Gold miners are heading higher, but the real gains are in front of us.

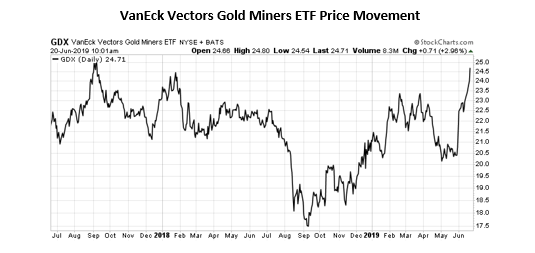

The price of gold bullion just hit its highest price since early 2018. This rise began after the yellow metal bottomed in August 2018 at $1,174 per ounce.

Gold is up 15%. The VanEck Vectors Gold Miners exchange-traded fund (ETF), which holds most of the big gold miners, rose 34%.

You can see it on the chart below:

Some investors would look at that move and figure they were too late. In this case, they are wrong. There is a bigger boost coming…

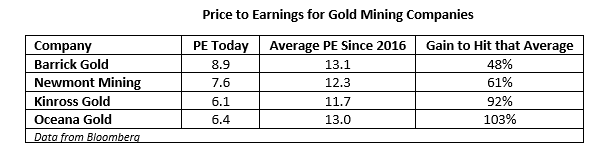

Gold Prices Rise but Price to Earnings Stays Low

You see, the gold price rose in anticipation of the Federal Reserve lowering interest rates this year. The market puts the odds of a rate cut at 97.6% likelihood by December 11, 2019.

In other words, the market thinks this is going to happen.

The higher gold price means we should see outsized second-quarter revenue and profits. According to Bloomberg’s estimates, giant gold miner Newmont Goldcorp will get a 30% boost in revenue in the second quarter. That will send its net income up too.

And right now is a great time to buy the big miners. Here’s what I see on a price-to-earnings (P/E) basis:

We calculate our own P/E metric here. We use enterprise value divided by earnings (before interest, taxes, depreciation and amortization, or EBITDA). Those numbers give us a clear picture of the valuation of the company.

A little detail on the chart data. For Barrick, Newmont and Kinross, we used second-quarter earnings forecasts to calculate the P/E today.

OceanaGold doesn’t have a forecast, so we used current numbers. Even without the forecast, the company’s price needs to rise 103% to get the P/E back to average. That’s a huge opportunity!

Another Boost for the Gold-Mining Sector

In simple terms, the P/E ratio tells us how many years’ worth of earnings it would take to buy the company. For example, the current P/E ratio of the S&P 500 Index is 21.9 times.

That means it would take nearly 22 years of earnings to buy the S&P 500 right now. Compare that to gold miners, which are under nine years.

Low P/E data tells us that the market hasn’t done the math for gold miners yet. The stocks remain cheap relative to their earnings.

That’s due to something called “recency bias.” Gold stocks were terrible investments from 2011 to 2015, and from 2016 to 2018. Most investors don’t even think about gold miners as a possible investment idea right now.

That’s great for us, because it means the gains in the gold price have not hit the shares of the gold miners yet. They are still cheap — an opportunity for us to buy and profit.

An easy way to play this trend is through the VanEck Vectors Gold Miners ETF (NYSE: GDX) or the VanEck Vectors Junior Gold Miners ETF (NYSE: GDXJ).

Both give us exposure to the whole gold-mining sector, which is exactly what we want right now.

Good investing,

Matt Badiali

Editor, Real Wealth Strategist