Earnings season is almost done.

With 87% of the companies reporting for the fourth quarter of 2019, it looks like earnings grew 0.9% last year.

But more important than what earnings were is the question of what earnings will be.

Companies often provide earnings guidance when they report. This makes earnings estimates more accurate after earnings season.

Knowing what earnings should be helps us estimate what the stock market should do in 2020.

Here, the news is grim.

Earnings Are 1 of 3 Important Factors

In the long run, there are only three sources of stock market returns. And for the next few years, all three point to small returns.

Dividends are one driver of returns.

Before 1929, dividends were the most important source. Investors bought stocks for dividends. That changed when companies canceled dividends during the Great Depression.

After that, investors looked beyond dividends. They realized earnings growth delivers returns. If the earnings of a company double, the stock should be worth twice as much.

After World War II, earnings grew quickly as American companies rebuilt the global economy. As earnings climbed, so did stock prices.

Stocks also benefited from a higher price-to-earnings (P/E) ratio after World War II. That’s the third factor affecting returns.

The Price of a Dollar of Earnings

The P/E ratio tells us what investors are willing to pay for a dollar of earnings. To find the ratio, divide the stock price by the earnings per share.

If a stock price is $10 (the P in the P/E) and earnings (the E) are $1, the P/E ratio is 10.

If the stock price is $20 when earnings are $1, the P/E ratio is 20, and investors are willing to pay twice as much per dollar of earnings.

The P/E ratio was about 12 in 1945.

It climbed to more than 44 as the bull market ended in early 2000.

That means investors were willing to pay 266% more for a dollar of earnings in 2000 than they paid in 1945.

Earnings were higher in 2000, and investors paid more for each dollar of earnings. That’s why investors were irrationally exuberant at the beginning of the 21st century.

Looking ahead, there’s little cause for exuberance.

3 Factors, All Bad

Looking at a shorter time frame, we can see exactly how important the P/E ratio is.

In 2019, the S&P 500 Index gained 31.5%. Earnings increased 0.9%, and dividends added 2.2% to returns. The rest of the returns are due to an increase in the P/E ratio.

For the next year, analysts optimistically expect earnings gains of about 7%. That’s before accounting for the coronavirus or an economic slowdown. Growth of 7% looks optimistic now.

Dividends can add 1.7% to gains. Assuming earnings hit estimates, the S&P 500 could gain 8.7% if the P/E ratio stays the same.

Whether this year is better than average depends on the P/E ratio. Here, the news is bad.

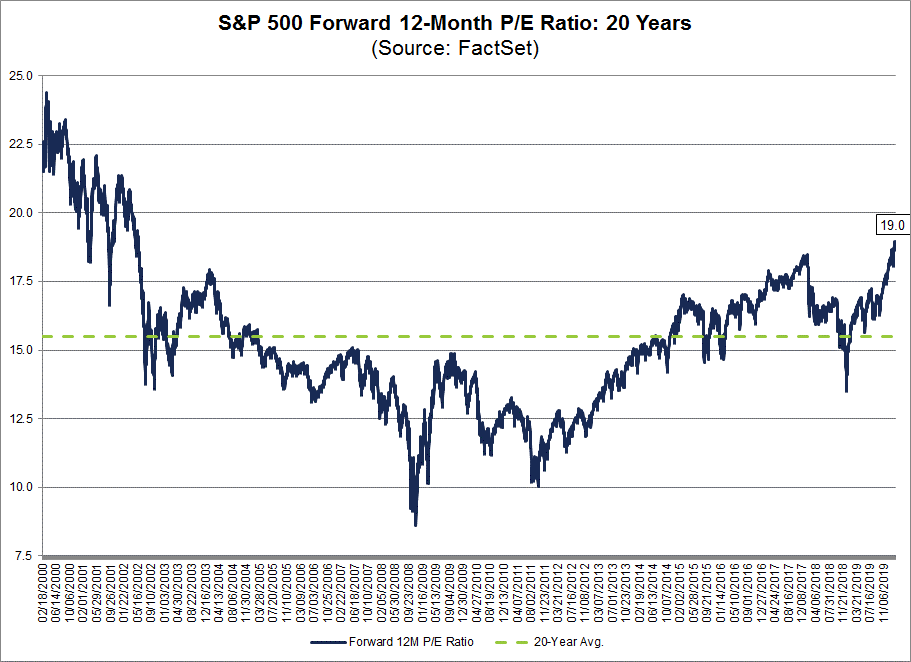

The P/E ratio, based on expected earnings, is now at 19. That’s the highest it’s been since 2002, when stocks were bottoming after the internet crash.

(Source: FactSet)

This indicates the P/E ratio is unlikely to go up. That means stocks should go down.

Now Is the Time to Be Cautious

Over the past 20 years, the average P/E ratio was 15.5, more than 18% below the current ratio.

From its current level, the P/E ratio is likely to hurt returns. We’re unlikely to end the year with the P/E ratio at a record high. Any decline in the ratio results in lower returns.

Don’t forget that earnings estimates are optimistic. Any shortfall in earnings growth also lowers returns.

It’s possible that none of this matters. Stocks could move up if investors ignore earnings and the news.

But that’s unlikely. Now is the time to be cautious.

Regards,

Editor, Peak Velocity Trader