I was supposed to be in South Africa at the end of next week.

Suddenly, however, I won’t be.

Thanks to the newly identified Omicron variant of COVID, the risk of lockdowns — and the possibility of a canceled return flight — we must delay seeing our loved ones for at least another six months. (It’s already been two and a half years.)

That’s got me thinking about a critical part of my job: predicting the future.

Every one of us here at Banyan Hill is in the prediction business. Whether it’s a stock, an option or a cryptocurrency, our job is to forecast which ones will gain in value.

But if there’s one thing that the last two years have proved, it’s the difficulty of making accurate predictions during a global pandemic.

At times of extreme uncertainty, external factors drive the prices of individual stocks.

Some are “a bit” predictable, like the actions of the Federal Reserve.

Others are true “Black Swans” — completely unpredictable events such as Omicron.

In “normal” times, on the other hand, we’re supposed to be able to predict the movement of stock prices using standard models.

But what if there are no normal times?

A fascinating article by a famous investment analyst convinces me that this is exactly the case.

Oops … the Models Don’t Work

In 2017, Dan Rasmussen of financial research group Verdad wrote an article about how professional finance analysts pick stocks.

One way is the Discounted Cash Flow (DCF) model.

You predict a company’s growth rates and profit margins in coming years. Then you assign a current value to those future cash flows using Treasury yields as your “risk-free rate.” That gives you the “correct” price of every stock.

The other way is the Capital Asset Pricing Model (CAPM).

Because the future is impossible to predict, stock prices will always vary from DCF predictions. People care about the variation in stock prices — at least as much as they do about total returns. That’s why investors don’t put all their money into the one stock with the highest future cash flows. Instead, they adjust their allocations according to how much each stock tends to vary from the overall market — its “beta.” The equilibrium price that emerges from this market activity is the “correct” price.

The problem is that neither of these models works. They don’t predict stock prices … at least not current prices.

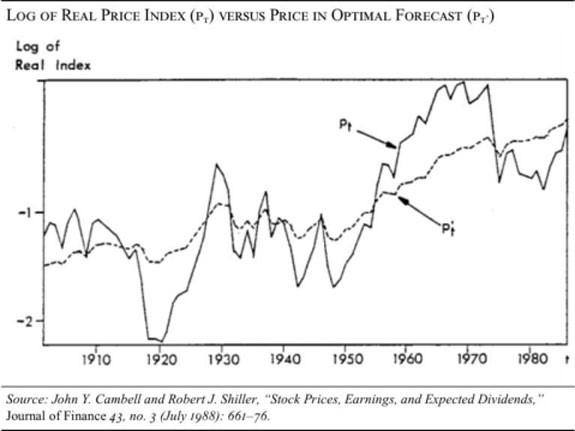

In 2013, Robert Shiller won the Nobel Prize in economics. He got it because his research had shown conclusively that neither the DCF nor the CAPM models worked when back tested against actual stock market history.

The graph below shows predicted stock prices based on the DCF model — the dashed line. The solid line is actual stock prices:

If that’s the case, why do professional investment managers in top Wall Street funds continue to use these models? Rasmussen had a cheeky answer:

Finance professionals rely on discounted cash flow models and capital asset pricing assumptions not because they are correct but because they are required for planning purposes. — Dan Rasmussen, Verdad

In other words, the future is impossible to predict … but you can’t run an investment business without predictions.

The fact that they are usually wrong is irrelevant.

Sentiment Is King … at Least for Now

The graph above shows that actual stock prices gyrate wildly above and below the cash flows produced by companies.

But the overall direction of both the predicted and actual lines is the same — gradually upward over time.

This proves two critical things about the stock market:

- In the long run, cash flows determine the direction of stock prices.

- At any given moment, investor sentiment decides actual stock prices.

I’m sure you can see the problem.

All of us here at Banyan Hill invest in companies that we believe have the potential to produce great future profits. We know that realizing that potential takes time.

But the investors who subscribe to our services have strong feelings about short-term price movements. When stock prices are surging up and away from what earnings models predict, they want part of that action. And when they dive below the model’s predictions, they want out … fast.

It’s precisely that sentiment that drives stock prices up and down.

On Friday, for example, news about Omicron led to a steep dive in stocks related to “reopening.” Stocks of “lockdown” companies surged.

These price movements make no sense.

Sentiment ruled — as it always does in the short term.

Stay Smart and Tough

None of the companies whose prices fluctuated so wildly on Friday were any different from what they had been the day before. Their long-term earnings won’t be any different because of Omicron.

But that’s not how it feels to most individual investors. Their instinct was to protect their gains and minimize their losses … even if surrendering to sentiment undermines their long-term returns.

Thanks to that sentiment, short-term stock prices are extremely difficult to predict at the best of times. Trying to predict them in the midst of a global pandemic is a crapshoot.

But there are two things we can predict with 100% accuracy:

- Sentiment will always rule in the short term. It certainly did on Friday.

- In the long term, investors who hang on to companies with a bright future will see the best rewards.

I can’t predict when I will next set foot in my beloved home in Cape Town. But I know I will.

I can’t predict when stocks that have taken a drubbing thanks to COVID will bounce back.

But by focusing on the fundamentals, I know they will.

Kind regards,

Ted Bauman

Editor, The Bauman Letter