Most market participants knew that the Federal Reserve would increase interest rates by 0.25%.

What they don’t know is if all this is leading to a recession.

And if it does, how do you even plan for it?

In today’s video, I break down the Fed’s press release to answer your many questions and more…

Transcript

Hello, everyone, this is Ted Bauman here, editor of Big Picture, Big Profits, and of The Bauman Letter. Before I start, know this is not a T-shirt that says “BRA-MASTER.” It says “BRAAIMASTER,” I wore it two weeks ago and some wag wanted to know what it means, but a South African popped in and said, yes, Ted must be a good BRAAIMASTER, which means barbecuer in South African lingo. And indeed I am.

Today we want to talk about the Fed’s meeting this week. In one respect, it was inconsequential in that the Fed didn’t really do anything that people didn’t already expect. We knew that they were going to raise interest rates. The big question was whether they were going to raise them by 0.25% or 0.5%. In the event, they opted 4.25%, which didn’t really surprise anyone. And as a result, I think, the market has taken it pretty well.

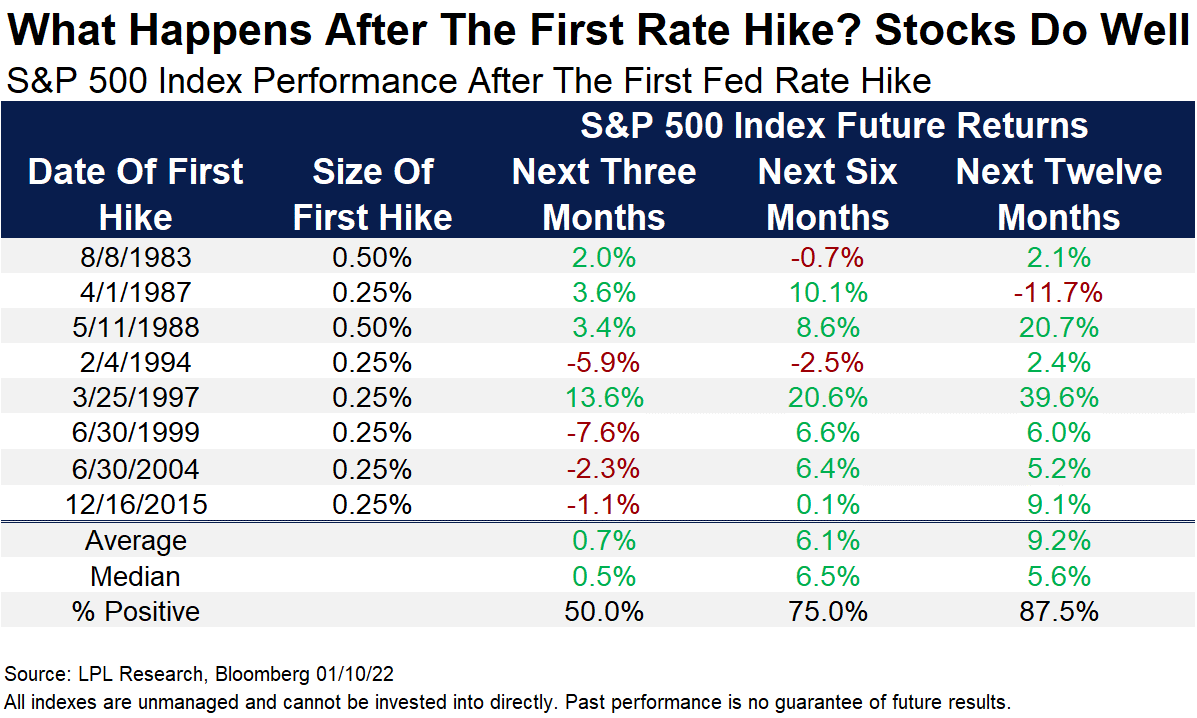

Well, what happens after the Fed hikes rates? Now here’s a chart that comes from LPL Research and it’s a good example of what not to do in the current environment.

And what this chart purports to show is that here’s a bunch of Fed hikes, the size of the hikes. And then what happened to the stock market over the next three months, six months and 12 months, the average over three months is about 0.7% up for the S&P, the next six months 6%, of the next 12 months about 9%.

My advice would be to forget about all of that, because we’re not in a circumstance like that at all. None of those dates from 1983 to 2015 are anything like the current scenario that we have. Right now. The scenario is this, we have two cross currents in the stock market that are really headed in different directions.

On the one hand, there are fears of a recession. I’m going to talk about why we might be concerned about a recession in a moment, but that would tend to be bad for the stock market as a whole. On the other hand, some investors believe that if there is a recession, the Fed might slow down its planned interest rate increases, and that would be good for long-duration technology, growth stocks, the stocks that have really struggled during this inflationary period for the last year or so.

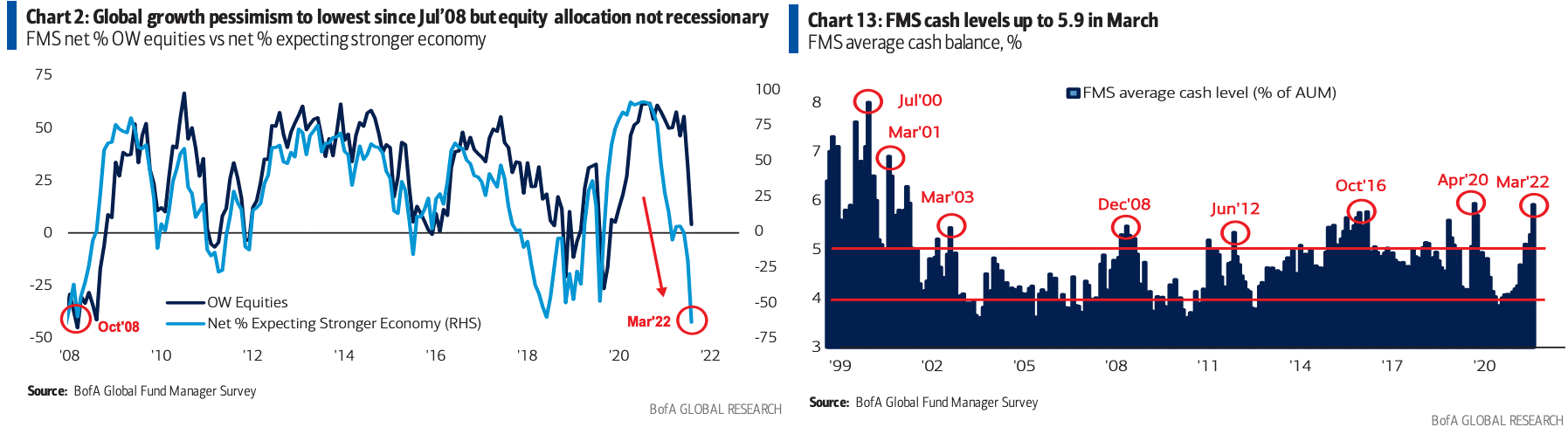

Well, what does the market think? Here’s a chart from the Bank of America, Global Fund Manager survey.

And it shows the concerns that the investors have fund managers in February light blue and March in dark blue. Now the obvious thing here is that hawkish central banks have fallen way down on the concern level and the Russia-Ukraine conflict has jumped up and so has fears of global recession.

Interestingly, fears of inflation have actually receded quite a bit. Fears of a pop in asset bubbles have fallen and partly that’s because they’ve already started the pop, I think it’s fair to say. What’s interesting, COVID falls under other. COVID has now been baked into everybody’s forward thinking. So really the big issues right now from the perspective of the market are the war in Southeastern Europe, a global recession and inflation. Now, what has the market done? What have fund managers done in anticipation of these concerns?

Well, here’s a chart that shows average cash levels as a percentage of assets under management.

And right now, in March, 22, we are at a level that is pretty much the same as it was in April, 2020. That means that the big guys are taking their money out of the market and keeping it on the sidelines. That’s not a bullish factor. That’s actually quite a bearish factor. That tells us that right now, the big boys, the people who invest for a living are taking their money out the market and keeping it on the sidelines.

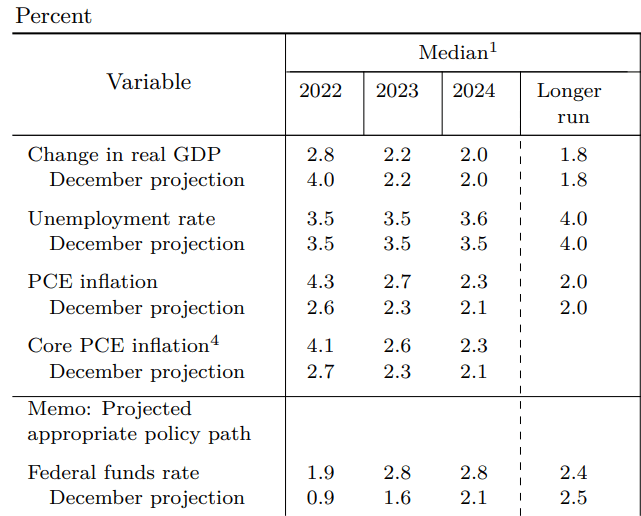

Well, what did the Fed actually say? And besides the announcement of a 0.25% increase in the policy rate and an increase in the target rate to 2.25%, the Fed also gave its indications of what it thinks the economy’s going to do. And here’s the chart from the Fed’s press release.

The important column is the 2022 column. And what I want to draw your attention to here is that, whereas in December last year, the Fed thought that the economy would grow by 4% in 2022, it’s now down to under 3%, 2.8%. The unemployment rate, the Fed sees it remaining relatively stable. Inflation, the projection in December was 2.6%, now it’s 4.3, that’s primary consumer inflation. Core inflation, which strips out energy and food is expected to be about 4.1%. Now, the Federal funds rate by the end of this year… In December, the Fed thought it would be a little under 1%, now it’s aiming for a little under 2%.

Now, what that means is that the Fed is acknowledging that the economy is going to grow slower this year than what they thought in December. Inflation is going to be higher than they thought. And there’s two reasons for that. One is of course, that the war in the Ukraine is a massive headwind to the global economy. But the other factor is that inflation tends to destroy demand because as prices rise, people buy less of what’s expensive. Now you add into that interest rate hikes, that could be a recipe for some very interesting times, indeed, which I’ll talk about in a moment.

So there are four things we want to talk about. What did the Fed say about these four things? First thing is how many interest rates this year? Last year, the Fed thought that they would increase rates by 0.25%, three times this year. This year, the Fed is talking about a total of eight quarter point hikes, this year alone. Okay. Now that would mean… Sorry, seven plus one in early 2023. Now that would mean that the Fed would end up with a policy rate of 1.9% as I mentioned earlier.

Now that is a fairly significant increase over where we are. It’s actually a huge increase because right now effectively, or until yesterday, the policy rate was zero. So that means that you can expect if the Fed pursues this, that’s a pretty hawkish headwind. Now interest rates have been a lot higher than that in the past, so this isn’t historically high, but relative to where we’ve just come from, it is quite high. Particularly since we could be heading into recessionary questions or conditions.

The second issue that we want to interrogate the Fed on is what do they think about the Russia-Ukraine war? Well, Powell said that the war raises risks for the US and global economy and people thought, well, if he played it down, that would be a hawkish sign saying that, “Well, we’re not worried about the war, that means we can continue raising our rates.”

In his post-meeting press conference, Powell said that the implications were simply highly uncertain. He left himself some maneuvering room. He said, “We really can’t tell what it’s going to do.” Now, the reason why this is important is because if he had said, “Don’t worry about it, we can deal with it.” That would’ve been a signal for people to pile back into long-duration stocks, growth stocks, stocks that pay off in the future, because they would assume that the Fed isn’t going to raise as quickly as they would’ve otherwise.

By saying it’s uncertain, he keeps the uncertainty in the market going. That means that we can expect to see a great deal of choppiness in duration stocks, in the technology stocks. We’ve seen a pretty huge jump in some of these stocks. Yesterday during the press conference, as it was happening, some of the stocks in my Bauman letter and profit switch portfolio jumped by double digits, some up to 25% on a single day.

And those tended be stocks that have really taken a beating in the last year or so. That tells me that people were thinking that the Fed was actually being more dovish than expected. Today, although there’s still some rises, I think it’s becoming a lot less certain and that’s exactly what Powell wanted to indicate. He wants to keep some maneuvering room for themselves.

So the whole idea that the war would lead to the Fed to be more dovish and therefore open the flood gates to investment in growth and duration stocks, I think that’s off the table for now. We simply are going to continue the way we’ve been, which is not knowing what’s going to happen and where day to day flows are driven by market structure, particularly the options market and the volatility at risk management systems a lot of big hedge funds use.

What’s the Fed’s message about inflation? Well, the Fed clearly expects inflation to slow down, but not as much as it did before. They’re still expecting basically a December inflation rate just under 3%, which is higher or lower than they thought, or sorry, 4%, which is higher than they thought it would be in December, but which is still a lot lower than it is right now.

I mean, producer price inflation actually hit close to 10% last month, which is quite shocking. But clearly the Fed is thinking that although inflation will remain higher because of the Russia-Ukraine war, which is a supply side issue, it is going to decline, but not by as much as the Fed wanted.

Now, one of the things that the Fed said, which is quite significant is that the labor market is extremely tight and wages were on an upswing. Now, given that wage price spirals, which is basically when workers demand more money because they expect higher costs and employers experience higher costs from wages and therefore raise their prices, which leads workers to ask for more money, again, the 1970s scenario, that’s the bête noire of all inflation Hawks. That’s what they’re scared of. The people like Larry Summers and others who are very inflation hawkish, that’s what they’re worried about.

So, by mentioning that Fed or Fed Chairman Powell basically put himself on the side of hawkish, which means that although he’s been very vocal about wanting to support the labor market and to see wages increase, he’s starting to talk about moving in the opposite direction. It’s also notable that Powell said in questioning by Congress later that day, that Paul Volcker, who was the chairperson of the Fed during its huge interest rate hikes in the 1970s, at one point up to over 20% policy race, which caused deep recessions, Powell said that Volcker was one of the greatest economic public servants of the Europe. Which tells us that if push comes to shove, Fed or Powell is prepared to see a recession happen even if it means hardship, which of course Joe Biden, the Democrats won’t want to see, but that is what Wall Street and pretty much the entire economic establishment wants to see.

What about shrinking the balance sheet? Well, the Fed’s balance sheet increased to almost $9 trillion during the pandemic. Shrinking it is absolutely essential. There’s no point in the Fed continuing to ease money conditions at the same time that it’s raising rates. Now, it wasn’t clear whether the Fed was going to announce an early cessation of bond purchases, but what the Fed or what Powell did say was that they were going to stop reinvesting proceeds from bond purchases and that they would consider starting to sell in their next couple of meetings.

You can interpret that as dovish, but traditionally the Fed has always used interest rate increases as a signal that it’s about to stop quantitative easing. So there’s a lag between the two. So this is not really unusual. Some people had called for the Fed to announce an instant cessation of bond purchases, but that’s not the way the Fed operates, that would’ve been too much of a shock that would’ve caused eruptions in the market. And clearly the Fed still has one eye on the market, even though arguably it’s not part of its mandate, the stock market and financial markets. The mandate of course being inflation and unemployment.

Now, what does this mean if the Fed is raising rates and if we are looking at potential recessionary conditions? Well, it’s hard for most people to remember, but one of the Fed’s most important tools is the ability to cut rates in recession. Normally in recessionary conditions, the Fed will cut rates by an average of about 5%. If you look back over the last half century or so, the average series of rate cuts to fight a recession is about 5%.

Now, obviously the Fed can’t do that. The Fed came into the COVID crisis with a policy funds rate of 1.75%, which it then lowered to zero. Because of that, the only way that the Fed could prop up the financial side of the economy was to use its balance sheet, which is why it doubled it from about $4.5 trillion to $9 trillion, just during the recession.

The main result of this, as we all know was one of the biggest asset bubbles we’ve ever seen, not just in stocks, but in cryptocurrencies, all kinds of things, art, you name it. If it was housing, if it was something that was sensitive to liquidity in the market, prices went up. Had little to no real effect on the real economy, which was stimulated primary really by Federal relief payments.

Nevertheless, the Fed does have to be seen to be doing something, which is one reason why it’s raising rates, even though arguably inflation is driven mainly by supply side issues. At least the nonwage inflation, inflation driven by energy, by food, by transport and logistical problems, even inflation driven by supply problems in China caused by a resurgence of COVID. All of these are arguably the main drivers of inflation. The only wage inflation or inflation that you can say is based on domestic stimulus payments is probably wages and things like that.

Now, the problem is that the combination of higher input prices and especially of energy in food means that the Fed would need to basically raise rates in order to try to cut back this kind of stuff. Now, the Fed wants to raise rates in order to hit inflation, but it also wants to get back that maneuvering room.

Remember I said earlier that the Fed wants to be able to raise or cut rates about 5% during a recession. Well, obviously that means it needs to get its interest rates up to a lot higher than a two point or 1.9%, which is where it expects to be at the end of the year. Now, if the economy does slow down, you’ve got higher input prices like energy and food, plus higher interest rates. That’ll cause what we call demand destruction, which is kind of a cynical way of saying that things will get too expensive for people to afford and they will stop buying as much of them. And if they stop buying them like energy in food, they’ll cut back their purchases of something else. That in turn leads to recession.

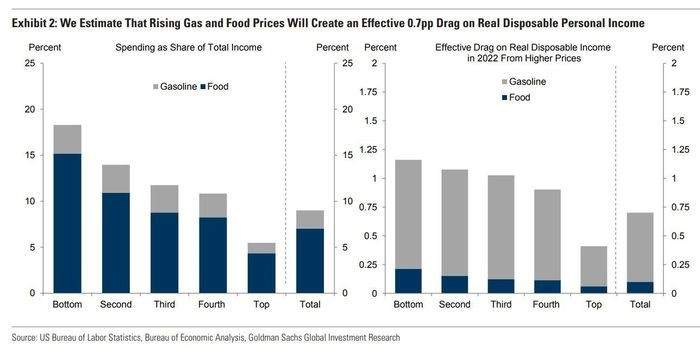

So, you have a scenario where the Fed is already looking at recessionary conditions that could be raising rates into recessionary conditions. Now it’s useful to note that technically speaking, we’re already in a recession when it comes to real wages, which is the rate of increase of wages compared to inflation. Real average, weekly earnings for American workers have been negative for five months in a row. 90% of the time when real incomes fall, so does real spending after a lag of one or two months. Now, considering that 70% of US GDP is driven by consumer expenditure, that means that we could see a recession as soon as this summer. Now here’s a chart that just shows what could happen from the perspective of just gasoline and food prices.

The left hand side of the chart shows the spending as a percentage of total income for five different quartiles or Quintiles of the population. For people in the bottom and second Quintiles, gasoline and especially food are huge elements of their expenditure. And so if the prices of those things rise, they’ll have to cut somewhere. On the right-hand side of the chart you can see the effective drag on disposable real income in 2022 projected from that rise in prices. Overall, you’re looking at a potential, a drag of 0.75% overall, primarily from energy prices, but also for food hitting harder as you get down the income ladder. So the bottom line here is that even with the best of intentions, we’re likely to see a drag on consumer in, or rather on consumer expenditure, which again is 75% of economic activity in the United States, which means that just because of the supply side problems that we’re having, we could see recessionary conditions add to that inflation.

So what could happen if the Fed raises interest rates into a downturn? Well bad for the stock market, bad for consumer discretionary stocks, bad for discretionary goods and services, things like restaurants and other kinds of services. It’s good for treasury bonds, consumer staples, healthcare and medicine, food, and energy, and other things that people must have.

But the single biggest effect I believe will be on housing. Now, the reason is that housing has a huge multiplier effect on the economy. Housing construction consumes large amounts of inputs in labor, which have to be bought, which is stimulative to the economy and rising home values make people feel wealthier and more likely to spend.

But housing is the most interest rate sensitive segment of the economy. Historically Fed interest rates have translated into recessions via a decline in falling house prices. It’s the housing sector that drives the initial recession. The problem right now is that housing is dramatically overvalued and really is a bubble waiting to pop. Historically, housing prices go up 1% to 2% points above the inflation rate. Right now they’re going up 12% faster. Housing is currently overvalued by 35% relative to its normal relationship to other macroeconomic indicators and by 27% relative to incomes.

House prices relative to residential reds are 25% overvalued compared to their normal levels. The price to income multiple, the price of house versus the incomes people have is about where it was in 2006 and 2007, which is before the subprime crisis. In a normal market, it takes five years of income to buy a single-family American home. A single family home now absorbs eight years of Americans’ income, 50% higher than the 50 year average. So the laws of mean reversions say that we’re going to have a 20% to 30% bear market in residential real estate in the worst scenario.

I’m not saying that’s going to happen, but that’s the dynamite that the Fed is playing with. We’re already seeing it in the housing market, where we are effectively already in a short term bear market for house builder stocks. This is despite the fact that demand for housing is enormous as I’ve spoken about.

Now, what should you do in anticipation of this? First thing, build up a cash reserve, because that will allow you to buy assets when they fall in price. If we do see a recession and we start to see falls in stocks and other assets, it’s a good time to buy them, because we will bounce back eventually. So take profits. If you’re up on something, sell some of it, put that money aside and wait for the market to fall. Limit the economic sensitivity of your portfolio and be defensive.

Consumer staples tend to do a lot better than discretionary, restaurants, for example, tend to under-perform grocery change during a recession. Focus on utilities, consumer staples, again, healthcare, which never goes away. Military budgets will go up. So defense stocks may be somewhere to go. Food costs are going to put a premium on farmland. There are farmland, ETFs and funds that you can buy. Also, agricultural equipment I think is a good place to be, not just in the short term, but in the long term, because we are moving towards automation and that space.

Europe is going to be forced to diversify away from Russian energy. As I’ve been saying for a while, liquid natural gas stocks, both producers and transporters will be good to own. The problem with commodities though, and I’m going to leave you with this, is that although commodity prices are rising, we’re actually seeing the stocks of commodity related companies starting to fall. And the reason for that is because of those fears of recessions. It’s one thing for prices to rise, but because the market is forward looking, it sees the possibility of the very rising commodity prices like energy and food leading to a recession, which would in turn lead to a decline in the prices of companies that handle those kinds of goods.

So be selective, buy commodities that have robust demand profile and that are required regardless like food. So that’s my message from you this week. I think the likelihood that the Fed is going to be tightening into a recession is probably around 50%. Some people are convinced that it’s going to happen, some thinks that the Fed can engineer a soft landing. Right now I would say it’s about 50/50. So prudence dictates, move into cash, start getting defensive.

Ted Bauman signing off. I’ll talk to you again next week.

Kind regards,

Ted Bauman

Editor, The Bauman Letter