On August 2, 216 B.C., Hannibal’s Carthaginian army inflicted one of the worst defeats in military history on the Roman army.

Hannibal’s victory was the result of a brilliantly counter-intuitive tactical strategy.

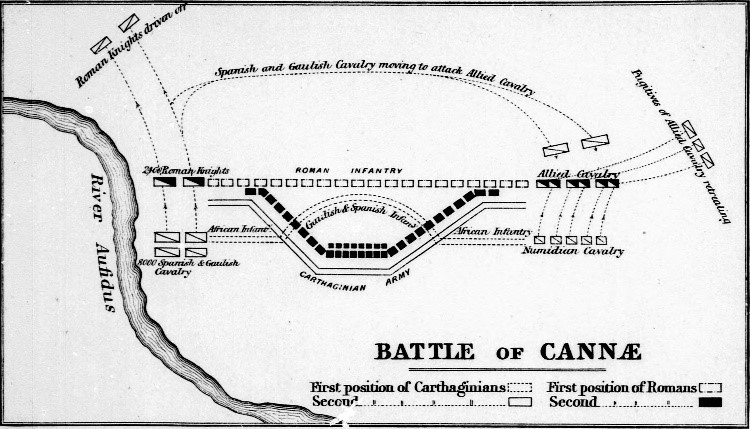

His initial dispositions were conventional: Heavy infantry in the center and mobile infantry and cavalry on the wings.

But when battle was joined, Hannibal did something unexpected.

Instead of pressing the attack against the Roman center, Hannibal ordered his heavy infantry to fall back from their initial echelon formation. They formed a funnel with the mouth pointed toward the Romans.

Thinking they were winning, Roman commanders Lucius Aemilius Paullus and Gaius Terentius Varro ordered their troops to advance.

As their legions advanced into the pocket formed by the retreating Carthaginians, Hannibal’s flanking forces advanced and encircled the Romans.

Seventy thousand legionaries died that day. The Roman Republic teetered on the brink of collapse.

Hannibal understood something that wise investors should remember in 2019.

The surest way to defeat an overconfident adversary is to lure them into a trap by appearing to retreat.

It’s starting to look like the Federal Reserve is doing exactly that to investors…

Investors Returned to Bull Mode

Of all the things that determine the price level of the U.S. stock market, interest rates are both the most — and least — important.

It depends on the time frame.

Chairman Jerome Powell’s announcement on January 30 that the Fed would pause its interest-rate hikes was all investors needed to return to bull mode … at least for the short term.

Low interest rates are good for the stock market. They make even modest stock and dividend yields seem more attractive. That draws in more investor money, boosting stock prices … again, in the short term.

But the stock market isn’t the economy.

The economy influences the stock market via corporate performance, especially earnings.

Increasing corporate earnings suggest the economy is healthy. That encourages investors to buy stocks in anticipation of future earnings. That pushes up stock prices.

But if earnings are falling, even low interest rates can’t keep stocks moving in an upward direction.

That’s why it’s important to be clear about what’s driving short-term stock market movements.

If it’s only removal of the threat of interest-rate hikes, rising stock prices could end — quickly.

An Earnings Recession?

Last year, analysts predicted that first-quarter 2019 profits for S&P 500 Index companies would grow by an average of 11%.

They are now predicting that the first quarter of this year will see the first year-over-year decline in profits in three years … -1.2%.

Some are even predicting an “earnings recession” — year-over-year earnings declines in the first two quarters of the year:

Lucky U.S.!

Why would we see rising stock prices and declining earnings?

It comes back to short vs. long term.

U.S. stock prices have enjoyed an unusual confluence of positive factors over the last decade, some long term, some short term:

- Long term: Extremely low interest rates in the wake of the 2008-2009 financial crisis have had the effect I described above, as well as reducing the cost of capital to U.S. companies.

- Long term: The de facto globalization of labor markets has allowed U.S. companies to keep wage growth down even with historically low unemployment.

- Short term: The Trump tax cuts of 2018 provided a massive cash windfall to U.S. corporations, which artificially boosted their earnings for the first three quarters of last year.

From 2010 until 2018, U.S. corporate earnings rose simply because the economy was recovering from a crisis, while costs were at rock bottom. Earnings always meant profits.

Indeed, increasing earnings with flat costs translated into an unusually rapid increase in profits for U.S. companies, which has boosted stock prices:

Between 2010 and now, those increased profits were essentially “free.” They were the result of natural recovery from crisis and flat costs thanks to low interest rates and globalization. Under those specific conditions, earnings always meant profits.

Those profits weren’t the result of investment in increased productivity and innovation. Outside the technology sector, gross U.S. fixed corporate investment has been below the long-term average since 2010.

So, if they weren’t investing, what did U.S. companies do with those profits? They used them to buy back shares.

The value of share buybacks was already high before last year, but the Trump tax cut sent them through the roof:

And buybacks, of course, boost stock prices.

Don’t Be Suckered In

Here’s what I think is happening.

Both the outstanding corporate profits and bull market of the last decade depended crucially on low interest rates and flat labor costs. The combination allowed companies to grow their profits in line with earnings.

But that’s not the normal scenario. Usually, costs rise as the economy strengthens.

Eventually, this pattern must end, even if interest rates remain low.

Labor costs will not remain low forever:

- Increasing import tariffs are already reducing the earnings and profits of many companies.

- Turmoil associated with Brexit in Europe will have a negative effect on the global economy.

- The Chinese economy is slowing.

In other words, we’ve reached the end of the recovery phase of the post-2008/2009 era.

Corporate costs will rise. Increased earnings won’t always produce profits as they have over the last decade. That means stock prices will not continue to rise as they are now.

Despite this, many people tell investors the stock market is once again booming, and they should all pile in. Interest rates are low … that’s all that matters!

That’s a mistake.

Like the Romans at Cannae, they mistake the Fed’s short-term retreat on interest rates as a permanent victory over a bear market.

But if a bear market comes, it will because of fundamentals like rising costs, not interest rates.

Just like the Romans, rushing into the market based on that mistaken assumption could be deadly!

Kind regards,

Ted Bauman

Editor, The Bauman Letter