2022 looks to be an interesting year for investors: a swift market rotation, continued inflation woes, volatility, midterm elections and at least three wild cards in the mix.

To survive and thrive through it all, you must start with the big picture.

Then you drill down to find the big profits.

That’s what Ted Bauman and Clint Lee do for you in this first 2022 edition of Your Money Matters. Watch now to hear what both expect of this year and the six exchange-traded funds they recommend.

Are You in for a Bumpy Ride?

Spoiler alert: Strap in! This year is going to be wild. Not least because of the upcoming U.S. midterm elections. According to Yahoo, if you look at the past 71 years, the “S&P 500 is very choppy for the first nine months and one might find the bull momentum is gaining traction only in early November.”

It’s events like this that encourage more questions than answers…

But that’s why Ted and Clint are here to help you understand what’s happening and what could lie ahead.

Click here to watch this week’s video or click on the image below:

VIDEO TRANSCRIPT

Ted: Hey everyone, it’s Ted Bauman here, editor of Bauman Daily and of The Bauman Letter. Just before we start today’s Your Money Matters videos, I’d just like to point out that I’m going to be doing a special live video where I’ll be responding to questions people can post to me on my YouTube channel this Friday at 2:00 p.m. ET.

So make sure that you log into that. You can sign up to get notifications for it and things like that. But basically, it’ll be an opportunity to pick my brain or throw darts at me or whatever it is you want to do, on Friday at 2:00. So now, let’s have a look at Your Money Matters.

—–

Angela: Happy New Year, and welcome back to Your Money Matters. After a brief holiday hiatus, we are back. I hope you enjoyed yourselves.

Before we get started, as a reminder, if you want more information about The Bauman Letter, there’s a link above, where you can get all the details on how to join, and everything that’s waiting for you on the other side. Our guiding principle here at The Bauman Letter is big picture and big profits.

Now, anyone who recommends stocks, invests in stocks, has a big picture that informs all of their decisions. Here at The Bauman Letter, we’re very fortunate, because we take a look at the big picture, and we have a renowned economist doing that job for us, very fortunate for all of us. We start with this big picture, and then we drill down to the best ways to play those big themes, the global stock markets, economic trends, that sort of thing.

Seeing as how it is the beginning of a new year, I thought it would be a great opportunity to talk about the big picture, as we head into 2022, and some of these big themes that will affect the stock market inevitably. I’d love to hear from you, Ted and Clint, but Ted let’s start with you.

Ted: Yeah, well, I mean, obviously it’s going to be a different year this year. We have a whole bunch of things that have changed, but my number one assumption for the year is that we’re going to see smaller overall level returns and that they’re going to be harder to find. There’s two reasons for that. One is that there just aren’t any more catalysts to make assets that are already highly valued relative to history go any higher than they are. I mean, the Fed, everybody said, “Don’t fight the Fed.” Well, it works both ways. The Fed’s pulling back now, but interest rates are going to go up. Also, just the liquidities. It’s just going to start evaporating. I think, just don’t expect to see these 60-70 P/E ratio startup stocks performing well this year.

The second thing is that the combination of slowing growth and high inflation means that earnings are going to rise more slowly. If you take those two in combination, my expectation is that we’ll see a rotation from the high multiple speculative stocks that did so well, particularly at the end of 2020 and the beginning of 2021, but to a certain extent last year, like some of the high flyers. That’ll rotate instead to value, especially value relative to earnings and to the value of the company’s assets. Companies that are generating lots of cash flow and that are producing good earnings but are relatively inexpensive, compared to their peers, that’s where the action’s going to be.

On that same note, I think defensives, like staples and telecoms and big pharma will probably do well, so will energy, especially fossil fuels, but at least in the short-term because, as we know, in the long-term, we’re looking at moving towards renewable energy, but I do think in the short-term, you’ll probably continue to see a big jump in energy stocks.

I think volatility’s going to increase. It’s going to be more of an up and down year, especially as passive indexes reduce their exposure to some of the overvalued stocks that we’ve seen and as earnings begin to pull back at some of the big heavyweights. I think people will start buying VIX options again, and that’ll become a way to make money the way it was a couple years ago, but a dangerous way.

Of course, the big macro issue this year will be inflation, especially in the first half of the year. I think the market has already priced in things like monetary tightening, interest rates, and what’s happening in Washington, but inflation is inherently unpredictable because there’s so many variables involved, if the Chinese economy slows down, if there’s shipping problems. All that kind of stuff, you just can’t predict.

Since I expect that speculative stocks will de-rate, i.e., people won’t be willing to pay high price-to-earnings ratio and overall growth will slow, the key thing for individual stocks will switch from macro things to micro. In other words, it’s not about what the Fed’s doing. It’s whether this company is making money and whether it’s able to keep that money and not have to spend a lot of money to make money, so profitability and margins will become critical this year, and I think dividends and other forms of yield, actual things like free cash flow yield, will become more important, as that’s what investors, smart investors, will be looking for, because that’s what the market’s going to reward.

Last thing on the predictions front is that I think the midterm election cycle could have a big impact on the market this year, but it could go either way. If it looks like the Republicans are going to basically win back both houses of Congress quite easily, then stocks that benefit from a hands-off government that’s not going to do anything, basically, could do well. On the other hand, stocks that rely on the government passing incentives to, like renewable energy, they could suffer. If the elections are close, and if there’s conflict over the conduct of the elections, as we know it’s gearing up to happen in a lot of states, there could be a lot of disruption. I haven’t seen any discussion of that in the financial press, but it could really be a big issue in the third quarter of this year.

In terms of recommendations, I think companies exposed to rising input costs, whether that’s from labor or materials, they’ll be under pressure, but companies with pricing power, those that can raise their prices to match their input costs and still get people to buy their stuff, they’ll do well. On the other hand, companies with low input costs, particularly software companies that software is a service, they’ll do well, as long as they’re growing their profits. I’ve got two ETFs on that front. One is the Morningstar Wide Moat ETF, MOAT, and the other one is First Trust Cloud Computing, SKYY. I specifically chose those two, because of low expense ratios and relatively good returns over the last year.

The second set of recommendations really involve, if you’re seeing a derating in the U.S., people are going to be looking for rising multiples elsewhere. That means you’re up in Japan, I think. I think emerging markets could do well, but it depends on what happens with interest rates. If interest rates rise rapidly for any reason, if the Fed decides to ride, that could put pressure on those companies because of their U.S. dollar denominated debt. I think China will continue to be a wildcard because of the current political and policy upheaval.

My next two ETF recommendations: first is the SPDR portfolio, Europe, ETF SPEU. I think Europe is poised to do well. I think that they’re going to go through a bad COVID winter, but things will get better. The only wildcard there, of course, is Russia and the Ukraine, so keep an eye on that. Then in Japan, my favorite ETF there is the WisdomTree Japan Hedged Equity Fund, DXJ, and that’s because they make sure that they hedge for the currency risk, the dollar versus the yen. There you go. There’s four ETFs from me.

Angela: Those last two, you suggest, maybe keeping a closer eye before pulling the trigger on them?

Ted: I would say, just keep an eye out. I think the tailwinds for Europe are obviously that once COVID normalizes, because I think what we’re heading for is COVID becoming endemic. Once most people have it, then they’ve had it, and maybe they’ll get it again, but it won’t be such a big deal, but that’s got to happen first. You’ve got to watch that and then poise yourself, but already European stocks are looking better. They’ve done better over the last quarter than they had previously, mainly because people are moving away from the expensive U.S. market in anticipation.

The other thing is to watch with Japan. I think Japan’s pretty stable. Obviously, the big issue there is if you end up seeing any kind of world crisis that causes the yen to rise, that could be an issue for exporting companies in Japan, because obviously the more expensive things are, in yen terms, the more difficult it’ll be for them, but basically I think things are good. Of course, if China decides to do something stupid, like with military stuff, that could be bad for Japan, but that’s always the case with global stocks.

Angela: Alright, Clint, I imagine you shined up your crystal ball. What do you see ahead in 2022?

Clint: For 2022, I think it’s more like an eight ball. You’ve just got to ask it a question and shake it, I guess. Actually, probably the most interesting thing I read this morning was from one of the investment banks. I can’t remember which one. It was basically they were justifying the levels that we’re trading at in the stock market, because everything’s expensive, so it’s that there is no alternative mindset.

Interest rates are still, on the long end, are still low by historical standards. You still can’t get anything for your cash savings, so is the stock market the only place to be? I step back and take a look at the big picture.

I think there is one overlooked macro opportunity that’s out there, and that’s with the commodities space. Commodities have, for a number of years now, underperformed what equities are doing, but that underperformance is creating some relative value, and it’s pushing that to an interesting level here.

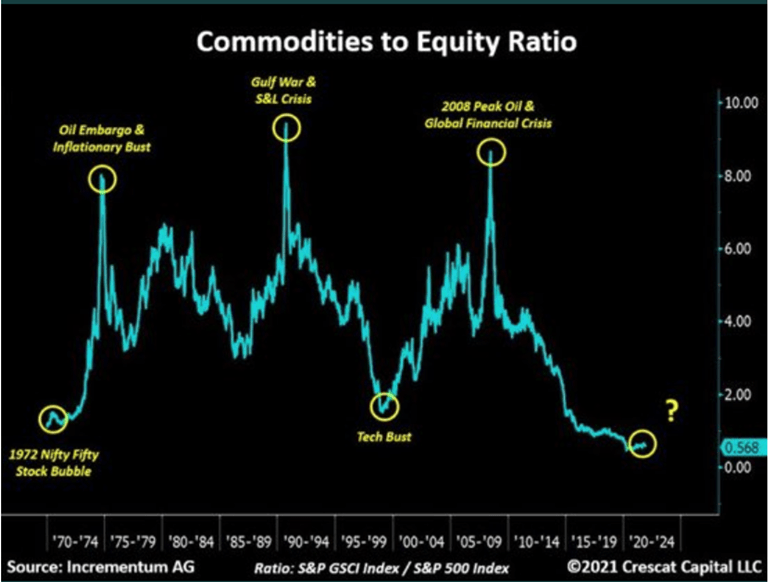

I’ve got a chart I want to show, and I want to highlight a couple key levels on here:

What this is, this is the commodities, physical commodities-to-equity ratio. This is just how commodities are performing relative to stocks. This goes all the way back to the 1970s. When the line’s rising, that means commodities are doing better. When it’s falling, that means the stock market is doing better. There’s a couple things I want to highlight on here.

First, this ratio, because of commodities underperforming, this ratio’s been pushed down to the lowest levels we’ve seen in over 50 years now, but what’s interesting is, when we’ve gotten down to these absolute low levels, this has come at other key turning points, bubbles bursting, in the stock market. You had, back in the early 1970s, the Nifty Fifty stock market bubble. That’s highlighted and circled on the left.

More recently, we had the dot-com, the original tech bust, back in 1999 and 2000. This ratio’s been pushed down to levels that we’ve last seen during those time frames. At the same time, we’re talking about how expensive stocks are here.

The other thing I find interesting with where we are is that, for a few decades now, commodities, as a group, have been moving in these 12-year cycles, a 12-year uptrend followed by a 12-year downtrend. Well, the last downtrend started with the financial crisis back in 2008, so since 2008, we’ve seen a sustained downtrend here in commodity prices. That 12-year timeframe would put us in 2020, which is, it looks like, where we bottomed at. Commodities had a good year last year but, based on this, they could just be getting started.

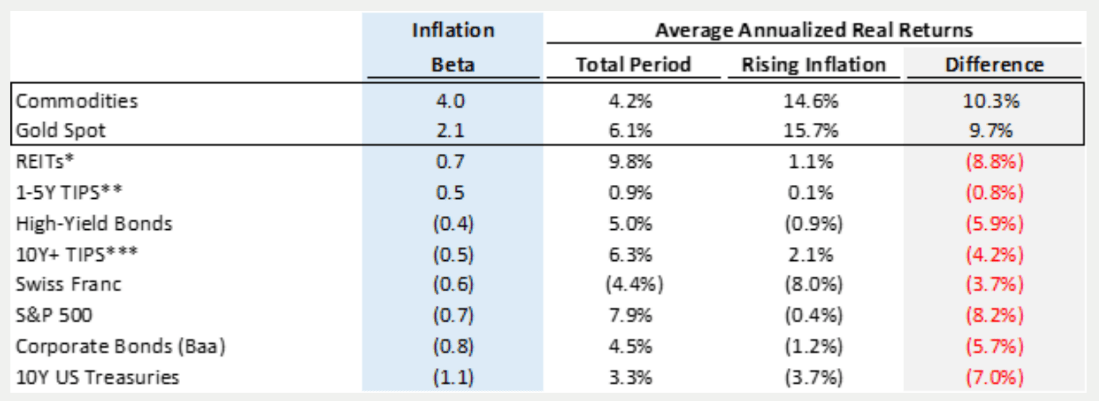

Now, the one other thing to consider with commodities right here is the uncertainty around the inflation outlook. Ted mentioned the uncertainties around knowing which way this is going to go, especially with COVID still ongoing, the supply chain issues that are still ongoing, so one thing to think about there is having a hedge, and commodities have been a good way to hedge against that inflation risk. Here’s a table, this comes from Verdad Advisers:

This shows different asset classes, what their inflation beta is. This is ranked by inflation beta, so just how sensitive these are to when you’re seeing periods of inflation. In the top two spots here are commodities, and then, specifically, pulled out of there is gold, as well.

You can look across the table here. I mean, historically, I believe this table’s from, this data is from 1970 through 2020, but across all periods, averaging life returns for commodities is 4.2%, but when you get into a rising inflation environment, it jumps up to 14.6%. You can look down the table. You can see, in especially certain asset classes, especially in fixed incomes start to struggle with this, but the key point here is that commodities, and certainly around inflation, is a good inflation hedge.

There’s a couple ways to play this. Look, this is a great time of year, you’re starting off the year, to just go through, look at your portfolio, decide how you want to re-weight, rebalance things, and if you have underweight or no exposure to commodities, this is a great time to think about adding some exposure here.

One way you can do that is with an ETF. The ticker is GSG. It is an ETF that is linked to the S&P GSCI commodity index. Now, I’m highlighting this one because it’s a broad-based index. It includes things like energy, agricultural products, base metals, precious metals, and so on. The one thing I’ll highlight with that ETF, though, is that about 57% of its exposure is to the energy sector, so especially with oil, you’re getting a lot of energy sector exposure there.

If you wanted to be more specific, more targeted, if you want to look at things like base metals stemming from industrial demand, you can look at ticker DBB for that. You can look at gold, if you want to be more specific, precious metals and gold exposure, looking at PHYS there. There’s a lot of different ways with ETFs that you can play commodities, and commodities, whether it’s these valuation levels, relative to how they’ve traded compared to stocks or the outlook for inflation, a lot of reasons to consider these right here.

Angela: There you have it, folks, some great ideas to get you started in 2022, some things to look for, maybe some warnings in there. Thank you, gentlemen, for your insights. Thank you, everyone, for watching. We’ll see you next week.

Good investing,

Angela Jirau

Publisher, The Bauman Letter