As some companies stumble … some are still crushing it.

And Lockheed Martin (NYSE: LMT) is doing just that.

After experiencing a major economic downturn, a global pandemic and massive government stimulus over the past few months, you’d think a company that relies on budget money from governments might have done poorly.

But with a massive backorder of $140 billion worth of deals, short-term things like an economic recession didn’t faze the company.

Instead, it was able to report solid earnings and revenue growth for the second quarter. It beat analyst expectations on both line items. That helped send the stock higher.

After the stock’s latest rally on earnings, the question we all want the answer to is whether this rally is going to fuel even more gains for the stock.

This is a stock that has failed to get back to its pre-COVID-19 price levels. Most companies that are not directly impacted by the virus, such as tech stocks and online companies, have climbed well past their pre-COVID-19 price levels.

Lockheed Martin is still down more than 10% from its peak in February. Even though the company posted great results for the last quarter, analysts are not sending shares back to that level anytime soon.

In my latest Bank It or Tank It YouTube video, I break down everything you need to know about Lockheed Martin.

We take a look at its key fundamentals, sentiment and price chart. I’ll also give you my price target for the stock over the next twelve months to determine if this is a stock you want to bank on … or expect to tank.

Breaking Down Lockheed Martin Stock

Summary:

- Lockheed Martin is one of the top aerospace and defense companies in the world.

- It’s shown that the coronavirus pandemic has had little impact on business.

- Take a look at the fundamentals, sentiment, and the technicals to see if you should “Bank” or “Tank” Lockheed Martin.

This week’s Bank It or Tank It covers aerospace and defense company Lockheed Martin (NYSE: LMT). We’ll take a look at the fundamentals, sentiment and the technicals to figure out of this is a stock that you want to bank on over the next 12 months or tank.

Lockheed Martin shares are trying to turn higher after investors are seeing the feared “blue wave” isn’t taking shape. Without total control by the Democrats, the defense industry doesn’t have to worry about budget cuts for now.

This is a company that relies on government contracts. So, with a lot of government spending, and another potential stimulus for the economy, the path for growth is becoming more clear…

In its latest earnings report, it showed that the pandemic had little impact on business and reported backlog orders are at 150 billion. So Lockheed Martin has a lot of contracts coming up in the years ahead to help keep it afloat, regardless of what’s going on in the short term.

That makes this a company that’s really cruising higher right now, and analysts were loving the stock. They dipped after the earnings report, even though the company beat expectations. It had to do with a softer-than-expected guidance that worried investors.

But the election news could be the piece of the puzzle to kick-start the turnaround for the stock.

We’ll take a look at how the technicals are shaping up. But first, let’s dive into some of Lockheed Martin’s key stats to break down how the fundamentals look.

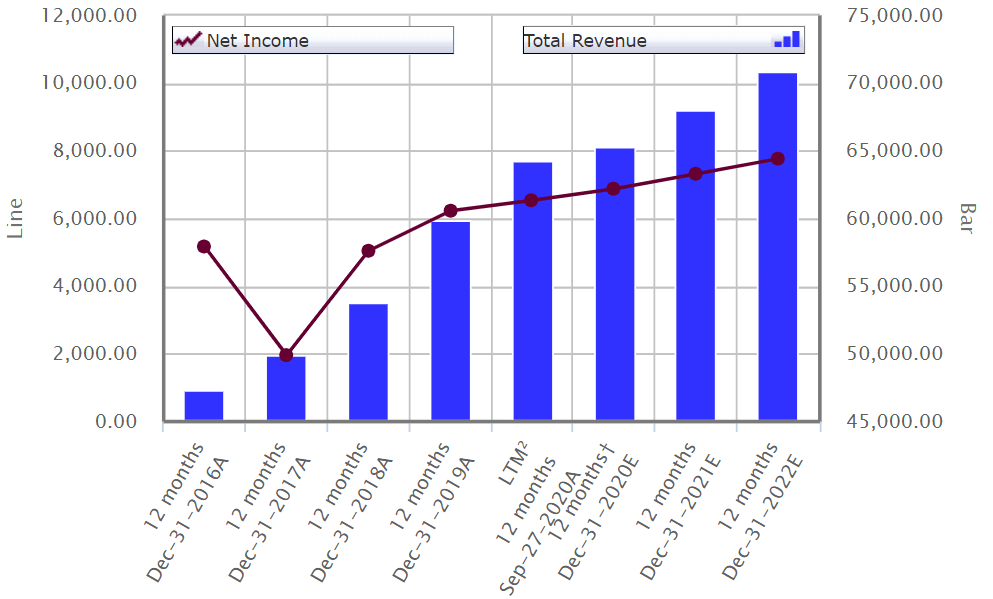

LMT – Key Stats

The two things we like to look at for key stats are net income and total revenue. Total revenue is the blue bars on the chart; net income is the line on the chart.

When we look at net income, it had a dip in 2017, but has steadily climbed since. Revenues have been heading higher since 2016.

There really are no hiccups in terms of the stock’s revenue stream. And even with the pandemic, like I said, Lockheed Martin recently had earnings and is still seeing a strong backlog — a strong demand for its orders.

This is a company that makes the F-35 fighter jets and other military aircrafts, vehicles and missiles. So Lockheed thrives when there’s tension around the globe. And right now, that tension has taken a back seat to everything going on with the global pandemic.

A virus is not a real threat Lockheed Martin would be able to benefit from. So, it’s created this uncertain time for Lockheed Martin.

The election was another big uncertain moment for the stock.

But now that it is out of the way, it seems favorable for the company to continue to see a steady budget to spend on military contracts.

At the end of the day, this is a company that’s still going to see contracts with its backorder staying intact.

Now that we’re moving past the election, we can look long term. And this is a company that’s still going to thrive.

Global conflicts will come back into focus as we overcome the pandemic, and we’ll see strong demand for Lockheed’s products.

Overall, its total revenues and net income look great.

Now, we can take a look at some of Lockheed’s competitors to see how it stacks up…

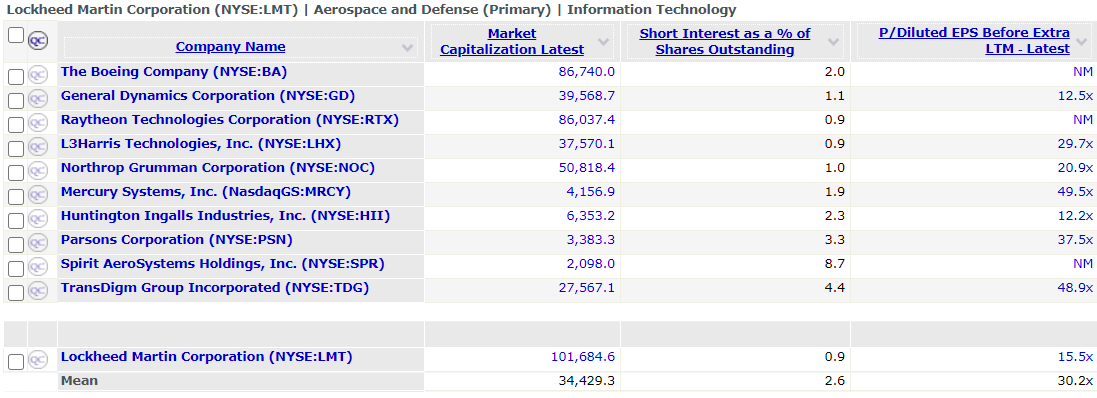

LMT – Quick Comparables

A few of the competitors are Boeing (NYSE: BA), which is really falling behind now. It’s listed at a market cap of $86 billion. But with all the bad press it’s had over the years, from planes going down inadvertently to grounding an entire fleet of airplanes, that market cap is going to continue to get trimmed.

Lockheed Martin is the largest company on the list here, at $101 billion. And some of its competitors, like General Dynamics (NYSE: GD), Raytheon (NYSE: RTX), Northrop Grumman (NYSE: NOC), are all companies that compete for some military contracts in some of the same areas as Lockheed Martin.

Short interest is as a percent of shares outstanding. It gives us an idea of how many investors are out there looking to sell this company short (expecting shares to go down).

Lockheed Martin, just 0.9% of its shares outstanding, has a very small portion. The average for these companies is 2.6%. And you can see some of Lockheed’s more direct competitors, with Northrop, Raytheon and General Dynamics, are all at roughly 1% or less. So, Lockheed Martin just stays in that ballpark, and it’s really nothing alarming there.

When you look at its price-to-earnings ratio, Lockheed’s at 15.5 times earnings. The average for these companies is 30.2. When you look across the board, Northrop Grumman is 20.9 times earnings, and other companies are at 37.5, 48.9, 49.5.

So, Lockheed Martin is doing well. The main thing we’re looking at here is if it’s overvalued compared to its peers. And it’s not. Lockheed’s actually undervalued and that will be appealing to investors.

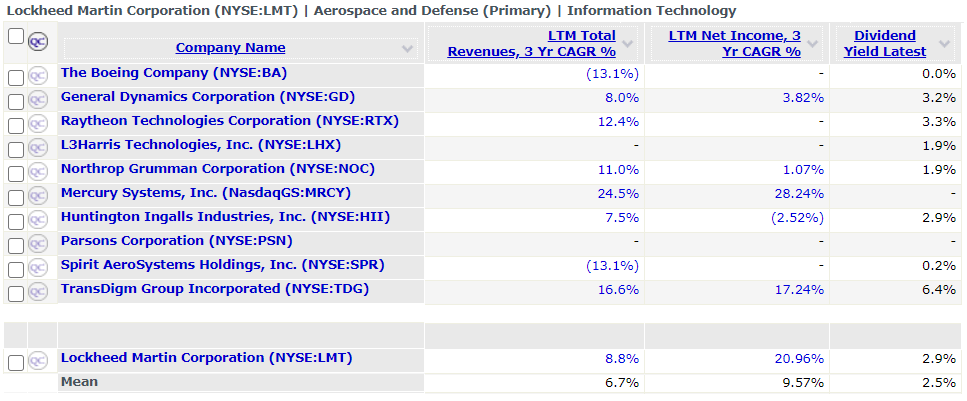

Now, let’s flip over and take a look at the revenue growth in net income over the last three years, the compound average annual growth rate (CAGR).

And for Lockheed Martin, it’s 8.8% for revenues and 20.96% for net income. Those are very consistent and steady growth rates, helping the stock stand out.

When we look at the average revenues, 6.7%, we see that Lockheed Martin is growing faster than many of its competitors.

And net income is 9.57% on average. Lockheed Martin has more than doubled the average amongst its peers, showing that it’s figured out a way to help generate positive earnings growth on a consistent basis.

We know from expectations from the Key Stats chart that net income and total revenues over the next three years are expected to continue. And a lot of that has to do with Lockheed’s huge built-up backlog.

This is a company that’s thinking ahead of the competition when it comes to revenues and net income. And to top it off, it has a dividend yield to go along with it.

At 2.9%, Lockheed’s below General Dynamics, at 3.2%, and Raytheon Technologies, at 3.3%. So, this shows that Lockheed Martin is one of the ideal plays in this sector, because it has stronger growth rates, a lower price-to-earnings ratio and still a solid dividend yield.

Analyst Recommendation

Now, I always like take a look at estimates from the analyst community. S&P Capital IQ took the average analyst recommendation out of 20 analysts that cover the stock and have it rated as an outperform, 1.81, with a 1 being a very strong buy and a 5 being a very strong sell.

So, the analyst community is extremely bullish on this stock, screaming that Lockheed Martin is a buy right now.

LMT — The Technicals

Now, let’s dive into our price chart for Lockheed Martin since 2018.

The stock was stuck in a downtrend from 2018 to early 2019 and then started to make a massive rally out of it. That lasted up till the coronavirus lockdown in March. The stock peaked at around $440 a share.

The dotted lines you see on the chart above show how Lockheed has traded based on these key levels over the past two years. But these ups and downs have created an extremely wide uptrend, from the solid green support line that goes up to around $280 a share, to the solid red resistance line that’s well above $400 per share.

Now the dotted lines between $340 and $400 are the shorter-term trends to watch.

Right now, we’re stuck in between these key levels.

There’s a lot of uncertainty for investors.

You don’t know if people are accumulating more shares for another massive breakout, or if it’s about to break lower and continue to fall back down to the solid green support line you see on the chart.

Those are my key levels to watch.

The dash lines are going to be the key resistance and key support lines. Because, when we look at these patterns, trying to play the guessing game and jump in before the breakout occurs is extremely difficult.

Even though periods of consolidation like this tend to be bullish patterns and send stocks higher, they don’t always do that.

One of the biggest things here to take away from this stock is that it could fall all the way to the green support line, down around $280-290 a share, and still be in an uptrend.

Now, it’s a massive drop and it looks very steep, but as long as the stock makes a high above the previous low, that’s a bullish sign for it to stay in an uptrend.

Reviewing the Checklist

Overall, this is a stock that we’re going to have on our Bank It list today.

We ran through the fundamentals. The net income and total revenues were in steady growth, a bullish opportunity for the stock.

For sentiment, while the analyst community was extremely bullish, another sentiment rating I use is on the 200-day moving average.

Right now, it’s trading sideways and the stock is trading right around the average. So, the sentiment rating is not a very clear indicator of where we’d like to see the stock heading at the moment.

But when we looked at the price chart, the overall trend is to the upside.

And for my price target, if it gets the bullish breakout to the upside out of the short-term consolidation, we’re going to be looking at a stock that’s heading north of $500 a share.

My 12-month price target is $510. That’s about $100 added to the top of this breakout that we would expect to see Lockheed Martin head over the next 12 months. So that’s about a 35% price move to the upside

Let’s put Lockheed Martin on the Bank It list for today.

Bank It — With Options

Lockheed Martin is a company that will continue to benefit from global threats and tactics. It’s $140 billion contract backlog will help it weather any short-term slumps.

But, as you can see in my Bank It or Tank It video, there’re several short-term trends to watch on this stock.

These key levels make for great entry and exit points into the stock, along with my overall view.

The best way to capitalize on the short-term price moves these key levels highlight isn’t by owning shares of the stock — it’s buying options.

Options give you leverage and exposure to the stock. But they also let you define the amount of money you’re willing to risk. You can benefit from high priced stocks at a much cheaper price.

With options, you are in a position to get a quick double-digit or even triple-digit return in just days.

They are my favorite way to capitalize on short-term moves in the stock market. There’s mispricing opportunities that come up practically every week in the stock market. And I know exactly how to take advantage of them.

I want you to be able to take advantage of these as well.

That’s why I’ve broken down my No. 1 approach to trading options in a simple 30-minute training video.

Click here to check out how I trade options.

Regards,

Chad Shoop, CMT

Editor, Quick Hit Profits

P.S. If you’ve never traded options before, you’re not alone. Many people don’t even know how to access them in their accounts. Options are one of the best and safest ways to make triple-digit gains in the market. And our options expert Chad Shoop wants everyone to be able to make their own trades. He’s created a Weekly Options Corner to help his readers learn the basics. It’s completely free. All you need is your email address.