Friday Four Play: The “Data Center Debauchery” Edition

Let loose the dogs of war and break out the bourbon, Great Ones, ‘cause it’s Friday! Freedom!

Well, it’s not freedom for everyone. I’m sure that Intel (Nasdaq: INTC) executives will be working overtime for the foreseeable future. The former semiconductor king presented what appeared to be an impressive second-quarter earnings report yesterday.

I say “appeared to be” because there are some rather serious cracks in Intel’s operations … and Wall Street is taking notice.

Let’s start with the headline numbers:

- Earnings per share: $1.28 versus $1.07 expected.

- Revenue: $18.5 billion versus $17.8 billion expected.

Looks pretty good, right?

Intel also lifted full-year 2021 revenue guidance to $73.5 billion on earnings of $4.80 per share. Both figures were above Wall Street’s expectations.

Now, this may look like a classic 2021-two-step situation. A double-beat-and-raise that leaves investors wondering why INTC stock fell more than 5% today. But a closer look at Intel’s numbers quickly reveals why the stock plummeted … and why we sold INTC out of the Great Stuff Picks portfolio last month.

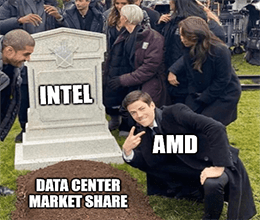

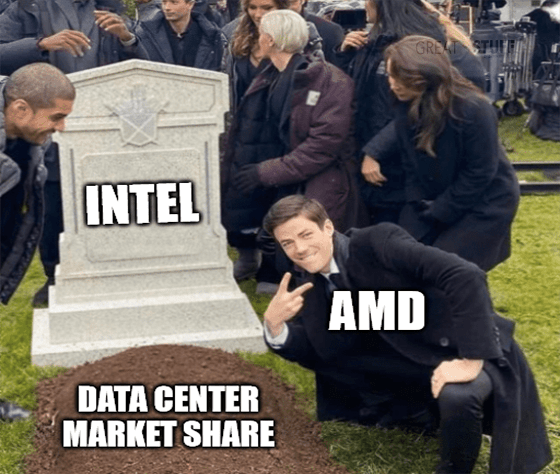

Specifically — and most notably — data center sales were way down. Like, they fell 9% to $6.5 billion in revenue. Sploosh. Just walked right off that cliff.

But “walked” isn’t the right word … no, sir! Advanced Micro Devices (Nasdaq: AMD) pushed Intel off the data center cliff. And when the Intel rival releases its own results next Tuesday, we’ll find out just how much of that 9% drop went AMD’s way.

Hint: It’s looking even better for any AMD options trades you Great Ones might’ve jumped into after my little exposé two weeks ago.

But while a drop in Intel’s control of the data center market was the biggest bombshell, there were other equally disturbing cracks in the company’s report.

For instance, while PC chip sales rose 6% to $10.5 billion — a surprise to be sure, but a welcome one — Intel said that the average price of PC chips declined, raising margin concerns for investors.

Furthermore, Intel is in acquisition mode to make up for its manufacturing shortcomings.

It already pledged $20 billion to improve in-house manufacturing, and it’s building two new factories in Arizona. But Intel is also in talks to acquire GlobalFoundries — ironically, this is AMD’s old in-house chip manufacturing business, which it spun off back in 2008.

Intel is also considering buying SiFive, a silicon manufacturer that competes directly with ARM Holdings — you know, that mobile chipmaker that Nvidia (Nasdaq: NVDA) is buying? Oof.

This means more debt for Intel and more doubt for INTC investors.

And if that wasn’t enough, Intel server design guru Navin Shenoy left the company last month after 26 years of leading the company’s Data Platforms Group.

In short, while Intel’s top- and bottom-line numbers look pretty solid … the company appears to be thriving off AMD and Nvidia’s scraps right now. Sure, that’s apparently a lucrative business all on its own, but it’s not the leadership position Intel used to enjoy.

And that, Great Ones, is a real investing sentiment killer for INTC stock.

That said … Wired magazine is saying this small company “could be the [next] Intel…”

The next Intel? I just got over this one!

…and it’s easy to see why. They’re both microchip companies. They’re both from Silicon Valley. The only difference is this new company is at the start of its journey — with most of its profit potential still to be realized…

Click here to discover the details of the stock Wired says “could be the [next] Intel…”

And now for something completely different! Here’s your Friday Four Play:

No. 1: Riders On The Tweet Storm

Into this house we’re born. Into social media we’re thrown. Like a dog without a bone or a politician without a loan. Riders on the tweet storm.

I don’t need a brain that’s squirming like a toad to realize that Twitter (NYSE: TWTR) is killing it right now. And the company proved it with this morning’s quarterly earnings report.

Revenue skyrocketed 74% to $1.06 billion, while earnings rose to $0.20 per share. Both figures topped Wall Street’s targets of $1.05 billion and $0.07 per share, respectively.

Furthermore, Twitter’s ad revenue soared 87% year over year.

Remember that pandemic-induced ad drought? Yeah. Twitter solved that problem in spades.

And there’s sure to be more growth to come as Twitter rolls out its subscription options to a broader audience.

“As we enter the second half of 2021, we are shipping more, learning faster and hiring remarkable talent,” said Twitter CEO Jack Dorsey.

Those weren’t just pretty words from Dorsey, either. Twitter upped its third-quarter revenue outlook to a range of $1.22 billion to $1.3 billion, handily topping the consensus estimate for revenue of $1.17 billion.

I know social media stocks leave a bad taste in most Great Ones’ mouths, but if you did decide to invest in one social media company, Twitter should probably be it for its growth prospects alone.

TWTR rose nearly 2% following this morning’s report.

No. 2: Oh … Snap?

Now, I just got through telling you that Twitter was the way to go … and yet, Snap (NYSE: SNAP) shares soared 22% after its quarterly report. I’ll tell you why in just a second…

First, let’s look at Snap’s report. It was a doozy.

Revenue blasted off 116% to arrive at $982 million — well above Snap’s own guidance and Wall Street’s target. Earnings came in at a surprise profit of $0.10 per share, versus Wall Street’s projection for a loss of a penny per share.

Snap also reported a rise in daily active users, up 23% to 293 million. And it boosted third-quarter revenue guidance to land between $1.07 billion and $1.08 billion, topping analysts’ expectations for $1.01 billion.

“Our second-quarter results reflect the broad-based strength of our business, as we grew both revenue and daily active users at the highest rates we have achieved in the past four years,” said Snap CEO Evan Spiegel.

So, why would I recommend TWTR over SNAP? I mean, Snap’s growth rate appears leaps and bounds over Twitter’s.

First, when you start at the bottom of the social media food chain like Snap, you really have nowhere to go but up. Second, Snap’s core audience is notoriously stingy when it comes to paying up. Advertising revenue is coming around, so maybe Snap has finally figured something out.

But we’ve seen this scenario before with Snap. It has moments of greatness followed by needless expenditures, like augmented reality glasses. I’ll need to see more stability and growth for Snap before I jump on that bandwagon.

Plus, maybe it’s because I’m old, but I still to this day don’t understand Snapchat as a social media platform. Any of you Millennial or social media savvy Gen X-ers out there wanna explain it to me? Or any daring Boomers wanna take a stab at Snap? Not literally, of course, though I know you’re feelin’ it.

Drop me a line at GreatStuffToday@BanyanHill.com with your two cents on Snap or social media in general. (Yes, I know what door I’ve opened. Come right on in!)

No. 3: Great Bolts Of Fire

You know that it would be untrue … you know that I would be a liar if I was to say to you … jeez, girl, your Chevy Bolt’s on fire. You gonna take care of that?!

General Motors (NYSE: GM) issued yet another recall for Chevy Bolts made between 2017 and 2019. The first “rare manufacturing defect” was software-based, GM says, while the new “rare manufacturing defect” is in the battery modules.

Rare. They keep using that word. I don’t think it means what they think it means.

While GM is offering to replace the affected battery modules for free, the repeated recalls can’t be good for GM’s coffers.

In the meantime, here’s what the automaker wants Bolt owners to do so their cars don’t, you know, become a funeral pyre:

- Avoid depleting the battery below 70 miles of remaining range.

- Set the vehicles to a 90% state of charge limitation.

- Don’t charge the cars overnight unattended.

- Park outside.

The recalls themselves are probably pretty important … if you happen to have one of the affected Bolts. I certainly don’t want any of you affected by any Bolt’s a-burnin’. I mean, how can you sleep when your Bolts are burning?

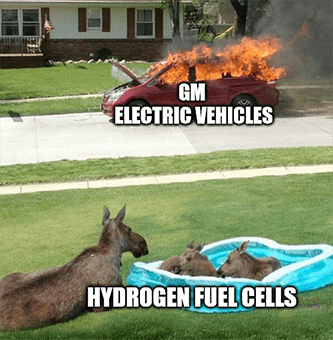

But recalls aren’t the meat of the matter for GM investors. It’s the frequency of them. It’s the fact that GM already rolled out what it thought was a “permanent solution” earlier this year. What do these constant battery breakdowns say about GM’s electric vehicle (EV) tech overall?

The company’s rushing batteries out the door and having reliability problems with them? Funny how that works. These batteries are critical for GM to compete in the new EV landscape, and that’s what should worry GM investors most.

If only the company hadn’t waited so long to get in on the EV market, maybe it would have these problems solved by now. But it’s not just GM…

It seems like every EV maker is having battery issues lately … that is, save for EV makers like Hyzon that work with hydrogen. If you’ve followed Great Stuff for any length of time, you know what’s coming next…

He’s gonna say it — by golly, here we go again!

Hydrogen power would fix this. Batteries are a brick wall that the EV industry keeps banging its head against, while the open door to hydrogen power is literally. Right. There. C’mon, GM, get it together.

GM shares were only down about 1% today, on the bright side. On the brighter side, there’s better battery tech out there than whatever nonsense GM is putting out…

Don’t believe me? Just click here for more.

No. 4: Truly, Madly, Deeply

I wouldn’t drink with you on a mountain. I wouldn’t drink with you in the sea.

I wanna lay like this forever … ‘till the dang seltzer craze is over, at least. And oh, how the turn tables.

Last quarter’s earnings scraped the bottom of the barrel for Boston Beer (NYSE: SAM), maker of Sam Adams, Angry Orchard, Twisted Tea and, regrettably, Truly Hard Seltzer.

Y’all liked those double-beat-and-raise reports?

How about a double miss with lowered guidance? Yikes…

Boston Beer’s earnings came in at $4.75 per share — a long ways away from estimates of $6.69 per share.

Revenue wasn’t as bad but still fell short: $603 million versus expectations for $658 million. The company also lowered earnings from a range of $22 to $26 per share down to between $18 and $22 per share.

Usually, I’d expect management to come up with some corporate fluffy-duffy B.S. to explain why literally every measure missed expectations, but this time, Boston Beer was surprisingly upfront. Its problem is seltzer. I knew it!

According to CEO Dave Burwick, the company “overestimated the growth of the hard seltzer category in the second quarter and the demand for Truly.” I, for one, am enthralled by the death of seltzer, though I’m also told that my ire for the craze usually devolves into “rah, rah, get a real drink” nonsense, so…

Turns out that Boston Beer ramped up seltzer production to meet demand that just wasn’t there, leaving supply chains all askew and overloaded with Truly awful inventory backlogs. It seems like the world’s incessant fascination for carbonated low-alcohol-content water has fizzled out … for now, at least.

Boston Beer’s dream, its wish, its fantasy of hard seltzer supremacy is no more. It needs a new beginning — a reason for living — that doesn’t involve falling head over heels for every passing drinking craze. And SAM investors know it: Boston Beer stock plummeted faster than Truly carbonation on a hot day, falling more than 25% today on the news.

(By the way, something about using Savage Garden lyrics always brings in strange, fangirling emails, so … keep it tame this time, I guess? I’m blushing over here, y’all.)

Something, Something … The Weekend!

By Jove, this is the moment you’ve all been waiting for — the weekend, at last! The end of my yapping and, with any luck, the start of your yapping. If you’re looking for something to do this weekend, why not drop us a line?

How’d this week treat you, Great Ones? Everything all gravy out there? Portfolio’s looking sharp?

It’s been a hot minute since we last caught up, so stop by the inbox this weekend and give me an earful — market-related or otherwise.

GreatStuffToday@BanyanHill.com is where you can reach us best. In the meantime, here’s where you can find our other junk — erm, I mean where check out some more Greatness:

- Get Stuff: Subscribe to Great Stuff right here!

- Our Socials: Facebook, Twitter and Instagram.

- Where We Live: GreatStuffToday.com.

- Our Inbox: GreatStuffToday@BanyanHill.com.

Until next time, stay Great!

Joseph Hargett

Editor, Great Stuff