Over the past few months, there has been an influx of doom-and-gloom articles claiming home prices are in a bubble.

Frankly, I don’t think the claims could be further from reality.

That’s because measuring value is all about perspective.

When compared to historical home prices, current home prices may seem expensive.

In fact, the Shiller Home Price Index is 38% higher than it was at the height of the 2006 housing bubble.

But if you consider factors like rising rent prices, wage inflation and a rapidly expanding money supply, the housing market has been modest in recent years.

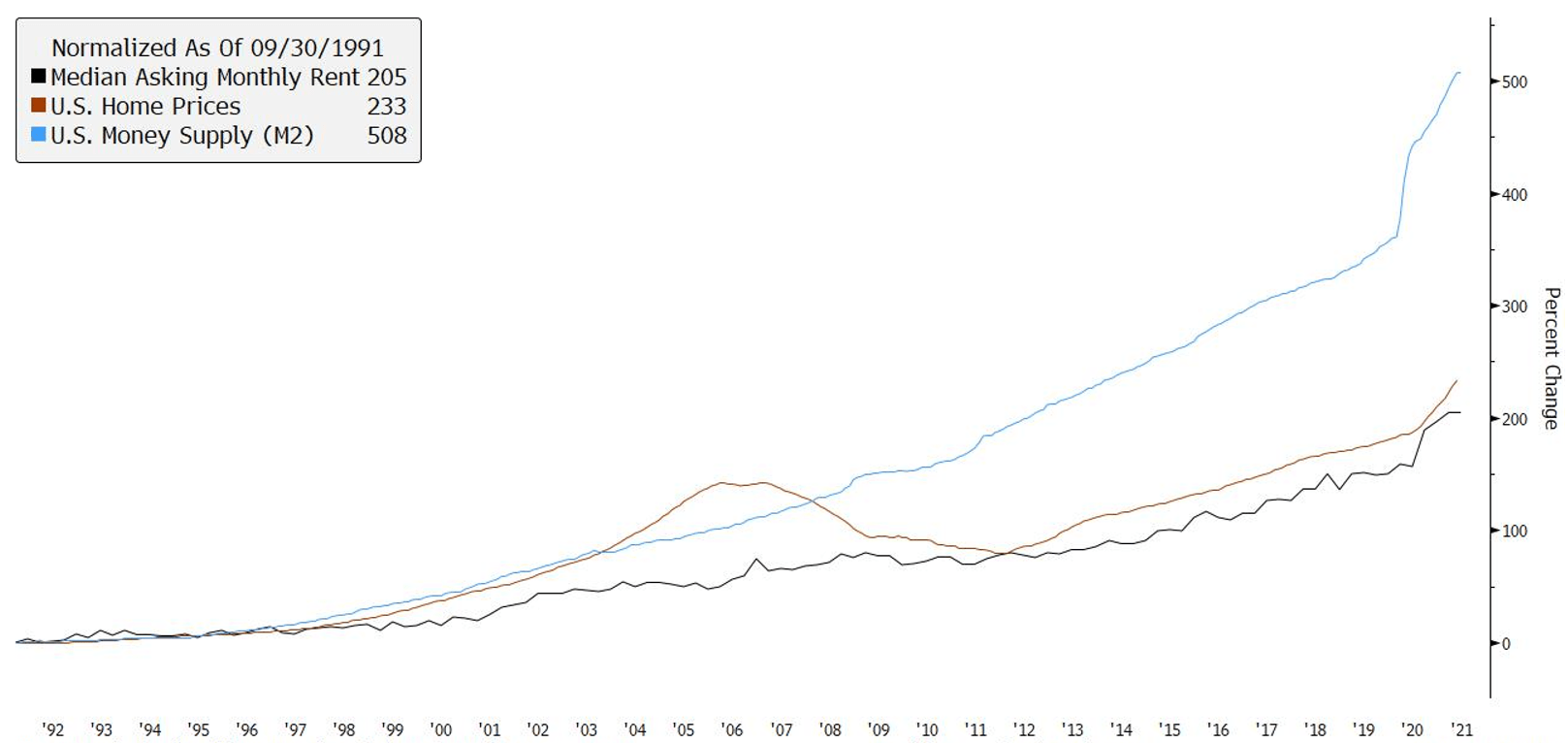

In the chart below, the blue line shows the U.S. money supply.

Below it, the red line shows U.S. home prices, while the black line shows the median rent cost.

(Source: Bloomberg.)

The 22% rise in U.S. home prices over the past two years has been met with an identical rise in rent costs. This means the cost trade-off between renting and buying hasn’t changed.

Prospective homebuyers will have to pay up for living costs regardless of whether they buy or rent.

So, the option to purchase a home and build equity still looks attractive.

Home Sales Are Still Strong

As you can see in the chart, in the 2006 housing bubble soaring home prices weren’t met with a similar rise in rent.

In that scenario, it was less justifiable to buy a home versus renting since the cost of ownership was rising much faster.

And consider this…

The rise in home and rent prices pales compared to the 39% increase in cash on the sidelines in the U.S.

This means Americans are sitting on more cash than ever before. And that cash has to go somewhere.

Based on current trends, it looks like it’s being put toward new homes.

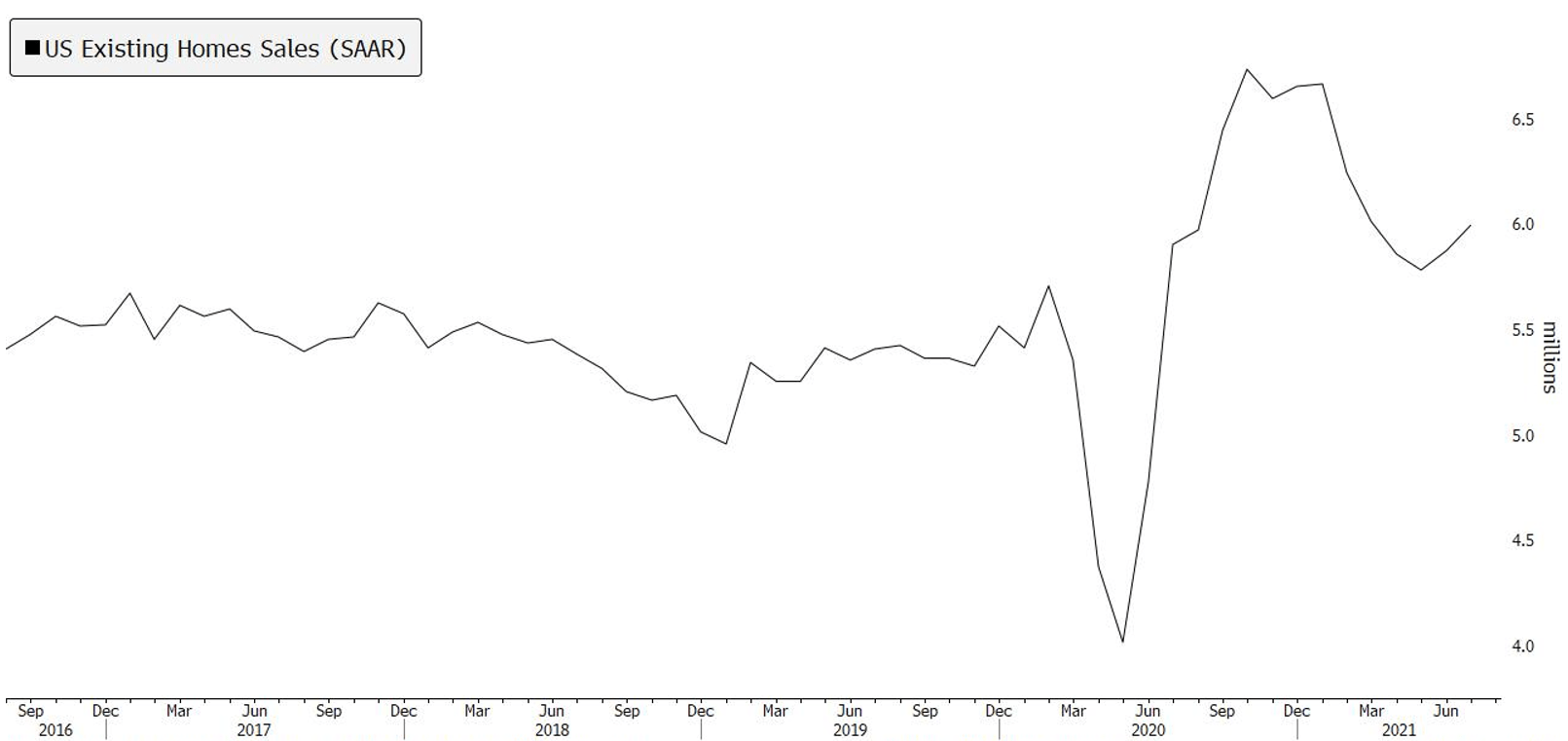

Even after home prices’ recent move higher and the slowdown in the number of houses sold, U.S. home sales are still strong…

U.S. existing home sales were 9% above their five-year average in July.

(Source: Bloomberg.)

The housing market will continue booming until mortgage rates see a material increase.

With lower interest rates, monthly mortgage payments are lower. This can offset higher home prices more than some realize.

For example, a $500,000 mortgage with a 3% interest rate has a monthly payment of $2,108.

But a $400,000 mortgage with a 5% interest rate has a monthly payment of $2,147.

As you can see, the more expensive house actually requires a lower payment each month.

And for most consumers, this is what matters. It’s why lenders usually ask: “What do you want your monthly payment to be?”

Interest Rates Will Remain Low

With the average 30-year mortgage rate still near all-time lows at 3%, getting financing for new homes is still cheap.

Freddie Mac researchers are forecasting rates will rise to 3.8% by the end of 2022. But even then, mortgage rates won’t have reached pre-COVID levels.

A material rise in interest rates will likely take years to play out, so U.S. home prices should keep climbing.

Regards,

Research Analyst, Strategic Fortunes