The Blue-Chip Kiss Of Death

Great Ones, I’d like to say that I’m surprised that Netflix (Nasdaq: NFLX) tanked today. I’d like to…

But after waking up to two-and-a-half inches of snow — in Kentucky — with forecasts for 67 degrees in the afternoon … well, I’m all out of surprise for the day.

In fact, I had pretty strong suspicions that Netflix would tank after earnings. The pandemic subscriber hype was just too much for the OG streamer to bear. Before we get to subscriber numbers, however, let’s look at the money.

Netflix blew out earnings expectations, banking a profit of $3.75 per share on revenue that jumped 24% to $7.16 billion. Both figures were well ahead of Wall Street’s targets. All in all, the company turned in a rather impressive quarter — fundamentally speaking, that is.

But, as anyone who invests in or follows Netflix knows, it’s almost never about earnings or revenue.

It’s all about subscriber growth. On that front, Netflix came up considerably short … like 2 million subscribers short. The company said it added about 4 million subscribers on the quarter, versus prior guidance for 6 million new subs.

The kicker? Netflix said it only expects about 1 million new subs in the current quarter. The company blamed the miss and low expectations on — shakes Magic 8-Ball — COVID-19.

“We believe paid membership growth slowed due to the big COVID-19 pull forward in 2020 and a lighter content slate in the first half of this year, due to COVID-19 production delays,” Netflix said.

C’mon, you know you saw that coming! Netflix said it expects subscriber growth to reaccelerate in the second half of 2021 … but I’m not so sure that will happen.

Netflix isn’t the only streamer in the pond anymore. In fact, the market is saturated. The technology barrier to entry that once protected Netflix is gone. Now, every media company with a smidge of content — and every tech company with enough money to buy content — has its own streaming service.

And the biggest threats are just now ramping up: With its combined unholy trinity of Disney+, Hulu and ESPN+, Walt Disney (NYSE: DIS) already usurped Netflix’s crown as the biggest combined streaming company.

AT&T (NYSE: T) is a serious up-and-coming threat with HBO Max — if only AT&T would stop tripping over its own shoelaces. And Amazon Prime TV (Nasdaq: AMZN) — which doesn’t even seem like it’s trying to compete while it rides Prime shipping subscribers.

And then there’s the growing multitude of free services from Roku (Nasdaq: ROKU), Peacock (Nasdaq: CMCSA), Crackle, Sling TV, Pluto TV, TubiTV and Plex … just to name a few.

If Netflix thinks things will just go back to normal in the second half of 2021, it’s in for a rude awakening. Consumers’ media budgets are already stretched thin. Choices will be made, and Netflix won’t be at the top of everyone’s “keep” list.

I think NFLX investors have to realize that the days of excessive growth are over. Netflix now must fight tooth-and-nail just to maintain its position. Don’t get me wrong: Netflix isn’t going anywhere. It’s a solid company with an impressive business model. However, the bloom has come off the “growth” lily, so to speak.

Netflix is no longer a high-growth tech stock. It’s now a blue-chip company. And that will change how investors all across Wall Street approach the stock.

The bottom line: NFLX investors should get used to a bit of volatility as Wall Street adjusts to this new Netflix normal.

Editor’s Note: It’s Not Impossible, It’s Imperium!

According to experts, “Imperium” is set to go from virtually unknown to having 2 BILLION users in the next four years. And it’s about to spark the biggest investment mega trend in history … with one small Silicon Valley company at the center of it all.

Watch this video now to discover details of the No. 1 Imperium investment for 2021!

Good: Losing A Two-Horse Race?

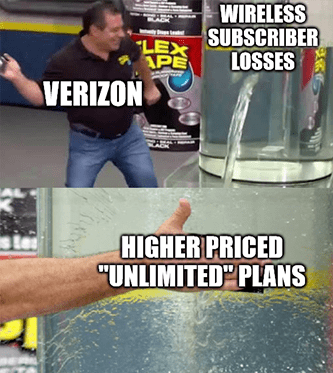

With AT&T fumbling toward ecstasy with HBO Max, the pure-play wireless market has essentially become a two-horse race between Verizon Communications (NYSE: VZ) and T-Mobile (Nasdaq: TMUS).

Judging by Verizon’s first-quarter earnings report, that race isn’t going too well. On the surface, nothing appears wrong. Verizon’s earnings and revenue both rose year over year to beat Wall Street’s expectations.

As with Netflix, however, subscriber numbers were abysmal.

Verizon said it lost 326,000 wireless retail postpaid customers on the quarter. Admittedly, it was an improvement over the 525,000 it lost in the same quarter last year … but still, losing subscribers during a pandemic lockdown is not a good look for the self-proclaimed best wireless network in the country.

Now, you might be thinking: “How did Verizon boost earnings and revenue while losing customers?” The answer is higher-priced unlimited wireless plans and premium wireless plans. Verizon is no fool — it partnered with Disney to give Hulu, Disney+ and ESPN+ free to premium subs. It also has deals for Apple Music and Discovery+.

One could argue that Verizon has growth potential with Fios Internet. But the churn rate between Fios TV and Fios Internet is nearly identical, with internet gains making up for TV losses. It’s essentially a wash.

That said, Verizon still has the perception as the best and most reliable wireless provider in the U.S. If customers are willing to pay more for this premium perception, Verizon still has plenty of chances for bottom-line growth.

Better: Go Ahead, Bite The Big Apple

Don’t mind the maggots. Uh-huh! (Shooby.)

Whatever you got up to throughout these many locked-down months … I guarantee it was more productive than Apple’s (Nasdaq: AAPL) ideas team. Apple kicked off its first product showcase of the year with its typical modus operandi … i.e., more of the same ol’ stuff.

The new iMac now comes in colors — she’s like a rainbow — which I presume is earth-shattering for some. Something other than silver and white?! By gosh, I think we’ve reached … the 90s!

Besides Apple rehashing old tech with new looks … wait, no, that’s all there really was. Want a new iPad? Apple’s fresh iPad Pros have 5G now, which is great for all you iPad streamers out there — no more buffering on my 4K high definition cooking videos, heck yeah! You can actually see the grains of salt!

And I guess we should talk about Apple’s AirTags — little round doo-hickeys that you can stick on stuff and then track using an iPhone’s “Find my $#!* for me” function. Apple must’ve scrounged around the spy gear table at a Scholastic book fair for new product ideas…

Apple thinks you could put an AirTag on your keys and, lookee there, you can find your keys like super easily! But sike, I’m putting that sucker on my cats to figure out where they run off to at 4 a.m. Just wait until someone stitches an AirTag into their teen’s sweater for some helicopter parenting. “Uh-huh, sure you were at Emily’s; the Tag proves that was a lie.”

Apple says the fob-finding feature is fully “privacy-sensitive,” and I think if any other company tried to pitch you tracking devices, the security uproar would be immense.

But with Apple, you can make a living off of “more of the same” … even if it’s tech that’s been around for decades now. AAPL investors weren’t quite thrilled with what the company hatched up anyway, and the stock ended the day relatively unchanged.

Best: Paging Dr. Robotnik

I told you Intuitive Surgical’s (Nasdaq: ISRG) report would be anything but a sleeper hit this week! Intuitive is one of those companies that I like more and more as time goes on.

The fact that it helps make surgeries safer and less invasive is just icing on the robotic cake.

Word of mouth is everything in the medical tech industry, and Intuitive is bubbling with built-up buzz over its robot-assisted surgery tech.

Understandably, the pandemic’s early stages had Intuitive’s main clinic-based clientele rather preoccupied. The bright side is that it makes Intuitive’s year-over-year comparisons tremendous.

Per-share earnings hit $3.52, and revenue reached $1.29 billion. Both figures beat analysts’ estimates — $2.64 per share on $1.11 billion in revenue — and blew last year’s earnings out of the water. The company shipped 26% more units this quarter compared to the same time in 2020.

But shipping the robotic machines out is just the start of the revenue train — system service revenue is also a growing part of Intuitive’s biz. That’s how they get ya hooked. Notably tight-lipped CEO Gary Guthart was over the moon about the news: “Our performance reflects customers choosing Intuitive as COVID eases.”

So that’s a “yes” to what we posited earlier about hospitals buying/upgraded their equipment, and the (relatively) waning pandemic should only ramp up medical spending for things like robosurgeons. And on that note … it’s time for a fresh Poll of the Week!

That’s right: We’re sticking with our intuition and surgical robot wunderkinder. Erm, I mean, talking about medical robots … and medical robot accessories. Intuitive Surgical is the top dawg in the assisted surgery space, but it’s far from the only name in the game now.

But what about you? Have you ever invested in Intuitive Surgical or rivals like Stryker? That’s to say, have you ever invested in medical robots?

Click below and chime in:

Answering polls not your thing? I’ll let it slide … this time around.

But do let me know: Would you (or have you) ever gone under the roboknife? Drop me a line with your thoughts on robosurgery, Apple’s aggressively average announcements and Netflix’s collapsing world. Who knows? You might just see your email here in tomorrow’s edition of Reader Feedback!

GreatStuffToday@BanyanHill.com is the virtual water cooler around which we’ll gather tomorrow.

And for all those numerous readers writing in saying “Add me!” or “Sign me up!” … first off, how’d you receive this? Second, all you have to do to sign up for Great Stuff is click here!

Once again: Just click here if you want to sign up for Great Stuff!

Finally, remember what Mr. Great Stuff always says: Like Stuff? Share Stuff! So be sure to share ‘Stuff with everyone right down your email list. Send it all!

And don’t forget! If you want to be in this week’s edition of Reader Feedback, drop us a line at GreatStuffToday@BanyanHill.com! But, if that’s still too many virtual hoops to jump through, why not follow along on social media? We’re on Facebook, Instagram and Twitter.

Until next time, stay Great!

Joseph Hargett

Editor, Great Stuff