Last Friday, Federal Reserve Chair Jerome Powell spoke at Jackson Hole, Wyoming. This is a traditional location for Fed chairs to make important pronouncements.

The Kansas City Fed has hosted an annual conference in Jackson Hole since 1982. Officials started holding conferences a few years earlier. During that time, locations changed and the speeches didn’t generate much interest.

In 1982, conference organizers decided to change that. They wanted a big name for the conference. At the time, no one was bigger in the global central bank community than Paul Volcker. That’s literally true. Volcker was 6 foot 7 inches tall. He was also the Fed chair.

Powell admires Volcker. We know that from the last line of this year’s Jackson speech: “We will keep at it until the job is done.” The title of Volcker’s autobiography is Keeping At It.

The two chairmen share a focus on inflation. Under Volcker’s leadership, the Fed raised short-term interest rates to 20%. That led to a recession and double-digit unemployment. President Reagan supported Volcker, and the runaway inflation that started in the 1970s came to an end.

In 1982, Volcker was busy and in demand as a speaker. To lure him to the Kansas City Fed conference, organizers decided to hold the event in Jackson Hole. The invitation Volcker received noted that there would be time for fishing.

As an avid fly fisherman, Volcker was familiar with Jackson Hole. He decided to attend so that he could get some fishing on his schedule.

The conference has attracted Fed chairs ever since. The chair often makes news as he or she speaks. They can even move markets.

Words That Rock Markets

In 2002, then-Chair Alan Greenspan spoke about bubbles. He said: “As events evolved, we recognized that, despite our suspicions, it was very difficult to definitively identify a bubble until after the fact — that is, when it’s bursting confirmed its existence.”

This seems obvious to traders, but Greenspan was speaking to economists. Some of them believe markets are efficient and bubbles are impossible.

Greenspan had also triggered a stock market panic. In 1997, he mentioned crises in Mexico and Thailand. Mexican stocks sold off before Fed officials could clarify the boss was referring to 1994.

Ben Bernanke triggered a rally that lasted for months in 2010 when he explained how quantitative easing could push stock prices up.

Last year, Powell’s speech reminded traders that the Fed was going to stay focused on inflation. His comments sparked a seven-day sell-off that pushed the S&P 500 down more than 7%. Almost half of that loss came on the first day.

This year, Powell mostly repeated his 2022 speech. He noted that inflation was high. He assured everyone that the Fed wouldn’t ease up. If unemployment rises or the economy slows, the Fed will keep at it — with “it” meaning inflation.

Powell also noted that the Federal Reserve is watching inflation in different ways. In addition to the overall level of prices, the Fed is looking at inflation in the prices of goods, services and housing.

This data for all three groups is shown in the chart below.

Fed’s Inflation Watch on Goods, Services and Housing

(From the Federal Reserve.)

Two of the factors Powell is concerned with — goods and services — are falling.

Housing costs are flat year-over-year. That’s the green line, which is data provided by Zillow. You might notice that Zillow’s data is more recent than the official government sources. It seems that private sector economists are able to publish data a little quicker than the bureaucracy staffed by the rich men north of Richmond.

The blue line shows that inflation for goods is also falling in line with the Fed’s expectations. This makes sense. Supply chain chokepoints eased. Demand is decreasing as consumers spend down savings. It’s likely that inflation for goods will remain low.

The problem in the chart is the inflation related to services, shown by the red line. This includes personal care services like hair stylists and dog groomers. It also includes recreation activities like gyms and movies, as well as insurance and medical care.

The chart shows that price increases were fairly steady, averaging about 4% before the pandemic. Now, services cost 7.5% more than they did a year ago. This might be the new level this inflation measure settles at.

Service providers are playing catch up. Goods prices surged in 2021. Service providers couldn’t raise rates that quickly. They tend to raise rates slowly and steadily to avoid losing customers. This is true for personal services, insurance companies and other service providers.

All that said, the Fed’s battle is far from over. This is important for investors to remember. Inflationary environments tend to lead to volatility in stocks. And this should bring plenty of trading opportunities for investors in the short-run.

Regards,

Michael Carr

Editor, Precision Profits

Corporate America’s Message to the Economy

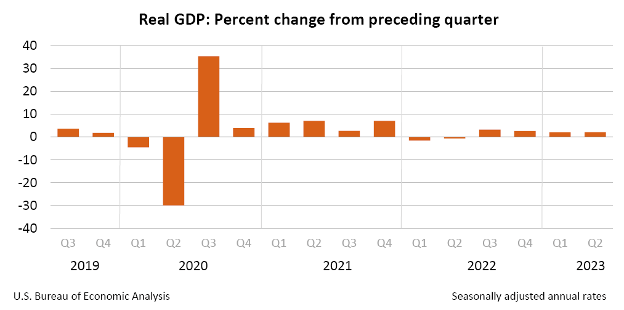

The Commerce Department released a revised estimate for second-quarter gross domestic product (GDP) this week.

It seems the economy isn’t growing quite as briskly as previously thought. The new data shows GDP growing at a 2.1% annualized rate, as opposed to the 2.4% originally recorded.

GDP growth has been tepid for the past six quarters. We may not officially be in a recession, but it’s certainly starting to look like a slow-growth rut.

(From BEA.)

That 0.3% difference between the original estimate and the revision isn’t all that interesting at face value. As usual, the real meat is in the detail.

Businesses have massively reduced their inventories. Rather than grow by $9.3 billion, they actually shrank by $1.8 billion. Now, in a $26 trillion economy, a couple billion dollars is chump change. This revision only lowered the growth rate by 0.14%.

I’m less interested in the number, and more interested in the story this tells.

If you’re running a business, and you expect the coming months to be strong, you order more inventory. If you think lean times are coming, you order less. Corporate America is sending a message here: The second half of the year isn’t expected to pick up.

Again, this doesn’t scream “recession.” While I think it’s likely, I think there is also a good chance that we’ll see a muddled, slow-growth malaise instead. In which the economy doesn’t shrink, but it certainly doesn’t grow fast enough either.

Either way, it’s not what I would consider a robust justification for stock prices at current levels.

However, there’s one modest bright spot. The Federal Reserve’s preferred inflation metric, the PCE Price Index Excluding Food and Energy, was also revised ever so slightly lower: from 3.8% to 3.7%.

That’s still far above the Fed’s target of 2%, but at least it’s trending in the right direction.

Regards,

Charles Sizemore

Chief Editor, The Banyan Edge