Warren Buffett is the world’s greatest investor, but he rarely speaks about how he achieves his success. Students of Buffett often rely on cryptic messages in his annual reports for insight into his thinking. But Buffett values money above all else, and rather than listening to what he says, we should focus on what he does with his money.

Kraft Heinz’s recent bid for Unilever is an opportunity to see what Buffett looks at when valuing a company.

We know Buffett was involved in the deal, and we know he takes pride in never overpaying for a company. The proposed price of the deal was what Buffett seemed to believe the stock was worth. For each existing Unilever share, Kraft Heinz offered $30.23 in cash and 0.222 shares in a new holding group. The total value came to $50 a share, or about $86 billion in cash and shares worth another $57 billion.

This likely indicates that Buffett believes the current value of the company is $30.23, with additional upside represented by the shares in the new company.

Although he’s known as a value investor, there is no sign of traditional value in this bid. The proposed deal valued Unilever at more than 23 times next year’s expected earnings. Value investors tend to prefer low price-to-earnings (P/E) ratios, and a P/E ratio of 23 is well above average.

Other value metrics paint a similar picture. The deal’s price-to-sales ratio of 2.5 is 70% above the industry average and a 25% premium to Unilever’s long-term average. Valuation ratios using book value, cash flow, free cash flow and other financial statement ratios are all overvalued compared to the market average, industry average and historic comparisons for the company.

The first lesson from this proposal is that Buffett doesn’t use simple, widely followed ratios. Let’s turn to some less well-known valuation metrics…

It’s Not So Simple

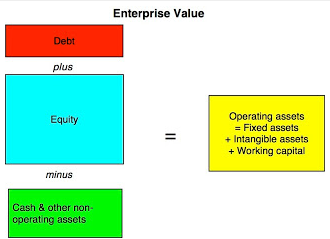

Enterprise value (EV) includes debt and measures the total cost of ownership for someone buying an entire company.

(Source: Musings on Markets)

Under the proposed deal, Unilever was valued at a premium to its industry using EV metrics, which indicates Buffett saw something about the company that isn’t measured by traditional valuation tools.

An analysis of Unilever’s performance over the past seven years shows Buffett also wasn’t buying growth. A span of seven years is used in this analysis because that was the time frame preferred by Ben Graham, a Columbia Business School professor who taught Buffett.

Unilever has reported average growth in sales of only about 4% over the past seven years, and revenue has been on a downward trend in recent years. Earnings per share and various measures of earnings from the income statement show average growth of only about 6%.

Financial statements can also be used to evaluate management. Return on equity (ROE) is one way to evaluate management’s effectiveness. A good management team should generate more profit for each dollar of the company’s equity. Unilever’s ROE of about 33% is more than twice the industry average. We now have our first clue of what Buffett might look at — a higher than average ROE.

Digging Deeper

Next, we need to consider what a dollar of equity costs. While management delivers higher than average ROE, it’s important to ensure the equity is obtained at a low cost. Otherwise, the company will not maintain profitability over the long run. In the case of Unilever, the cost of equity is about 8%. This is lower than average for multinational companies like Unilever.

The company is generating returns four times larger than the cost of equity, and the equity carries a lower- than-average cost. This indicates, in effect, that Unilever is a money printing press.

That’s what made Unilever attractive to Buffett. He likes to own money printing presses, and in the case of Unilever, this printing press could generate billions of dollars a year.

Cash flow from operations (CFO) has averaged about $7 billion a year. About a third of that amount is required for reinvestment in future operations. This would leave Buffett with an average of about $4.5 billion a year to allocate for other investments, and this could be what Buffett was trying to buy: a measure we could call the owner’s cash flow.

At $30.23 a share, Buffett offered 19 times the owner’s cash flow. This would have provided a cash yield of 5% on his investment, a nice return in the current environment. Buffett could then have increased that yield with some simple financial engineering and by issuing debt at near-zero rates in Unilever’s euro-denominated bonds.

Now we can create a checklist for how to think like Buffett:

- Look for higher-than-average ROE.

- Look for lower-than-average cost of capital.

- Look for companies with CFO at least 100% larger than average capital expenditures.

- Limit buys to companies offering a yield on owner’s cash flow that’s about twice as large as the yield on long-term Treasurys.

This isn’t as easy as looking for stocks with low P/E ratios, but Buffett obtains better-than-average returns. The extra work of digging deeper should be rewarded, as Buffett has proven for more than 50 years.

Regards,

Michael Carr, CMT