One viewer’s question sends me down the rabbit hole, questioning whether the old saying that “cash is king” still rings true.

Obviously, it is, but what kind of cash?

I go into detail, covering everything from gold and TIPS to buffer exchange-traded funds.

Transcript

Hello everyone. It’s Ted Bauman here, editor of Big Picture, Big Profits, and of The Bauman Letter. Before I start, I’m wearing this T-shirt today kind of as an ironic dig on myself. Congratulations to the Bangladesh cricket team, which just won their first away series in South Africa, by beating my team, the Proteas, two nill in a one-day international series. So congratulations to you, Bangladeshi Tigers. The guys who run the little shop down the road for me, who are all from Bangladesh are going to be ribbing me about that all week. Today, I want to talk about something that one of you raised in the last video that I put out. Comes from Grand Lux Auto, and he says:

Well, before I get to that, just remember that one of the things you can do is to consider subscribing to The Bauman Letter by clicking on that little eye up above my left-hand shoulder on the left-hand side of the screen. And we do have some strategies for a recession. And that’s one of the things that we do. We’re not just about investing in stocks on the way up. We’re also about looking for strategies to the way down. So if there’s something that interests you, click on that link, which will still be there and also in the description below, after you’ve heard what I’ve had to say, you can click on it then too.

So, what are your options, Grand Lux Auto, any relationship to Lux Supreme from The Cramps? Maybe? No. Anyway, first thing you’re going to do, potentially, is go to cash… Now why do you want to go to cash? Well, obviously one of the reasons to go to cash is to get away from assets that could potentially lose value like stocks in a crash, but that’s not the only reason. Because even if stocks do fall in a crash, you shouldn’t sell them.

People often do that in a panic when the market collapses, out of emotion, because there’s no logic behind selling in a crash. All crashes eventually recover. So, let’s look at evidence for that:

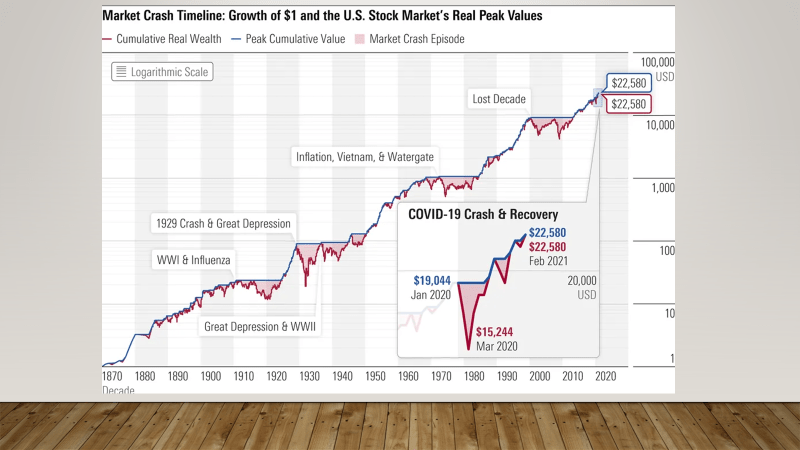

Here’s a chart that shows periods in the stock market when we have seen very significant drawbacks. And you can see them going back right to World War I. All periods in the stock market involve pullbacks. It’s pretty rare that you see uninterrupted growth in the stock market without a pullback. We saw big pullbacks during the period, well during World War I, during the Great Depression, we saw it again during the 1970s with Watergate inflation, and then we saw it, interestingly enough, what they’ve called the lost decade on this chart. And that’s basically between the dot-com crash and the crash of 2008, the subprime crisis. And what’s interesting is that stocks only really regained their highest level, the level that they had reached at the beginning of the ‘90s, really only just after the 2009 subprime crisis.

And what’s interesting is if you look at the line there, what do you see? You see that the line after that has very few pullbacks up until the very last moment, which is pulled out as the COVID crash. The only other time we’ve seen something like that was in the early 1950s, just before the Great Depression, and then just before the big pullback in the dot com bust. So there’s something to be said for these periods of uninterrupted stock market growth. They tend to be followed by periods of stagnation. Now that gives you the evidence that proves that doing something is better than doing nothing. So I’ve said that cash is one of your best options. Why is that?

Well, as I said, the reason for going to cash is not just to be out of stocks. You don’t want to be a 100% out of stocks, but you want to have enough cash to be able to buy stocks when they are at their lowest point.

In other words, when they’re blood in the streets, that’s when you buy. So one of the key things about going to cash is not just about avoiding holding equities that may fall, but having dry powder to buy stocks when they’re at their bottom. Remember if you had bought stocks at the market bottom after the COVID 19 crash in early 2020, and held them until the market peaked in 2021, you would’ve made an enormous windfall of over 100%. Of course, that depends on calling the bottom and calling the top. Again, it’s very hard to do. But without cash at the bottom, you wouldn’t have known what to do. Now, one of the problems with something like the COVID crisis is that that was completely out of the blue, unpredictable. It was not related to economic or financial conditions. And therefore it’s a genuine black swan event. A black swan event being basically an event that nobody can predict, that is not foreseeable.

Right now, I do think that we see lots of reasons why we could potentially see a big pullback in the stock market. I’m not going to predict one. I’m not calling for one. What I am saying is that the conditions are in place for such a pullback to happen. And when that’s the case, all it takes is a small piece of tinder to light that on fire. Now, what are those factors? Well, one is that for nearly 15 years, the federal reserve has suppressed price discovery, both in stocks and bonds, basically by intervening in the bond market, suppressing yields, which forces everybody out the risk curve and into lower quality assets. Which means that a lot of those assets are still overvalued and therefore ripe for pullbacks. We’ve got historically excessive inflation. We’ve got a fed that’s committed to raising interest rates, and we’ve got a war in Europe and a massive spike in commodity prices.

Probably most concerning was we’re starting to see a pullback in the 40-year bull market in U.S. Treasurys, widening yields. And we’re also seeing widening yields between corporate debt and Treasurys. That’s putting stress on the financial system, especially highly indebted companies. Now, with all of that together, the idea is not just to go to cash now willy nilly by selling everything, but by selling enough equities now that you can feel comfortable riding out a downturn or a pullback with those equities, knowing that they’re eventually going to bounce back. Because they did in every time period that I showed you in that chart, but more importantly, so that you would have cash at the time when you want to buy stocks when you feel like they’ve bottomed, you want to be opportunistic. Now, the next thing of course is gold.

Now gold is clearly an asset that is known to be a safe haven in times of crisis. In fact, we’ve seen gold outpace the market this year for understandable reasons. But gold is second place to cash in my book because gold takes time to convert back into cash in order to be able to apply that into stocks. Now, I would say that if you want to liquidate part of your stock portfolio in order to be able to have dry powder, about half of what you sell now in anticipation of a pullback, keep in cash. The other half you can keep in gold so that you could at least buy something now, or when the market pulls back, you’ve got the cash. Then you can convert more gold if you needed to do so in order to take advantage of low prices in stock. Now, one of the other things about gold in a crash is that, paradoxically, it tends to fall in the beginning of a crash.

Not because people don’t want it, but because a lot of people are liquidating gold holdings to raise cash. So one of the things to remember about gold is that when the market pulls back suddenly, you want to wait a couple of days, sometimes as long as a week or even a fortnight for gold prices to bounce back after that initial bout of selling as big institutional investors sell gold to raise cash. Now, the third potential opportunity is something called TIPS.

TIPS basically means inflation-protected Treasurys. And what they are essentially are Treasury bonds that have some unique features. Unlike normal Treasury bonds, which have a fixed value and a fixed coupon, TIPS essentially have an inflation protected setup. And this is how that works. When you buy a TIPS bond, you buy it at a face value.

Let’s say you buy a thousand dollars face value TIPS bond with a 3% coupon. 3% meaning that is the nominal yield, the yield that is committed to by the government. Now in the first year, you would receive semi-annual payments of $30, in two semi-annual payments like you always do with Treasurys. But let’s say that the consumer price inflation increases by 4%. In that case, the government will automatically increase the face value of the TIPS bond by $40 to compensate you for the 4% rise in inflation. So you bought a bond for a thousand dollars. It’s now worth $1,040. Now in year two, you still receive a 3% coupon interest payment, but this time it’s based on the new higher value of the TIPS, which is 1040. So instead of receiving an interest payment of $30, you receive $31.20, which is 0.03 times 1040.

Same thing happens when inflation goes down. Basically it’ll pull back the value of the TIPS in relation to the fall in inflation. And so you’d get a smaller coupon payment, same rate, but a smaller coupon payment based on the current value of the bond. The critical thing is with TIPS that the face value of the bond goes up to compensate you fully for consumer price inflation, and you get paid your full amount or your full coupon payment calculated as a percentage of that increased face value. Now, one of the things that’s nice about TIPS is that can help to compensate you for inflation. The only downside is that if you want to trade that bond for cash, because they do trade in the secondary market, you might sell it for a lot less than its actual current face value.

In other words, somebody might not be prepared to pay you what the government would pay you if you held it to maturity. That bond that’s worth maybe $1,040, because inflation is at 4%, somebody might only pay you $998 for it. And so you’d lose money. So one of the critical things about TIPS is you want to make sure that you hold them to maturity, or don’t sell them unless the market for TIPS is essentially getting weaker, which means that the demand for TIPS is falling. When you have inflation and rising interest rates, the demand for TIPS goes up, which means that their face value or their trading value in the secondary market, i.e. buying them from other investors as opposed to the government, tends to fall. So if you want to buy TIPS in order to protect yourself from a potential market crash, buy them directly for the government.

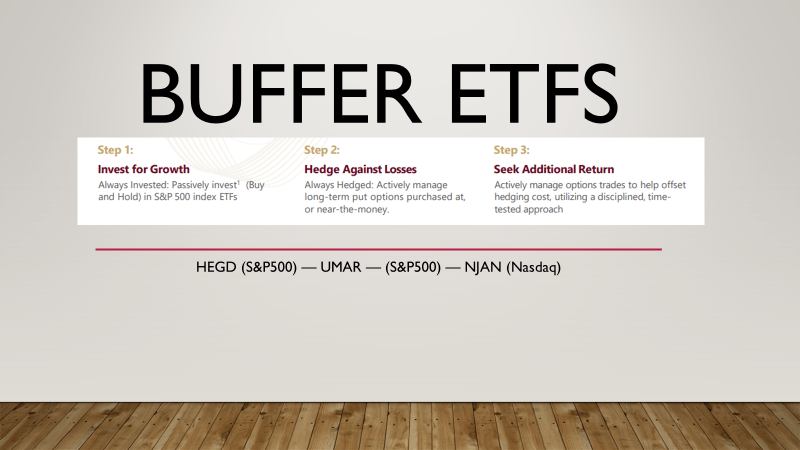

You just Google, “buy TIPS,” and it’ll take you to a government website where you can do that yourself. The other thing to remember about TIPS is that you are taxed on the increase in the value of the bond that the government gives you to compensate for inflation. So there is a slight negative correlation with inflation, thanks to the proportion of tax. But if you hold them in a retirement account, which is really the ideal scenario, you won’t get taxed. So that is a critical thing to remember, that you will pay tax on the increase in value of the TIPS bond as a result of the government basically just giving you extra value when inflation goes up. All right, what else have we got? Well, the next thing you can do, and it’s actually something that I find very interesting, they’re called buffer ETFs.

It’s something that I’ve recently discovered. Now, buffer ETFs are ETFs that are designed to track the performance of a particular index, like the S and P 500 or the NASDAQ. But they’re designed to trigger a downside protection once that index falls by a certain amount. You can get different ETFs basically with different downside protection. Some of it will kick in very quickly, let’s say after a 5% pullback in the market. Some of them will only kick in after a 15% pullback. Obviously the big difference there is that the ones that pull back sooner give you a lower return and a lower dividend payment than those that kick in with a steeper drop in the market. Now, one of the things about TIPS is that they are actively managed, which means that their expense ratio relative to other passive ETFs is a bit higher, because it means that there are managers who are doing this work on your behalf that are basically actively managing. But they’re not just buying the index fund, obviously. Because in order to be able to give you that downside protection, they have to do something else.

So for example, they buy long-term put options against the same index. They always buy them at or near the money, which means that they are not going to lose on the put options under normal expectations, but they will get paid enormously if the market does pull back. Now, that allows them to pay an additional return above and beyond the index, which is what helps to hedge your position. So buffer ETFs are essentially something that is actively managed, that in good times will track the index, but in bad times the put options kick in and they then basically protect you on the downside. Now here’s some examples on the bottom of this slide, HEGD is one. UAMR is another. Both of those are hedged against the S&P 500. And NJAN, that’s the Nasdaq, it’s hedged against the Nasdaq.

Now, one of the things that I haven’t mentioned, which some people often mention in these kind of environments, is something like foreign currencies or commodity ETFs, or consumer staples ETFs. Because those are all things that continue to do well, even if the economy pulls back. But remember, I’m not talking about the economy here, I’m talking about the stock market. The stock market can crash even if the economy is doing well. But what about if both crash together? What if we have a recession as a result of rising interest rates and higher commodity prices? Well, all things being equal, that would put downward pressure on commodity prices, which is why I’m not suggesting that you hold commodity ETFs as a hedge against a pullback. Because my opinion is that if we do see a pullback in the market from which we will recover eventually, remember nothing last forever, but if we do see a pullback in the market eventually, or the most likely scenario in current situation is that it’s going to be accompanied by a pullback in the economy, which means commodities will fall.

So under these specific situations, I wouldn’t go for commodity as a hedge. The same thing goes for currencies like the yen or this Swiss franc. Now they may recover quite nicely if we do in fact see a downturn in the economy. But right now, because the dollar tends to be such a strong currency and because it is de facto the cash reserve that most people take, the chances are under current circumstances that the dollar strength would negate any benefit you get from the rise in the yen and the Swiss franc. Now that’s not always the case, but particularly if there’s a recession, you might see people fleeing to the dollar because they want Treasurys and that would lead to both a decrease in Treasury yields and to a strengthening of the dollar, which would negate that.

In other words, the strength of the yen and the Swiss Franc. The last thing is sometimes people say buy consumer staples because if the economy does slow down, all your other stocks are going to go down because of a recession. But consumer staples should stay relatively, they should maintain their value and potentially even grow as investors shift from the stocks that are going down to staples, which should be going up. Now that’s a viable strategy. But if you really are expecting a recession, and particularly if prices are rising, if we have stagflation at the same time as a recession which is the scenario we could face, then people are going to cut back even on their staples purchases.

And that means that that effect might not be as strong, which is why I have not recommended them here today. So to recap, what I’m saying is that if we do have any kind of a major pullback in the market, and I’m not predicting when, I’m not saying it’s definitely going to happen. But if it does happen, then my four recommendations are (1) cash, (2) gold, (3) TIPS, inflation-protected Treasury bonds, and (4) buffer ETFs. Those are all options that you can pursue. Now, when it comes to gold, you don’t necessarily need to buy physical gold. You can buy ETFs like GLD or any other ETF that holds gold because it’s essentially based on the gold price. If you really want to own gold, by all means own gold. I do believe everybody should have about 5% of their portfolio in gold anyway. The other possibility, of course, is to buy gold miners. So that’s another option for you there.

Anyway, there’s four strategies and some sub-strategies that you could use if you think that there’s going to be a pullback later this year or next year, or anytime really. But remember, it’s impossible to predict. And anybody who says they can predict exactly when a pullback is happening, they’re just talking smoke. My personal belief is the only way you can prepare is to look to see what’s happening on the forest floor. Is there tinder building up? Is it getting dry? Are we likely to see fire conditions in the market?

I think we are seeing those right now, and it really wouldn’t take much. An escalation in the war in southeastern Europe, a real move that might suggest conflict between NATO and the Russians, that could do it. If we saw the beginnings of serious trouble in financial markets as a result of leveraged bets anywhere, on debt, anything, Russian bonds, who knows what it could be, those can cause kind of domino effects. All those kind of things can happen. And those are the kind of things that are unpredictable in terms of when they will exactly happen. But more than likely under certain conditions like the ones we are facing right now.

Anyway, that’s all for me this week. And I will talk to you again next week. Ted Bauman signing off.

Kind regards,

Ted Bauman

Editor, The Bauman Letter