Legend has it that “Nero fiddled while Rome burned.” This legend is not true.

First of all, the fiddle hadn’t been invented yet. And even if this legend is taken metaphorically, most accounts put Nero in Rome trying to help during the fire.

This was in the year 64 A.D. The fire lasted six days. It leveled almost three quarters of the city.

When surveying the damage, Nero decided to build a large palace on the ruins of part of the city. That’s one reason the fiddle legend became engrained in history.

It’s easy to assign an evil motive for the fire when we think of the decision of where to build a palace. The truth is more complex.

By some accounts, Nero cared about the citizens of Rome. He developed roads to ensure there was access to food. He built a covered marketplace to help relieve the discomfort of the weather. He enforced tougher building standards after the fire.

These and other good deeds are less memorable than the image of a tyrant fiddling as he watched flames consume Rome. And the phrase “Nero fiddled while Rome burned” became a metaphor for inaction in times of crisis.

I mention this story because it helps to illustrate how the Federal Reserve is handling the current state of the economy…

The Fed is certainly not inactive. But it also has a lot of fires to put out. And spraying the hose in one direction leaves the fire in another to grow out of control…

There is a way to boost your portfolio’s performance during this economic fiasco that many of you haven’t considered, and still won’t after you read this. But the rare few of you that do will likely see rewards.

The U.S. Economy Flares Up, and the Fed Watches

Fed Chairman Jerome Powell could be likened to emperor Nero. He has done many things right. But the Fed’s decision to wait for additional data before raising rates is concerning. Because it further risks sparking a fire in the economy.

If prices rise much further, many families will be left behind.

For example, while inflation did drop to 4% in the latest CPI report, grocery prices are still too high. The cost of food at home is up almost 20% in two years. At the same time, wages are up 4.3%.

No one wants to hear about the lagging effect of Fed policies when they check out at the grocery store. They want to see lower prices.

It’s not just the grocery store that is on fire. Home prices are up sharply since the pandemic. And this isn’t just a problem in the U.S. The International Monetary Fund believes there is a high risk of a housing crisis in 15 of the 38 developed economies they track.

The Fed should be trying to help families battle inflation. But that requires high interest rates. And other powerful people don’t want high rates.

Low interest rates allowed Congress to pass budgets with trillion-dollar deficits. If interest rates rise, debt costs more. Even a 1% increase in financing costs could cost the government more than $300 billion.

That’s a lot of money, even when revenue is nearly $5 trillion a year.

But this isn’t just a national issue. Outside the U.S., economies are struggling to maintain growth. We know that a recession threatens the economic expansion of the U.S.

Germany (Europe’s largest economy) and the U.K. are no longer threatened with recessions — they’re already in them. European emerging markets are expected to slide into recession this year. And China’s growth is slowing.

The Fed should be trying to help boost global growth. But that requires lower interest rates. Low rates help increase business investment and that creates jobs. It’s a formula for growth central bankers have relied on for hundreds of years.

Of course, lower rates would make inflation worse. This sums up the Fed’s problem.

No matter what Powell does, he faces problems. The best course of action could be to just pull out his fiddle and watch the flames from afar.

As for us individual investors, it’s not a time to be idle. Times of crisis — or as Nero might’ve put it, when everything is on fire — present plenty of profits to be made.

The best thing for us to do as investors is to fasten our sights on short-term trading opportunities that arise in volatile times. That’s exactly what we do each morning in the Trade Room at the market’s open, five days a week.

One of our most popular strategies has beat the market 33X over the last two months (April and May). And there’s new ones I’m designing and testing with the Trade Room community as well.

See what kinds of cutting-edge techniques we’re currently using to find new trades by clicking here.

Regards, Michael CarrEditor, Precision Profits

Michael CarrEditor, Precision Profits

Why It Pays to Think Short-Term

On Tuesday, I noted that U.S. consumers have let their credit card spending get away from them again. Total credit card debt is close to touching a trillion dollars for the first time.

Let’s dig a little deeper into those numbers.

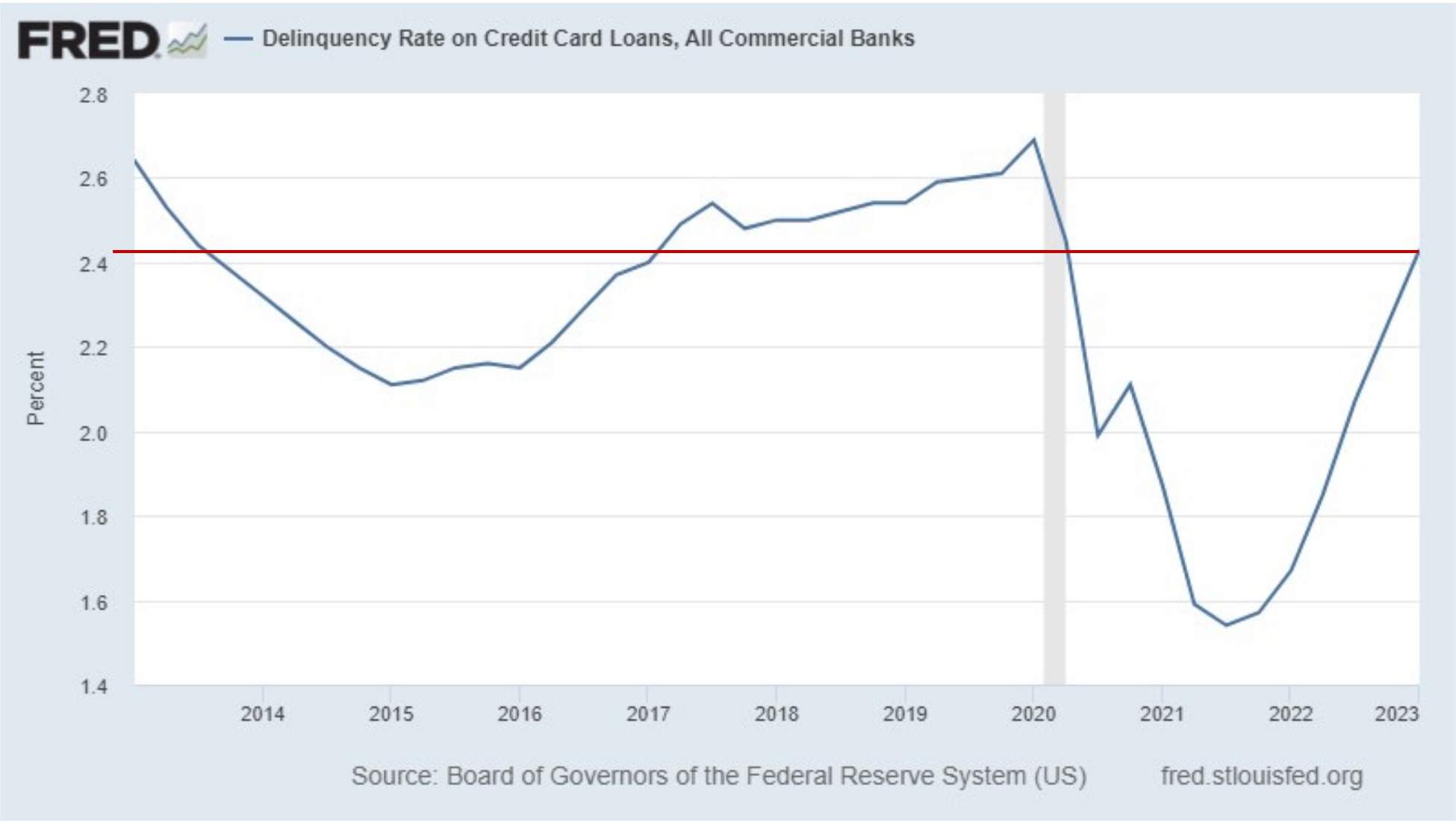

Credit card delinquencies (30 days or more late) have followed the same basic pattern of credit card balances.

These delinquencies dropped to record lows in 2020 as higher income due to stimulus, less credit obligations due to freezes on student loans and even rent in some situations. There was also a general dearth of things to spend money on during the pandemic.

And these all worked to reduce delinquencies. As credit card balances have risen, so have the late dues. Today, the delinquency rate is roughly in line with the average of the years prior to the pandemic.

Why This Is Happening

We’re swiping the cards more because, following the pandemic, we’re making up for lost time on expensive experiences, like vacations. I’m taking my kids to Europe for the first time in July, and I already have heartburn looking at the expenses pile up.

But then there are some wilder contributing factors, such as high inflation. This is forcing us to spend more on regular, basic necessities, and the tapering of government stimulus payments.

But here’s the thing.

Even if a recession isn’t coming soon, we’re about to see the delinquency rate spike much higher.

The pause on student loan payments — which allowed nearly 40 million Americans to avoid costly monthly payments for the past three years — is set to be lifted in another two months. Millions of Americans are going to have to prioritize their student loan payments over other debts … like their credit cards.

For weeks now, I’ve been saying that I expect a recession within the next three to six months. Is the resumption of student loan payments the straw that breaks the camel’s back?

I think it very well could be.

Mike Carr believes the best way to navigate the unknown in this market is by being nimble — with short-term trades. Getting in and out with your gains to avoid the dips and capitalize on the spikes.

Interested in learning more about Mike’s most popular (and successful) trading techniques? Go here to check out his Trade Room.

Regards, Charles SizemoreChief Editor, The Banyan Edge

Charles SizemoreChief Editor, The Banyan Edge