“Death and taxes.”

Those are the only two certainties in life, according to Benjamin Franklin.

And his words have never rang truer than last year as the Federal Government fleeced Americans for a grand sum of $4.4 trillion.

And it looks like they’re coming after even more in 2024. Each bracket is inching up about 5.7% compared to 2023.

It’s getting a bit crazy.

Our tax code now exceeds 1 million words…

And it is extremely complex … changing 4,680 times over the last decade. That’s more than once per day.

However, while our tax system may be complex, and paying taxes may be inevitable, you have the right to pay as little as legally possible.

This is why today, I’m going to show you one of my favorite tax “loopholes.”

It reveals how you can earn $47,025 in tax-free income per year.

$94,054 if you’re married.

It’s 100% legal.

And it’s drop-dead simple to use.

Yet, few people know about it (or fail to fully understand how to take full advantage of it).

And today I want to give it to you for free. All I ask is that you share your favorite tax loophole with me, and the Banyan community, by leaving a comment at the end of this article. More on how to do that in a moment.

So, let’s get started.

Step 1: A 99% Pay Increase

As you likely know, the IRS withholds up to 37% of your wages (before the state taxes, sales tax, real estate tax, capital gains tax and other taxes. Yuck!).

You also likely know that the highest dividend tax rate is only 20% … assuming you hold on to your stock for more than 60 days making it “qualified.”

Again, most of you know this…

But what you may not know, is that the dividend tax is only 15% if your total income is under $583,751 (filing jointly).

The 15% dividend tax alone is a huge windfall and a reason to make dividend investing an essential part of your portfolio strategy.

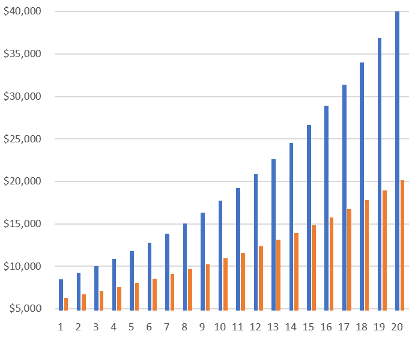

Let me give you an example using assumptions…

- You have $100,000 to invest in two different assets.

- Both assets pay a 10% yield.

- You are reinvesting your income over 20 years.

- You are happily married to the love of your life!

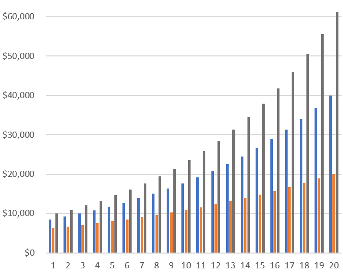

This is how your income stacks up over time.

The orange is the asset that pays an ordinary income … perhaps it is a bond, real estate income or an MLP.

Your AFTER-TAX annual income starts at $6,300 and slowly builds to $20,113.

Not bad.

But not great.

The blue is the other asset. It pays a dividend income.

Your AFTER-TAX annual income starts at $8,000 and slowly builds to $40,048.

That’s 99% MORE than you would get with your first option.

Again, this is likely what you already know.

But here’s what you may now know…

You may be able to boost your income to $61,159 by paying zero taxes on your dividend income.

Step 2: The 204% Pay Increase

Let me repeat that.

Let me repeat that.

You may be able to boost your income to $61,159 (a 204% pay increase) by paying zero taxes on your dividend income.

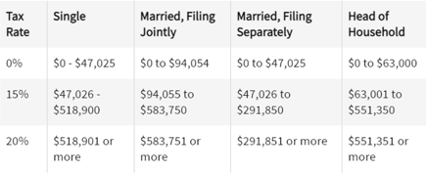

Just look at this tax schedule from the IRS:

You pay zero taxes on your dividend up to $94,054.

And only 15% on the dividend earned between that amount at $583,750!

This is an insane benefit.

Using the same assumptions as before, this zero-tax strategy would allow you to boost your real income to $61,159 (The grey bar in the chart below).

What would you rather have?

- An income of $20,113.

- An income of $40,048.

- An income of $61,159.

I think we would all agree that $61,159 in tax-free income sounds mighty nice!

Please Note: To make this work, you also have to take your ordinary income into account. For example, if you make $100,000 a year and then get $50,000 in dividend income, you will need to pay 15% on your dividend income.

This is why if you are in retirement now, this is a great strategy. Odds are, your ordinary income is low. If you shift your investments to strong dividend-paying companies, you can boost your REAL return.

But if you are NOT in retirement, you can start planning now to ensure your real income is low during retirement. Speak to your financial advisor for strategies to do this.

The big takeaway: Once you’re in retirement, owning dividend-paying stocks and compounding that income is the best game in town.

You have to pay taxes on Social Security, Bond Income, 401(k) withdrawals and selling stocks for big gains.

But NOT dividends.

So, you may want to consider shifting some of your assets to stocks with big dividends.

I love this strategy. I mentioned a few weeks ago that I own a stock that is legally required to pay me a 19.59% dividend … perpetually! You can read that article by clicking here.

But our team here at Banyan Hill also has plenty of big dividend payouts in their portfolios.

I know I am a bit like a chef bragging about his own cooking, but our team has found some real gems.

- Charles Mizrahi has positions yielding 1%, 5% and 3.8%.

- Adam O’Dell has positions yielding a whopping 1%, 7.4% and 4.1%.

If you want full access to stocks like these, consider signing up for their investment services.

Now in a moment, I’m going to ask you for YOUR favorite tax loophole, and you will be able to share it with the Banyan community.

But first, I have two additional tax loopholes I think you will love.

Bonus Loophole 1: Use an IRA for … Aggressive Trading Strategies

Oftentimes, people put their most conservative investments in an IRA … mutual funds or similar.

Not me.

I often use my IRA for aggressive trading strategies whether that be stocks or options.

Take for example.

Twenty years of data proves that it has the power to beat the market 300-to-1.

But, the average hold time of a position in that portfolio is only a few months. So if I’m cashing out of a 100% gain for $10,000 … my real return is only about $6,500.

Over time, that eats away at my gains.

But in an IRA, I don’t have to pay taxes until I withdraw the money. It grows tax-free, without the capital gains that can take as much as 37%. (If in a Roth, I never have to pay taxes on it).

Meanwhile, I use my regular account for strong dividend stocks…

This month alone, U.S. Bancorp will pay me $421.34.

Merck will pay me $384.17.

And PepsiCo will pay me $355.45.

Remember … this dividend income is NOT subject to the 37% tax rate. At most, one pays 20%.

This strategy of using an IRA for aggressive investing goes against conventional wisdom. But the math suggests it may be the best way to grow your wealth and minimize taxes.

Bonus Loophole 2: Why I Overfunded a 529 Plan

This “loophole” is a bit more straightforward.

Here’s how it works…

You can put as much money as you like into a 529 plan and when you take the money out, it is all tax-free as long as it is used for educational purposes.

To be clear…

Unlike a 401(k), IRA, Roth IRA … there are far higher limits to how much you can put into these plans. It varies by state, but a 529 can be funded up to $550,000.

Once in, you generally invest in mutual funds and exchange-traded funds (I couldn’t find a plan that lets you invest in individual stocks).

I use Vanguard for my account. It has plenty of low-cost funds.

And when you take the money out, it is tax-free, as long as you use it for educational purposes.

That can be…

- Tuition and fees.

- Elementary and secondary schooling (public or private).

- Pay student loan debt.

- Off-campus housing.

- Food and meal plans.

- Books and supplies.

- Computers.

- Software.

- Internet service.

- Business purposes if purchased while in college.

These can add up to hundreds of thousands of dollars.

Here’s what you may not know…

You can open a 529 plan for pretty much … anyone.

A kid.

A grandkid.

Or just … a friend.

And, if you choose to change who you designate it for, you can do so.

Take me, for example.

I have four young kids.

And I’ve been squirreling money away in a 529 plan since they were born.

And now, after several years of doing this, I no longer have to put money into the plan. I have more than enough to pay for any future college expenses.

In fact, I overfunded it.

But, it wasn’t an accident.

That’s because, if I choose, I can reallocate my 529 plans to my grandkids one day, or great-grandkids, or just someone I wish to bless.

And all the money that comes out will be tax-free.

Imagine your grandkids, great grandkids leaving college, debt-free.

What a gift!

That’s creating wealth “for a thousand generations.”

I hope these tax strategies help you keep more of your hard-earned money.

Of course, everyone’s situation is different, and you should run anything tax-related by an accountant.

So…

What About You?

I can geek out about tax strategies.

I really can.

Most of my insight is investment-related … IRA, Roth IRAs, 401(k)s, municipal bonds and the like. But, you may have a few that you want to share with your fellow Banyan Hill readers.

If so, I’d love to hear from you.

Thanks, in advance.

Aaron James

CEO, Banyan Hill Publishing and Money & Markets

Great insight!

Gifting from an IRA to a registered charitable organization is tax-free and reduces the net taxable RMD.

Most people probably already know this, but it came as a pleasant surprise to me. We own two properties that we rent. Not only are we entitled to deduct repairs and supplies but also every year we get a major depreciation deduction on each of them. That’s made our STR (short-term rental) especially profitable for us in the long run.

Rental properties can be a bit of work, but with cash flow, price appreciation, and the tax benefits you mentioned, they do a nice job of building wealth!

Everyday I look for ways to make my money work for me and reading many different strategies I’ve found different ways to capitalize however I can’t find too many ways to make it tax-free. I’ve been investing for quite some time with minimal gains and your info helps guide me as well as focus on different key performance indexes. Thank you for the info.

I have been using $94054 since retiring with regards to withdrawals from retirement accounts. When planning the amount is actually $123254 for joint filing with the standard deduction (2×14600).

Wow, that’s awesome… definitely something to think about when planning for retirement income!

I send my church pledge from the brokerage IRA account which meets my MRD requirement and takes it out of take it out of taxable gross income. It must go directly from my account to the church.

I love Real Estate. You get paid in so many ways. 1. the Tenants pay your bills, pay down your mortgage and increase your equity. 2. Tenants give you monthly cash flow. 3. Tax deductions and property depreciation are galore. As my children grew up and move out of the house deductions decreased, I replaced their deductions with real estate deductions and keep my taxable income low. 4. Leveraged appreciation on property value. Real Estate goes up over the long term on your 10-25% investment. Lastly real estate is a hedge on inflation.

Thank you for putting this info in clear understandable language.