The California Public Employees’ Retirement System manages almost $400 billion.

CalPERS, as the fund is known, recently reset its portfolio. To see how it fared in recent volatility, I turned to its annual report.

Right from the start, I knew I was in for a unique experience. Page 1 listed awards the managers won.

There was a copy of a Certificate of Achievement for Excellence in Financial Reporting. That came before performance numbers or details on investment strategies.

It was almost funny … except for the fact over 1.9 million California employees depend on the fund for retirement income.

Reading more, I thought CalPERS might focus on awards because there are concerns under the surface.

The fund only has about 71% of the assets needed to pay future benefits. Shortfalls require higher taxes, higher contributions from employees, lower benefits or better investment returns.

The first three options are painful. So CalPERS chose to improve performance results.

Its target is 7% a year. On page 103 of the report, I saw the average gain was 5.6% over the past 10 years.

This is a big problem.

Experts found there was less than a 40% chance of having enough money to pay promised benefits. So, the fund reset its policies.

And that provides an important lesson for investors.

This Pension Fund Made Some Questionable Decisions

CalPERS decided to borrow money to invest. It will also use futures contracts to increase returns.

Now the fund can invest up to 120% of its assets. If all goes well, this strategy increases gains.

You don’t personally manage a $380 billion fund, so you probably see the problem: Losses will be higher if the strategy doesn’t work.

You’re right. But the managers can’t think about that. The other choices they face are politically unacceptable.

Managers also decided to increase the amount they invest in private equity funds. These funds are illiquid. That matches CalPERS’ timing.

The fund needs money to finance pensions 30 years from now. Private equity locks up money for years at a time. In theory, illiquid investments deliver larger returns.

CalPERS implemented that theory by allocating almost $30 billion to an asset class that underperformed the S&P 500 Index over the past 20 years.

Despite these questionable decisions, CalPERS did something we can learn from. It realized returns were lagging and reset its portfolio.

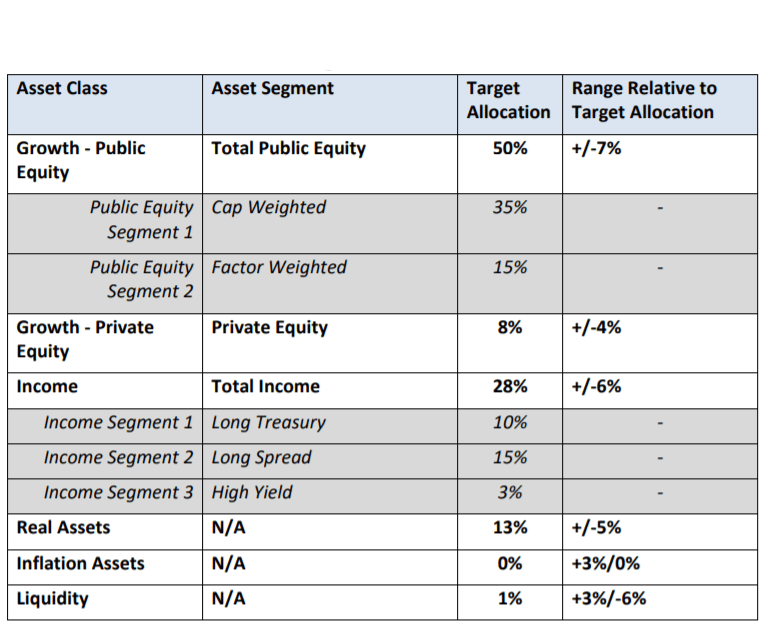

Its current allocations are shown below.

CalPERS’ Portfolio Reset

(Source: CalPERS)

As individuals, we can benefit from something like that. An allocation strategy helps investors stick to plans in both good and bad markets.

It’s Time to Reset Your Retirement Plan

Notice CalPERS uses a range. This avoids active trading. It keeps the investments on track for the long term.

After the recent market sell-off and rally, now is an ideal time to reset your retirement plan.

Consider the following:

- Did you have a plan?

- Did you stick with your plan during the decline?

- Did you stick with that plan in the rally?

- Does your plan need some adjustments?

The answers should be obvious. Many of us need some adjustments.

If you were uncomfortable with the size of your losses in the decline, consider adding Treasury bonds. If the rally disappointed you, increase your equity investments.

This framework is useful. Just don’t act like CalPERS.

Avoid leverage in your retirement account since that increases risk. And avoid high-fee investments such as in private equity.

Over time, you can outperform CalPERS.

Regards,

Editor, Peak Velocity Trader