Last week, I warned that the real estate market is in a bubble territory.

The survey revealed that 76.2% of you agreed with my assessment, and many of you shared your thoughts…

- No way prices will rise to higher rates. —

- WE ARE SCREWED! My wife and I have been residential investors for many years and we have seen many scenarios play out, as I’m sure you have. The small house movement is really picking up due to, as you said, high interest and already ridiculous house pricing… Prices for a 500 square foot house… Really!!!!!! —

- A great help in understanding and perspective. Your charts richly aid understanding. (If we look up and see the guillotine blade falling, the situation will be clearer.) —

These are just a few of the responses I’ve received. I enjoyed reading all of your letters. Thank you for the feedback.

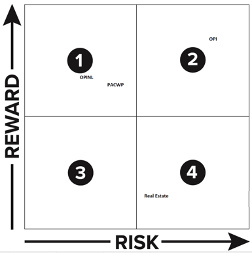

But, as many of you rightly pointed out, avoiding “high-risk, low-reward” investments is just the first key to achieving financial freedom. The second key is finding Zone 1 opportunities.

I’m talking about “low-risk, high-reward” investments.

Zone 1 is where fortunes are made.

It’s the type of investment opportunity that jumps out as a “no-brainer, can’t-miss” opportunity.

Like real estate was from 2010 through 2020. But as prices rose, along with interest rates, it moved to Zone 4.

Today, I’m going to reveal a Zone 1 opportunity. A company that pays most people a .54% dividend … yet, it pays me a 19.59% dividend.

Yes, I’m getting paid 36 times more than most people!

You may want to scoop it up yourself.

The Secret to My 19.59% Dividend Check:

The Letter “P”

This past May, banking stocks were getting hammered after the Silicon Valley Bank disaster. The entire financial sector was in distress.

Including, PacWest Bancorp (Nasdaq: PACW).

PacWest is a small regional bank (market cap under $1 billion) located in Beverly Hills. It mainly services commercial loans.

So, when Silicon Valley Bank crumbled, PacWest was the baby that was tossed out with the bath water.

The company announced that it would lower its dividend from $0.25 to $0.01 to keep cash on hand.

Shares slid from $49 a share all the way down to $3 a share.

Everybody was ditching the stock. Surely, it too would go bankrupt. Or would it?

I asked Ian King if I should buy any shares on the cheap. He said the risk was too high. Instead, he told me about an alternative…

Just add a “P” to the end of the ticker symbol.

That’s right.

Instead of typing in the normal ticker symbol, PACW, I typed in PACWP.

That one letter opens up an entirely new avenue to make money in the stock that is more lucrative AND safer.

Because I was no longer buying ordinary shares of the company.

I was buying preferred shares.

You see, when a company raises money, they typically sell shares of common stock or raise money through bonds.

But there are other options…

Like preferred shares.

Preferred shares of a company are the best of a stock and a bond.

Typically, shares sell at $25. The buyer usually gets a higher dividend … 5%, 6%, 7%. Whatever the market is willing to pay.

And here’s the best part… Unlike normal dividends, which a company can cut at any time, a company must pay the dividends from preferred shares. It’s the law.

The only knock on preferred shares is that they are limited on the upside. They normally don’t trade much higher than $25. They trade more like a bond. The only case might be if the Federal Reserve lowers interest rates and income seekers start bidding up the stock in search for higher income.

Take PacWest as an example.

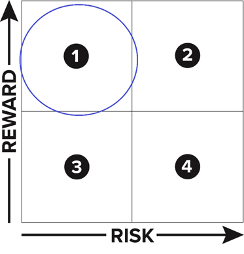

In 2022, the bank sold preferred shares at $25. They offered a dividend of 7.75% (or $1.94 per year). That’s a pretty juicy dividend.

As people sought income, PACWP traded as high as $26.79 in February (blue circle below). But then, when the banking crisis hit just one month later, people questioned if PacWest would go bankrupt. Shares plummeted.

But the more my team and I looked into the company, we could see that it was much safer than Silicon Valley Bank.

Thanks to Ian King’s timely recommendation, I was fortunate enough to scoop up preferred shares at $9.89 (green circle).

And since the bank shares MUST pay preferred shareholders $1.94 a year, my dividend yield comes out to 19.59%.

You can buy the shares of PACWP today if you would like. They trade around $19 a share and still pay out $1.94 a year. That’s a yield of 10%. Not bad.

I still consider it a Zone 1 opportunity.

Low risk, high reward.

But you may have never bought a preferred share before and wonder if this is a little too fringe. If so, you should know that I’m not the only one who loves these preferred shares.

How Warren Buffett Used Preferred Shares to Lock in a $250 Million a Year Income Stream

In 2011, the United States was still coming out of the financial crisis, and Washington was fighting over the debt ceiling.

Banks were struggling.

Bank of America’s once $50 stock sank to $10 a share.

They needed a boost of confidence.

The Oracle of Omaha, while taking a bath, came up with a genius idea.

He dried himself off, and hopefully put on some clothes, and then called the CEO of Bank of America. He stated that Berkshire would invest $5 billion into the company. But he didn’t want the common shares. He wanted preferred shares that guaranteed him a 5% dividend along with a guaranteed 5% profit.

So, $250 million a year in income along with a $250 million bonus to boot.

(There were other perks too that I won’t get into because only a billionaire can negotiate those terms.)

Buffett stated he’s been looking for more great deals like that one. “I’ve spent a lot of time in the bathtub since and nothing’s come to me. Clearly, I either need a new bathtub or we’ve got to get to a different kind of market.”

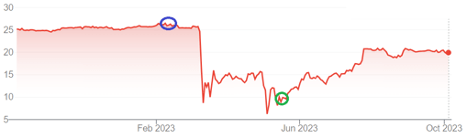

Fast-forward to today and BAC currently pays a 3.5% dividend.

But the preferred shares pay much more. Just go to your brokerage account, type in the ticker symbol and put a period at the end — “BAC.” — and you’ll see 10 preferred shares pop up.

There are all kinds of preferred shares.

Typically, they pay 6.5%.

And while that is good, I would put that in the “low-risk, low-return” zone (Zone 3). So, I don’t own any of these shares.

However, there is another deal I’m loading up on.

If you thought Buffett’s 5% guaranteed return and 5% guaranteed profit were juicy, you’ll love this.

My Zone 1 Opportunity:

A 13.01% Annual Return and a 100% Profit … From Uncle Sam

I’m going to invest some money in the preferred shares of Office Properties Income Trust (Nasdaq: OPI).

This is a real estate investment trust (REIT). It owns 155 office properties and has a 90.6% occupancy rate.

Of course, with the work-from-home movement, there is a reason to be cautious about investing in office properties. As mentioned, I am not a huge fan of real estate right now, and that includes commercial real estate.

But here’s what makes this a no-brainer opportunity: Its largest tenant is the U.S. government.

The vast majority of its offices look like this one in Reston, Virginia … just outside of Washington D.C.

And if there is any organization that continues to grow, it’s the U.S. government.

Washington added 75,000 more employees in the last year.

That’s a 5% increase.

And Biden announced that he wants to add another 81,000 next year.

While I hate to think about how much this will cost us in taxes, I do see a way to profit from the “Rich Men North of Richmond.”

Through Office Properties Trust, you can collect income from Uncle Sam and this never-ending expansion.

Now, when you look up the ticker symbol, OPI, you’ll see that it pays a 20% dividend. That is massive. Too massive, and too tempting, in my opinion. There is a chance they will cut that dividend in the future. That is a Zone 2 investment … high risk, high reward.

However, by law, it cannot cut its preferred shares. They are legally obligated to pay shareholders a 13.01% dividend.

The ticker symbol is OPINL.

It trades for just $12.50 a share and pays $1.60 a year.

Here’s what’s interesting about these preferred shares: They also have a (nearly) guaranteed 100% profit … if you wait long enough.

You see, they act more like a bond and are due in 2050.

Think about that … you can buy shares today at $12.50 and Office Properties Trust will be required to pay you $25 per share in 2050 … and a 13.01% yield every year until that day arrives.

So, you’re getting a Warren Buffett-type deal, and you didn’t even need to know the CEO of the company.

For every $10,000 I invest, I plan to make $32,570 in income over the next 26 years, and in 2050, I’ll get a $20,000 payout.

But you may not have to wait that long.

Why?

Because historically speaking, when the Federal Reserve increases interest rates rapidly, it goes too far and then has to decrease rates rapidly.

And when that happens, income seekers will be willing to pay $15, $20, maybe even $25 for shares of OPINL. So, you could potentially sell these preferred shares for a nice gain.

In the meantime, I will gladly collect my 13.01% dividend.

Let me know if you decide to join me on this investment, or if you have any questions. My email address is AaronJames@BanyanHill.com.

Aaron James

CEO, Banyan Hill Publishing and Money & Markets

P.S. If you like Zone 1 investment opportunities, I’ve got a great one for you: Ian King’s Strategic Fortunes. He’s the one who told me about preferred shares and his team helped me research OPINL. His top closed recommendations include…

If you want to become a member and get access to his next recommendations, email me at AaronJames@BanyanHill.com … I’ll have my team knock 75% off the subscription price (from $200 a year to $47 a year), and it comes with a 100% satisfaction guarantee. If you don’t like what you see, just email me. It’s that simple.