A friend of mine says…

“Never run out of month before you run out of money.”

It’s a more interesting way to say: “Don’t spend more than you make.”

If you earn $50,000 a year, but spend $60,000 a year, you accrue $10,000 in debt.

$50,000

– $60,000

($10,000)

Then, you have to pay interest on that debt, compounding the damage.

You either have to earn more, or reduce spending, or both. Otherwise … you default.

On a personal level, I think we all get it.

It’s 3rd grade math, really.

But apparently, the politicians in Washington, D.C., never took 3rd grade math.

They now “earn” (via taxes) $4.4 trillion a year. They spend $6.1 trillion. Leading to $1.7 trillion in debt a year.

$4.4 Trillion

– $6.1 Trillion

($1.7 Trillion)

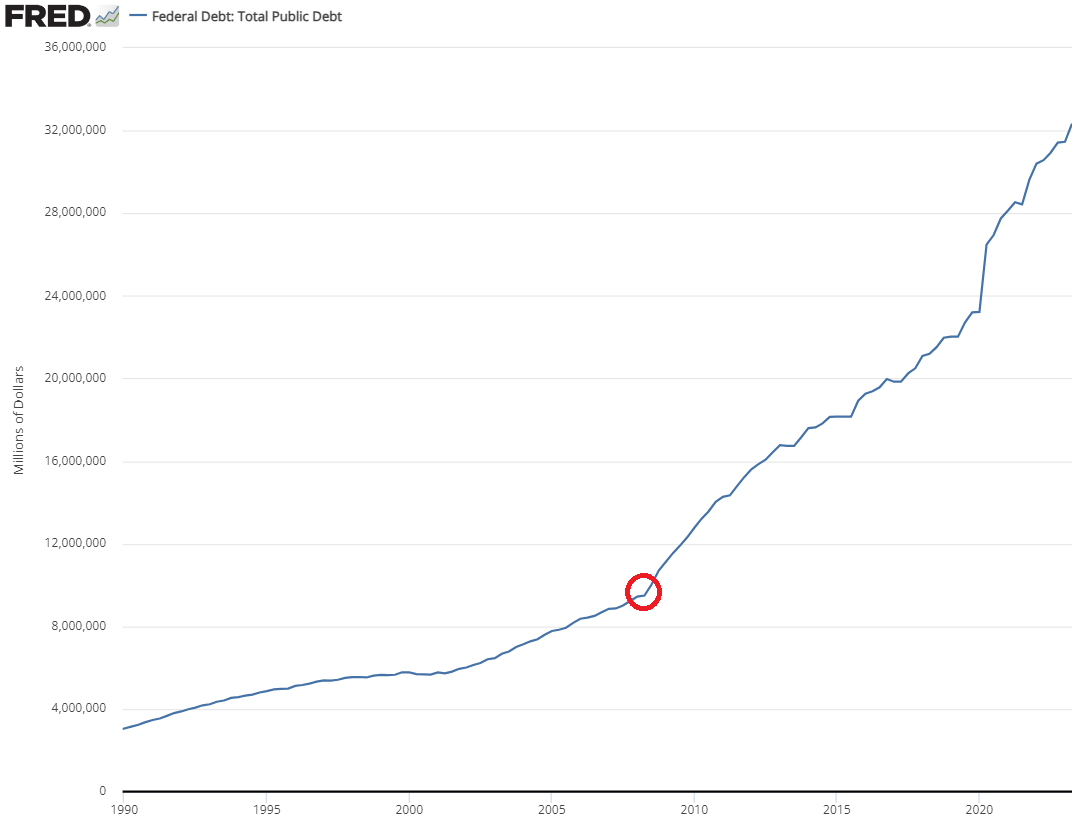

Which is why our country is now approaching a total debt of $34 trillion…

To put that in perspective, we were only $10 trillion in debt when we entered the 2008 crisis (red circle) which led to Standard & Poor’s downgrading our debt a few years later … from AAA to AA+.

We are now 3X higher, in just 15 years.

And it seems to be climbing faster, faster and faster. Making the U.S., weaker and weaker.

Washington either needs to make more (increase taxes) or cut back on spending.

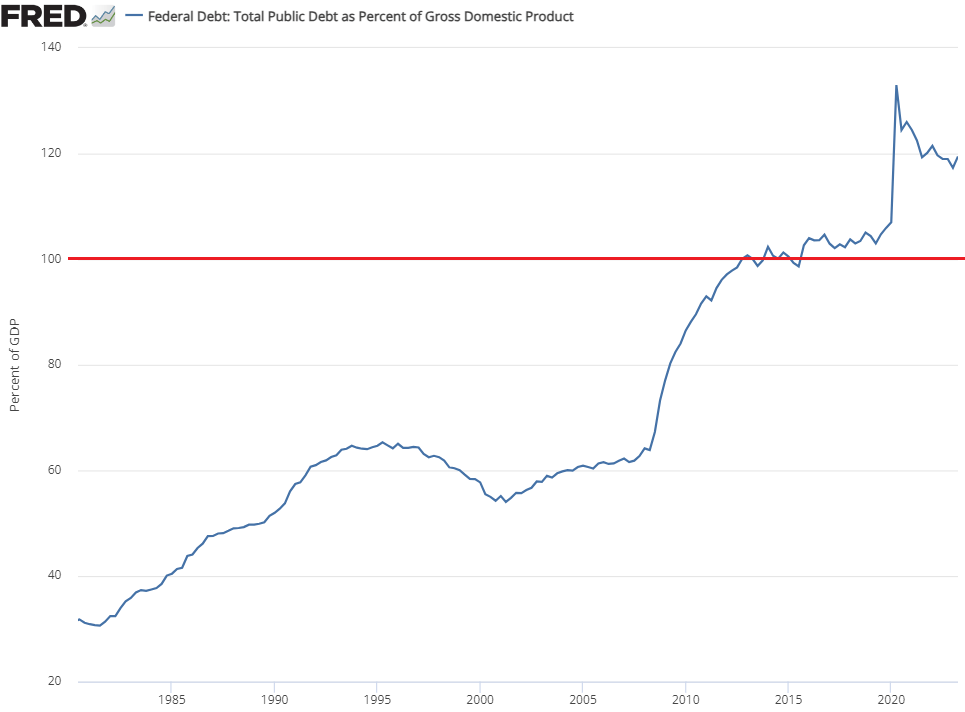

Historically, we’ve been told that spending is not a concern because our GDP was growing faster than our debt.

But, recently, that changed.

Our debt-to-GDP ratio has crossed the 100% mark.

See that red line?

That is when our debt became more than 100% of our GDP … meaning, our economic output cannot keep up with the amount of debt we are taking on.

The Congressional Budget Office projects that we will be at 180% by 2050.

Now, does this mean “the End of America?”

That you should sell all of your stocks and stuff your money under the mattress?

Well, let’s look at history as a guide.

Taking on massive debts is one of the main reasons most empires fell. From the Roman Empire to the Spanish Empire to the French Empire, debt was, ultimately, the final dagger.

Which is why the Founding Fathers were well aware of the dangers of debt.

James Madison called it a “public curse.”

He said that “armies, and debts, and taxes are the known instruments for bringing the many under the domination of the few.”

Thomas Jefferson called “public debt as the greatest of the dangers to be feared” and later wrote that “the principle of spending money to be paid by posterity, under the name of funding, is but swindling futurity on a large scale.”

George Washington warned against debt as well, arguing in public speeches that money should be borrowed sparingly and paid back promptly.

And Ben Franklin warned that debt gives another “power over your liberty.”

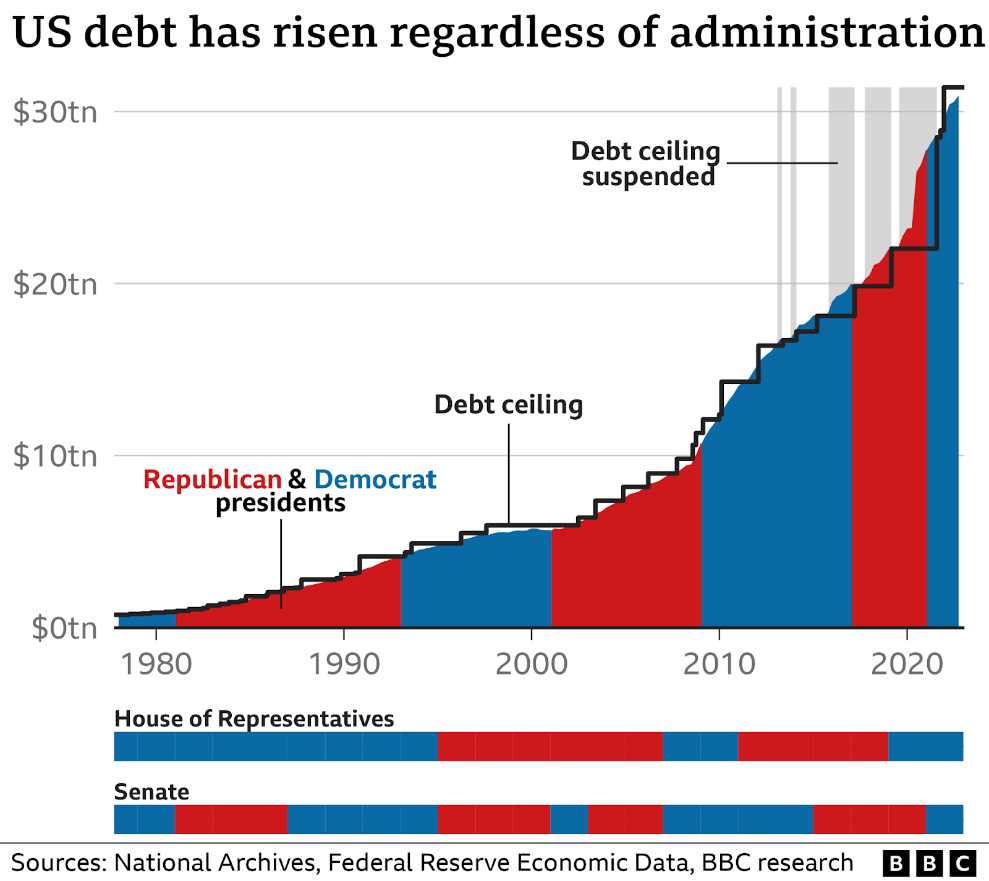

Yet, it’s as if our current politicians have never heard these warnings.

They just go further, and further, into debt.

It’s the one thing Democrats and Republicans have in common. Our public debt has risen regardless of who controls the White House or Congress.

Both parties love to spend to appease their constituents.

They just debate what they want to spend the money on.

But things seem to be getting out of control.

In August, Fitch joined the Standard and Poor’s by downgrading U.S. debt from AAA to an AA+.

Both downgrades followed a close call with paying our bills on time, the debt-ceiling debate.

And now we are back to the usual spending standoff, again. Washington has to come up with a solution before November 17 to prevent a new government shutdown.

The last debate like this ended with the Speaker of the House getting the boot. We have a new speaker now, but precious little is different about the basic financial facts: We need to either increase revenue, or cut costs.

Now, I’m not one to vote for paying more taxes. I personally think an increase in taxes could backfire. Taking more from individuals just means they will have less to spend, hampering the growth of the economy.

But, can we make cuts?

Yes.

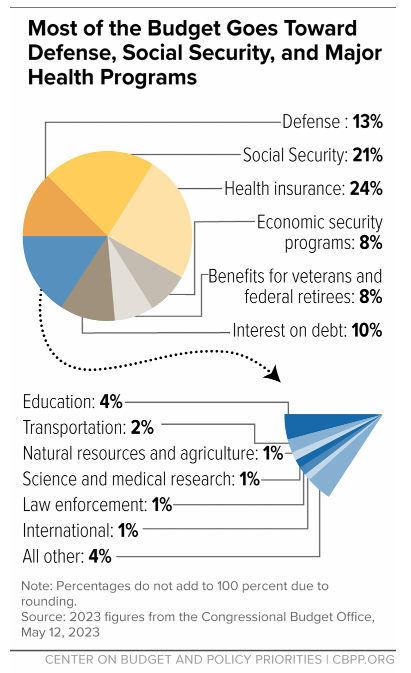

To do that, look at the simple pie chart to the right. It shows where all the money is going.

Somewhere in there, we have to make concessions.

That’s where things get sticky. One person wants to cut defense, another education and another law enforcement.

The big problem is this … the “interest on debt: 10%.” That is going to increase to 15%, 20% and higher.

That’s simply because the Federal Reserve has increased the interest rate.

It’s not just ordinary people who have to pay more for debt…

Uncle Sam has to pay more too.

The 10-Year Treasury has gone from 1% to more than 5%.

This year, the federal government is on track to spend $879 billion on interest … up from $350 billion two years ago.

That’s a big jump.

And it will only get worse.

So, again, will it cause “the End of America?”

No.

But it will be an ever-increasing drag on our economy.

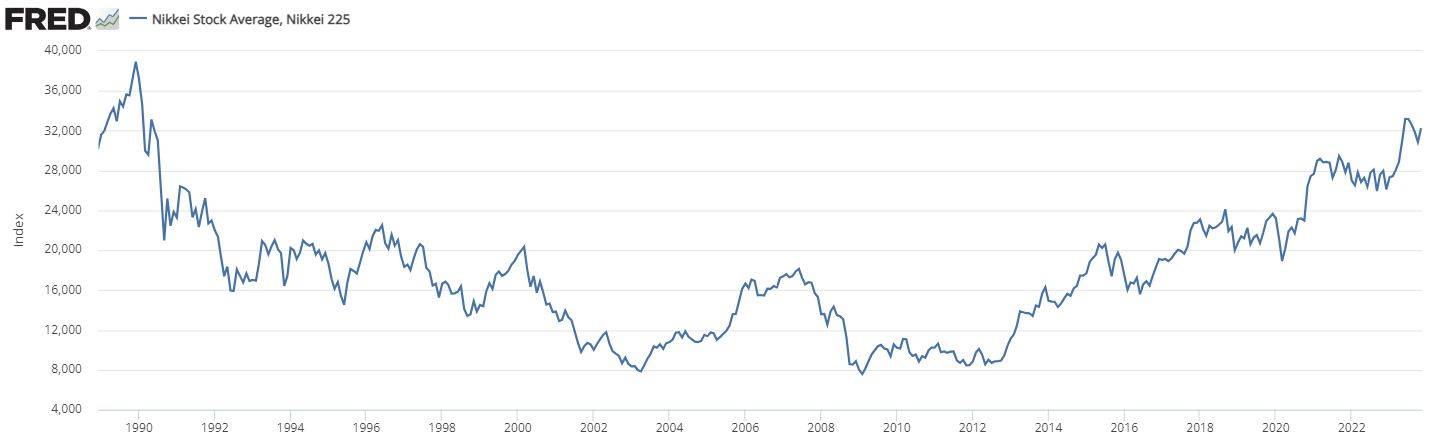

If we want to see our future, look to the past … Japan’s past.

Japan first crossed the “100% GDP to Debt” threshold in the 1990s, and it’s only gotten worse.

They are now at 255%.

And, look at their stock market…

After 30+ years, anyone in the Japanese stock market, is still down.

Yet, it’s not the “end of Japan,” nor will it be the end of America.

But, it is a big drag on the economy.

With that said, there are Japanese companies that have made investors a lot of money over the last decade.

- Nippon Telegraph is up 470%.

- Fast Retailing is up about 800%.

- Sony has gone up as much as 1,000%.

I think the same situation will emerge in the U.S.

Historically, we could invest in the U.S. economy … in “the stock market” … through an S&P 500 fund.

And that did well for us.

But in the years to come, I suspect many of these companies will struggle and the entire “stock market” will start to lag.

Truthfully, we are already seeing this play out.

While the S&P 500 is relatively flat this year, a handful of companies have accounted for all the gains…

- Amazon is up 58%.

- Tesla is up 63%.

- Nvidia is up 179%.

Those who invested in those companies have done very well.

But, we are entering an era where it is important to invest a good amount of your money in specific stocks.

Those who do invest selectively will make more money than ever.

Those who fail to do so will lose out.

That’s one of the reasons I have worked so hard to recruit great investors to Banyan Hill and our sister company, Money & Markets.

One of those guys is Charles Mizrahi. He runs a service called Alpha Investor.

And one of the four things he looks for in a company is sound finances … basically, a strong cash flow, especially relative to debt.

Since he joined our team in 2019, his investments not only survived the 2020 crash and the 2022 bear market, they thrived.

Investments that are up as high as 121%, 144%, 168% and 429% … and they’re still rising!

Why?

Because, unlike our elected officials, the CEOs who run these companies understand that cash is king. And during tough times, they can expand.

These CEOs love a tumultuous market.

And shareholders are richly rewarded.

If you’re one of our 80,000 subscribers to Charles’ Alpha Investor service, you are in good hands.

If not, I urge you to watch this interview he did with Mike Huckabee called “Miracle on Main Street.”

In it, Charles explains exactly what this service is like, and how you can try it out 100% risk-free.

Aaron James

CEO, Banyan Hill, Money & Markets

To learn more about Charles Mizrahi’s “Miracle on Main Street”, click here.

How do I invest in the fusion company with the thousands of patents? What is the name ?