Germany’s Wehrmacht invaded Poland on September 1, 1939.

Western Europe’s response was swift and decisive.

No sanctions. Just declarations of war.

Now imagine Europe depended on Germany for grain. Without those imports, European populations would suffer, especially with winter approaching.

Would World War II have come as quickly as it did? Probably not.

In reality, Germany was already isolated. After 1933, the Nazis moved to make the country self-reliant. Everything went to Hitler’s war machine. Germany didn’t depend on Europe for anything in 1939, and vice versa.

From its spurious historical rationale to its bloodiness, Vladimir Putin’s invasion of Ukraine is a carbon copy of Hitler’s invasion of Poland (with one exception: Putin’s blitzkrieg appears to be failing in the face of fanatical Ukrainian resistance).

And yet, Russian commodities still flow westward.

Although Western sanctions have ratcheted up faster than I expected, there are still big carve-outs for Russian energy exports.

Trading With the Enemy

Between World Wars I and II, exports were about 6% to 14% of global gross domestic product (GDP).

Today, global trade is double that.

In geopolitics, that changes everything.

As the U.S. learned in 2020, depending on foreign countries — for things like Chinese masks — is a great deal, until it isn’t. The Chinese learned the same lesson when the Trump administration slapped sanctions on its flagship microchip company, Huawei.

Personal protective equipment and chips are critical commodities. But if a country puts its mind to it, it can make its own.

Not so when it comes to fossil fuels and minerals. You either have them or you don’t.

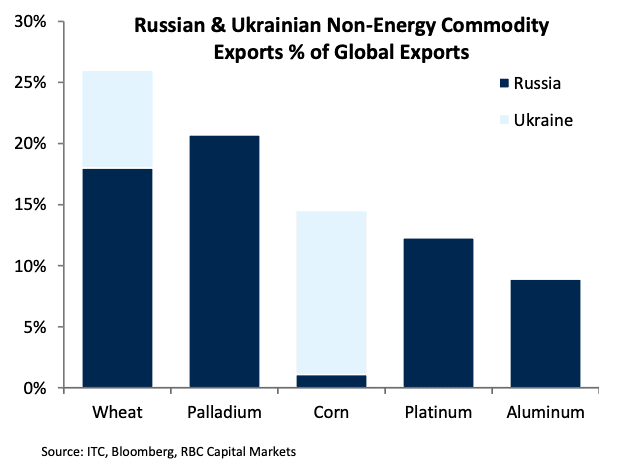

As Clint Lee and I explained in yesterday’s Your Money Matters, Russia and Ukraine are major exporters of some of the world’s most important commodities:

(Click here to view larger image.)

That’s why Europe and the U.S. were so reluctant to slap significant sanctions on Russia.

Comprehensive bans on Russian exports would have severe implications for the global economy. Sanction the Russian elite, sure, but keep buying all that Russian “stuff” on which we depend.

After a weekend of images of Ukrainian housewives and grandmothers bravely brandishing assault rifles and Molotov cocktails against the Russians, however, the West has decided to go all-in on sanctions.

What could this mean for you?

3 Key Fallouts

There are three key implications of ejecting Russia from the global economy.

1: Stagflation and Policy Paralysis

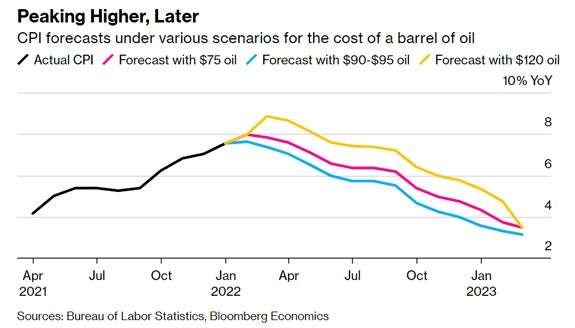

The war is a massive negative supply shock to the global economy. It will reduce growth and increase inflation — stagflation.

Commodity prices — especially energy — will skyrocket.

It’s already happening. Oil is trading at over $100 a barrel. European natural gas futures have risen from an average of about €75 ($83) per megawatt-hour last year to between €115 ($128) and €140 ($156).

That means inflation will peak higher and later than previous forecasts:

(Click here to view larger image.)

The same dynamics are at work in agricultural and mineral commodity markets. The Food and Agriculture Organization Food Price Index is at its highest level since 2010. Aluminum futures have reached $3,500 a ton, their highest price ever.

The result will be a sharp slowdown in the global and U.S. economies, with rising inflation and slowing growth.

But there’s nothing central banks or national governments can do about it.

Raising interest rates in the face of supply shock won’t stop inflation. It’ll just push the economy further into recession.

Pumping out money to compensate for trade disruptions will reinforce inflation, without supporting economic growth.

2: A $300 Billion Hole in Global Liquidity

The press talks about Russia’s foreign exchange reserves and how they could insulate the economy from Western sanctions.

There’s just one problem: About half of those reserves are held in foreign banks. And now they are trapped there.

As a commodity exporter, Russia accumulated a surplus of dollars. Russian banks, including the central bank, lent them out in the eurodollar market.

Now that Russian banks are cut off from the SWIFT payment system, those dollars are inaccessible.

The problem is that Russia used them to make payments for imports, currency swaps or other transactions with counterparties. Since the Russians can’t access those dollars, those counterparties are stuck with billions in unpaid bills. So now they have a liquidity crisis of their own.

On top of that, Switzerland has frozen Russian assets. The Norwegian sovereign wealth fund, the world’s largest, is liquidating all of its Russian holdings, probably at a steep loss.

All of this adds up to a massive withdrawal of liquidity from the global market. That lost purchasing power could put downward pressure on stocks and bonds all around the world.

It gets worse. As we saw with the collapse of Lehman Brothers in 2008 — not to mention the 1998 Russian bond default that crashed Long-Term Capital Management — a “liquidity event” like this could expose a hedge fund or a bank trading desk to insolvency. That could ripple through the financial system.

3: Emerging Market Crisis

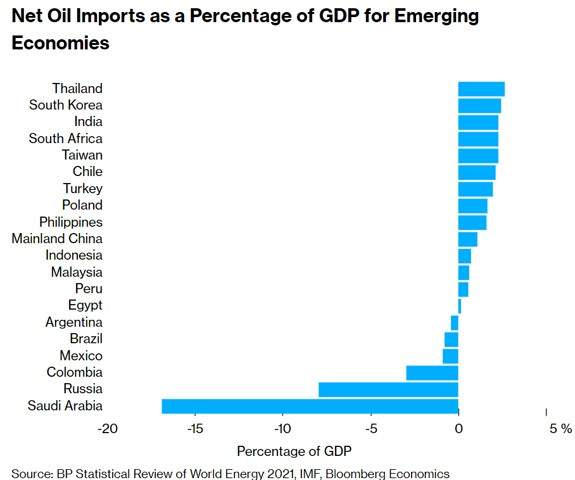

I just returned from South Africa, where a liter of petrol is about to cost more than ever before.

The same scenario is playing out across the entire developing world. Countries with large net oil imports as a percentage of GDP are going to see massive price pressures. Those will undercut the liquidity and balance sheets of everyone from national governments to individual households:

(Click here to view larger image.)

If the Ukraine crisis carries on for an extended period, we could very well see a financial crisis in emerging markets. That could lead to debt defaults, further eroding global liquidity.

Opportunities

Of course, it’s not all bad news.

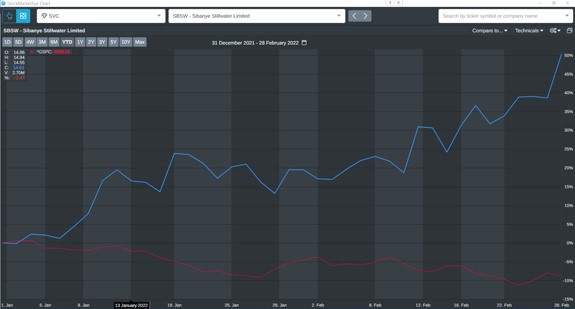

Shares of South African metals producers — the main alternative to Russian supplies of palladium and platinum — have spiked along with the futures prices of their products.

(Click here to view larger image.)

There will be many other opportunities like these, and I’ll be looking out for them.

But that’s cold comfort. Things are going to get worse before they get better.

At a time like this, it’s important to remember something I’ve always stressed at The Bauman Letter.

Some people are going to encourage you to look to politicians … either to solve this crisis or to blame for it.

But no matter what they tell you, this crisis isn’t something those in office today caused or can solve.

It’s entirely up to you to defend yourself against the onslaught coming from the global economy … the same way brave Ukrainians are defending themselves against the predatory Russian hordes.

Kind regards,

Ted Bauman

Editor, The Bauman Letter

{kind=link}

{kind=link}

{kind=link}

{kind=link}