CAPE TOWN, South Africa — My wife keeps elbowing me in the ribs … all because of debt.

To be more specific … about lack of debt.

I was elated when we paid off the mortgage on our house in the seaside suburb of Muizenberg, in Cape Town. I bought the place years ago — my first home — then refinanced in the early 2000s to add some space.

I was elated when we paid off the mortgage on our house in the seaside suburb of Muizenberg, in Cape Town. I bought the place years ago — my first home — then refinanced in the early 2000s to add some space.

Retiring my first major debt felt liberating!

But my wife thinks I shouldn’t talk about it. After all, so many people here are battling financially. She worries about their feelings.

At least my South African friends have an excuse for indebtedness. After years of mismanagement by a corrupt government, the economy is only slowly recovering under new leadership. People had to borrow to survive.

But another class of debtors has no such excuse. Instead, they’ve squandered a huge opportunity to pay down debt … in fact, they’ve taken on even more.

Who are these spendthrifts? U.S. corporations … and with interest rates rising, you should examine their balance sheets before you spend a single penny on their stocks.

Drowning in Debt

U.S. companies currently owe more debt than at any other time in history. With rising interest rates, that debt is a time bomb that will bankrupt firms, destroy jobs … and send the stock market crashing.

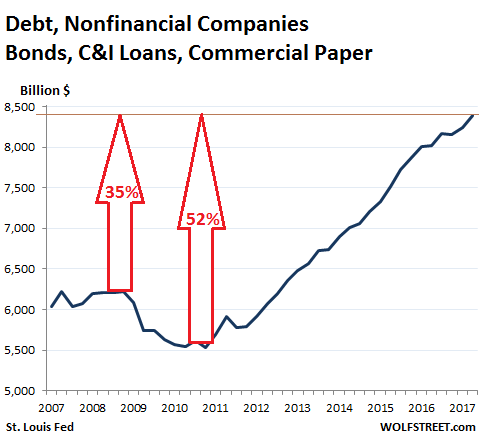

Encouraged by a decade of low borrowing costs, the U.S. corporate sector has accumulated $6.3 trillion of debt. And that doesn’t include highly leveraged U.S. banks.

That’s more than double what they had in 2010. It’s also 35% higher than the debt load just before the crash of 2008.

That’s more than double what they had in 2010. It’s also 35% higher than the debt load just before the crash of 2008.

But wait … isn’t the U.S. corporate sector cash-flush? Aren’t profits sky-high?

Yes indeed. According to S&P Global Ratings, the 1,900 U.S. companies it rates hold $2.1 trillion in cash.

The problem is that the richest 1% of U.S. companies control more than half of it. Seven of these companies share $800 billion: Apple, Microsoft, Alphabet, Cisco, Oracle, AT&T and Amgen.

At the other end of the spectrum, hundreds of U.S. corporations are more leveraged than at any time in history. They’re holding $8 of debt for every $1 of cash!

An Accident That WILL Happen

This is essentially the same situation that faced the U.S. housing market in 2008. U.S. households were leveraged to the hilt. They relied on increasing house values to make the purchase work.

Until it didn’t.

Debt-heavy U.S. companies are doing the same thing. They’re betting on increasing stock valuations to make their debt-to-equity ratios look good.

Until they don’t.

As interest rates rise, two things happen. Investors move out of stocks and into bonds, putting downward pressure on prices. The increasing cost of debt service weakens companies’ cash flow and balance sheets.

This scissor-like movement will eventually cull hundreds of firms. The lucky ones will be bought out. The others will die.

Back to the Fundamentals

Which will be which? And how can you know?

My own trading service, Alpha Stock Alert, incorporates indicators of market sentiment to identify our picks. One of the biggest drivers of analyst sentiment is the financial health of a company. As interest rates rise, those indicators will tell us to pull out of firms in danger.

You can do the same thing — and protect yourself from loss — by paying attention to the financial position of the firms in your portfolio. Everything you need to know is right there in the financial statements:

- Current ratio (current assets divided by current liabilities): This is used to determine the company’s ability to pay back its short-term liabilities. The resulting number should be between 1.5 and 3. A current ratio of less than 1 means the company doesn’t have enough cash coming in to pay its bills.

- The total-debt-to-equity ratio (total liabilities divided by shareholders’ equity): This can be expressed as long- or short-term debt. The optimal debt-to-equity ratio varies by industry, but the consensus is that it should not be above 2.

- Negative leverage: This is when a company’s total annual interest expense exceeds its net operating income margin. It’s a death knell.

Publicly traded companies are required to publish their financial statements for a reason — so investors like you can calculate ratios like these and decide whether it’s safe to invest.

If you’re not doing this already, now would be a great time to start.

Kind regards,

Ted Bauman

Editor, The Bauman Letter

Editor’s Note: Value expert Jeff L. Yastine’s relationships with some of the world’s top investors, such as Steve Forbes and Warren Buffett, led him to the discovery of a little-known investment program. Jeff now considers this program to be the single most powerful way for an investor — regardless of how much or how little they have — to multiply their wealth tenfold over and over again. To see why Jeff’s readers are singing praises about their results from this lucrative program, click here.