Article Highlights:

- The top 1% of U.S. households now earn about 25% of the national income.

- That means further interest rate cuts could make things dramatically worse.

- It’s time to follow the “smart money” and reap some defensive profits in case of the next recession.

The world’s central banks have no idea what they’re doing.

That means in the next market slump, you’re on your own.

Are you ready?

At Friday’s policy conference in Jackson Hole, Wyoming, Federal Reserve Chairman Jerome Powell said: “There are no recent precedents to guide any policy response to the current situation.”

The current situation, of course, is a slowing global economy, a raging trade war, historic levels of debt and minuscule inflation … all in an environment with the lowest interest rates in history.

Everyone — especially President Donald Trump — expects the Fed to prevent the next recession and keep the bull market going.

But Powell has let the cat out of the bag.

He knows that further interest rate cuts aren’t going to do anything for the global economy or for the stock market.

In fact … they could make things dramatically worse.

But he’s probably going to be forced to cut rates anyway.

It’s time to get ready for the consequences.

Pushing on a String

In current economic conditions, further interest rate cuts are pointless … and possibly counterproductive.

Here’s an example that explains why.

When I was a kid, I lived in an old house a couple of miles from town. It was surrounded by farms.

Imagine I had set up a lemonade stand at the end of the half-mile driveway to the nearest road. A car might pass every 20 minutes or so.

The entrance to our driveway was on a bend and hard to see. Even if they saw me with my lemonade, at most three or four drivers would have bought a cup each day.

Now let’s say a local bank offered to lend me hundreds of dollars to buy lemons, sugar, containers, coolers and ice for my store. Would it make sense to take that loan?

Of course not. It wouldn’t make sense at any interest rate … not even a negative rate. There simply wasn’t enough demand for lemonade to justify a financial obligation I probably couldn’t meet.

That’s essentially what’s happening in today’s global economy — so cutting interest rates hasn’t had the desired effect.

The bulk of the “easy money” pumped into the global economy since the 2008 financial crisis has found its way into the accounts of corporations, banks and wealthy investors. Because they already had substantial assets to use as collateral, they could easily obtain loans at extremely low interest rates.

But because there haven’t been many profitable investments to make — like with my lemonade stand — they’ve used that money to speculate in asset markets, such as stocks and bonds, and to repurchase their shares.

By contrast, very little easy money has found its way to small businesses. That’s because banks are smart: They analyze how much “lemonade” a new business can likely sell, and if it’s not enough to repay the loan, they don’t make it.

In conditions like these, lowering interest rates further is like pushing on a string. You can push all you like, but whatever is attached to the other end isn’t going anywhere.

Inequality Broke Interest Rates

Interest rate cuts don’t work the way they used to because the structure of the economy has changed dramatically.

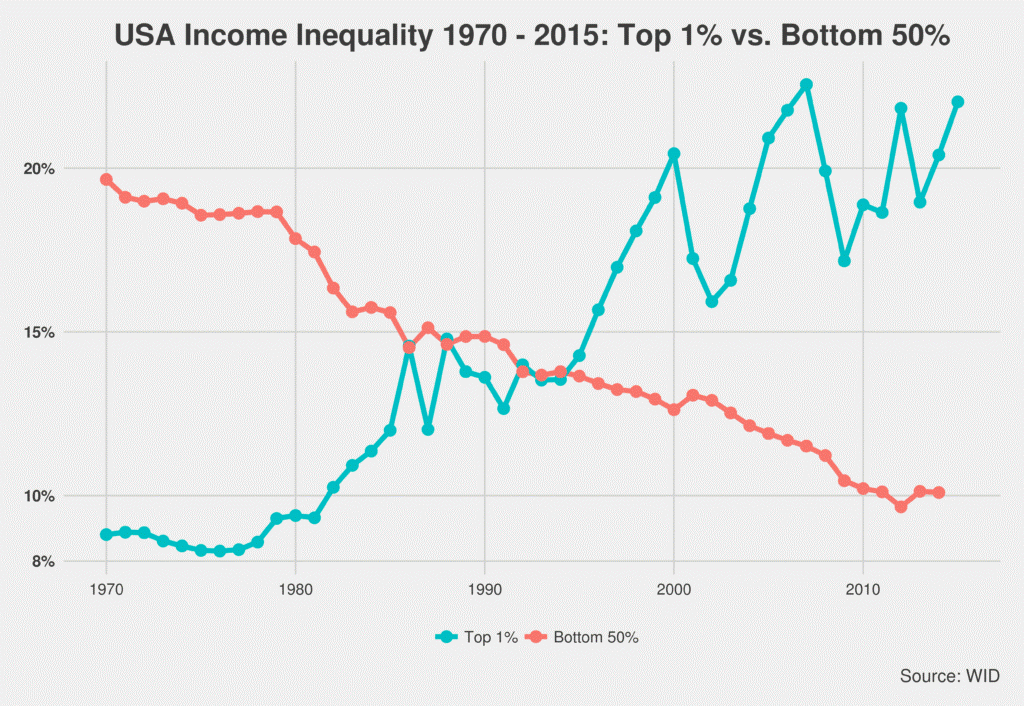

At the beginning of the 1970s, the bottom 50% of U.S. households earned nearly 20% of national income. The top 1% earned about 9%.

Now the figures are 10% and 25%, respectively:

In the old days, when the Fed cut interest rates, banks could increase their lending to Main Street American businesses and households because they knew businesses would have customers, and households earned enough to repay their loans. That made interest rate policy an important tool.

Nowadays, when the Fed cuts rates, banks shy away from lending to Main Street because they know incomes remain low. That limits the potential demand for new businesses.

They also know that many households are already over-indebted because they’ve gorged on cheap debt already.

So instead of boosting economic activity, cutting interest rates these days just leads to further inflation in asset prices as borrowers with plenty of collateral use cheap money to invest in stocks, land and share buybacks.

It Could Be Worse

In conditions of extreme inequality, low interest rates cause asset price inflation, threatening bubble conditions and the next recession.

Low rates also mean retirees invested in bonds and other fixed-income assets receive less money. So they spend less, slowing the economy down. That’s a big problem these days, as the proportion of retirees in the population is growing rapidly.

My research tells me Wall Street’s already aware of this problem. In fact, it’s already preparing defensive positions — stocks in companies such as McDonald’s, Walmart, Coca-Cola, O’Reilly Automotive and other purveyors of low-price consumer essentials. Because even in a recession, people need to eat, drink, clothe themselves and keep their cars running.

But you don’t need to buy all those companies individually. The Consumer Staples Select Sector SPDR Fund (NYSE: XLP) holds most of them.

So while the Fed pushes on its interest rate string, follow the “smart money” and get ready to reap some defensive profits.

Kind regards,

Ted Bauman

Editor, The Bauman Letter