The Federal Reserve met this week. As you may know, Fed officials hold a two-day meeting every six weeks.

While that makes interest rates a trending topic on X (formerly Twitter), economists and analysts look beyond those headlines. They know that interest rate policy might be the Fed’s least effective tool against inflation.

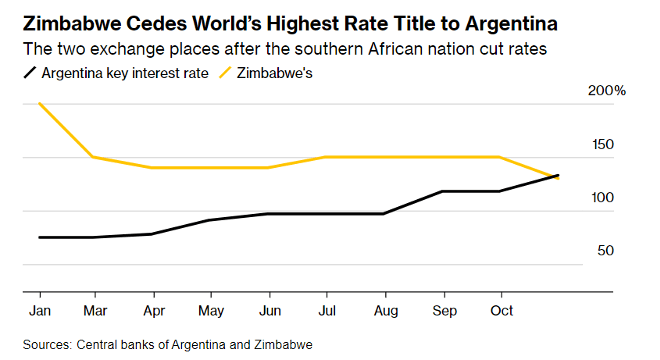

And we have proof of that all around the world. For example, Argentina and Zimbabwe would be in great shape if high rates actually killed inflation.

Last month, Argentina raised rates to 133%. Central bankers hope that’s enough to curb inflation of 138%. That hike pushed Argentina ahead of Zimbabwe in the contest for the highest rate in the world.

Interest rates in Zimbabwe are 130%, but that might not be enough to lower the country’s inflation from 176%.

(From: Bloomberg.)

So if interest rates aren’t the big story on Fed days, then what is? It’s actually the Fed Chairman’s press conference…

Confidence in the Fed: A Tool Against Inflation

Press conferences are relatively new. The first conference was held by former Chair Ben Bernanke in April 2011. Bernanke delivered quarterly updates on the Fed’s economic projections. Jerome Powell began holding conferences after every meeting in January 2019.

Bernanke started the conferences to solve a problem. He worried that markets weren’t giving the Fed credit for solving problems.

The Fed contributed to the recovery in 2009 by taking unprecedented steps to increase the money supply. A plethora of new programs were introduced. Confusion reigned during the crisis and for months into the recovery.

Bernanke’s press conferences changed that by boosting confidence in the Fed. We have research supporting the fact that confidence in the Fed is an important inflation fighting tool.

Nobel Prize-winning economist Milton Friedman believed that the Fed made the Great Depression great. He blamed unpredictable policymaking for the mayhem.

You see, businesses and consumers couldn’t plan in that environment. And that led to widespread unemployment and a decade of economic stagnation.

Moreover, Friedman argued that predictable monetary policy would fuel economic growth. It would slow inflation. But getting there required clear communications from the Fed.

Bernanke knew all this. He was a leading scholar of the Great Depression. In that sense, he was uniquely qualified to be Fed chair during the 2008 crisis. His research drove his decision to offer insights into Fed decisions.

The market loves Bernanke’s invention. So Powell and future Fed chairs are stuck with press conferences. Because if conferences stopped, traders would wonder what the Fed is hiding. That would push rates up, and stocks would fall.

Trust in the central bank is also critical to low inflation. Lack of trust fuels triple-digit inflation in Zimbabwe and Argentina. Both governments follow erratic economic policies as presidents lean on central bankers. Long-term planning is impossible in those countries, and this creates high inflation.

It’s unlikely the U.S. will end up like Argentina. But the Fed may lose some credibility if the public believes politicians influence the Fed.

That’s the problem Powell faces over the next year. We might see rate cuts in 2024. Traders might see aggressive cutting as helping President Biden’s electoral prospects. That will hurt the Fed. Market rates will rise if that happens. And stocks will fall.

That means the Fed’s on a tightrope, and those press conferences will determine how investors react.

Regards,

Michael Carr

Editor, Precision Profits