editor, Total Wealth Insider

P.S. I have readers of my Total Wealth Insider service positioned in a number of turnaround plays. These are companies that Wall Street hates now, but will soon be buying hand over fist. With my Total Wealth strategy, we always beat it to the punch. To learn more, click here.