Global markets are feeling whiplash as Europe severs financial ties to Russian gas and oil providers.

The race to renewables is on, but will we get there before a major economic slowdown?

In today’s weekly recap, I dive deeper into the war for our energy future and share my favorite pick for weathering the current storm.

Transcript

Hello everyone. It’s Ted Bauman here, editor of Bauman Daily with your weekly Friday video.

Today, I want to talk about energy more particularly where global energy markets are likely to go over the next decade or so with the impulse behind them coming from Russia’s invasion of Ukraine. Trends that were already underway are going to accelerate dramatically. In fact, they already are. So let’s look at some of the background here. Russia produces nearly a fifth of the world’s natural gas, and more than a 10th of the world’s oil supplies. Thirty percent to 40% of the European union’s natural gas supplies come from Russia. That’s how they heat their homes and their stoves over there. This has fallen in recent months. It’s down to about 20% as the European union has switched some of its sources of supply of gas, going to come to that in a moment.

But one of the critical things here is that this big chunk of the world’s energy production, particularly Europe’s energy production could disappear in short order, not just because of sanctions, but because it looks like energy companies and energy traders don’t want to do any business with Russia, sanctions or no sanctions. So let’s look at a chart that show as Russia share of European union and UK natural gas supply.

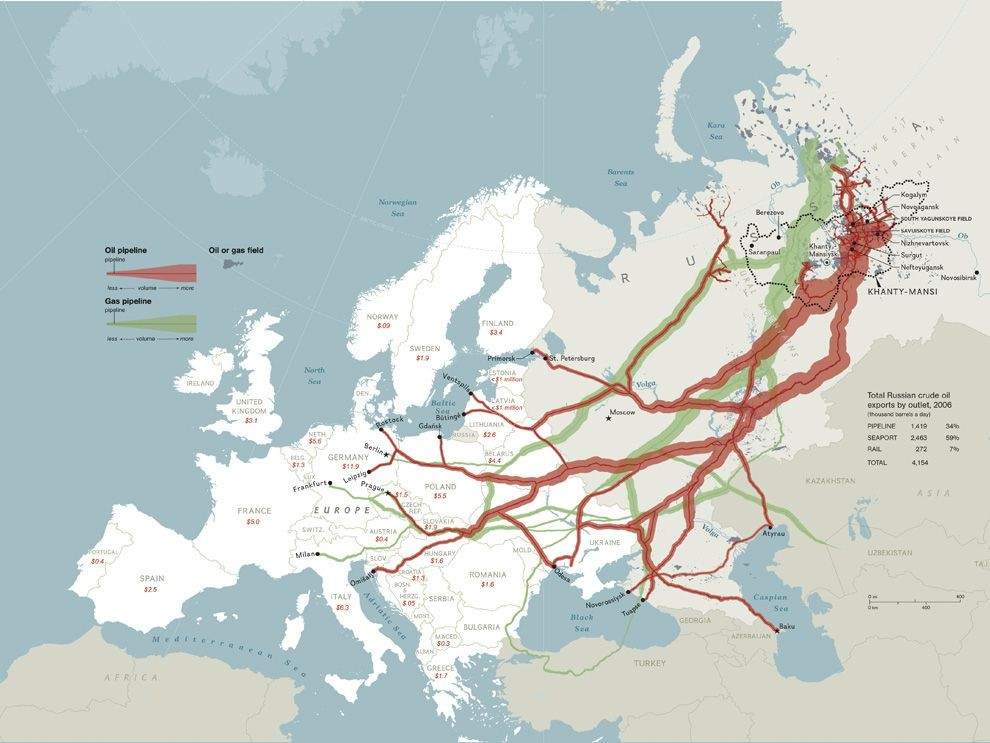

Going back over the years, essentially the story is falling domestic production, a slightly rising production from Russia, but then increases in other gas supply. You see, particularly in 2019 and 2021, there were big increases in the sources of other gas supply. We’re going to come to what that means in a minute. Well, here’s why this is so important. Here’s a picture that shows really the pipelines and the volume of the pipelines, oil and gas coming from the Russian gas fields in Western Siberia.

Now, as you can see these natural gas and oil pipelines really snake all over Eastern Europe, but once they get to Western Europe, they then branch out into other supply channels.

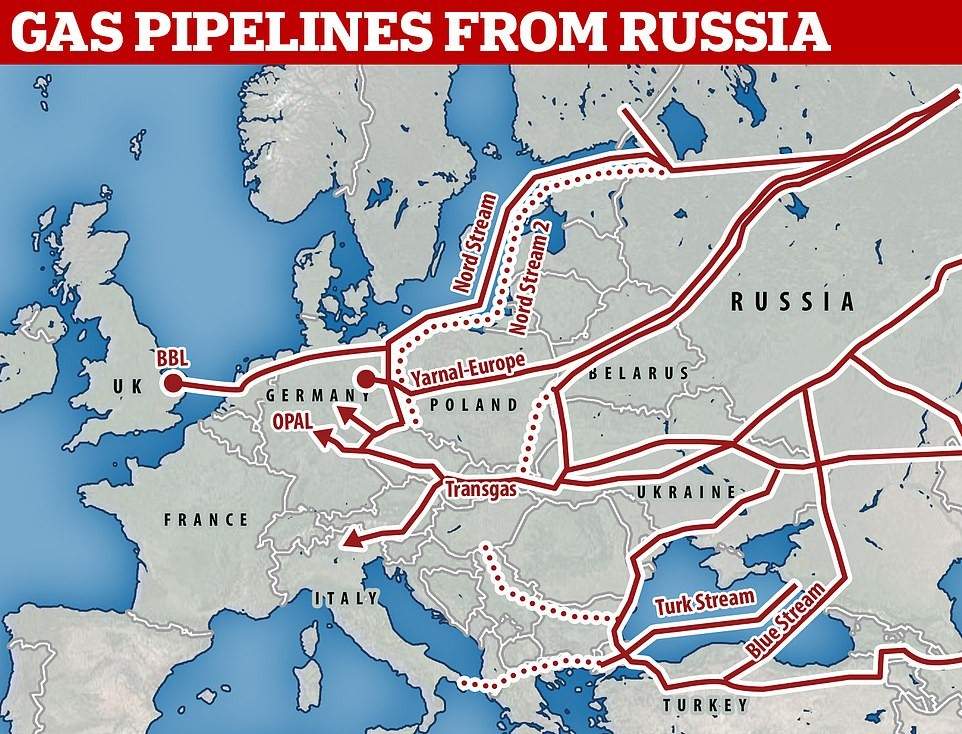

And here’s a chart that shows some of them important ones.

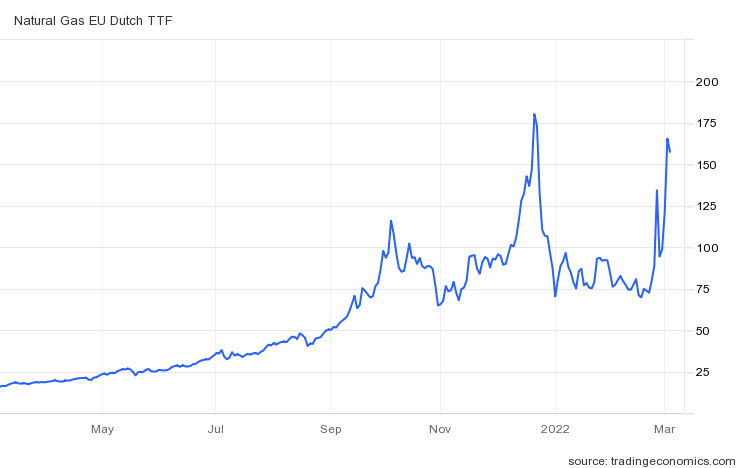

They carry on into Great Britain, Germany, Italy in particular. Now, if you’ll note, you can see that a lot of these pipelines go through Ukraine, particularly those that go into Southern and central Europe, the Transgas pipeline. Russia has tried to bypass Ukraine and send gas through around Belarus, which is likely also to be hit with sanctions soon. But the key thing here is that all of these projected pipeline buildings, for example, you see nor Nord Stream 2 is also in dots. All that’s likely to be put on hold right now. What that means of course, is that the price of natural gas in Europe is skyrocketing, not just in the short term, but in terms of futures. Here is the current price in euros of natural gas on the Dutch Exchange.

Now what’s interesting here is that it spiked before, it’s not as high as it was in December of 2021. But, what’s interesting is that was also a case of Russia slowing down shipments in the middle of winter, really just to show Europe who’s boss.

And that of course is backfiring now, because what we’re going to see, what I’m going to show you is that European consumers, in other words, the companies and the traders that buy energy from Russia are scrambling to get away from Russia as fast as they can, and find other sources of supply. One more chart, just to show you that it’s not just about natural gas.

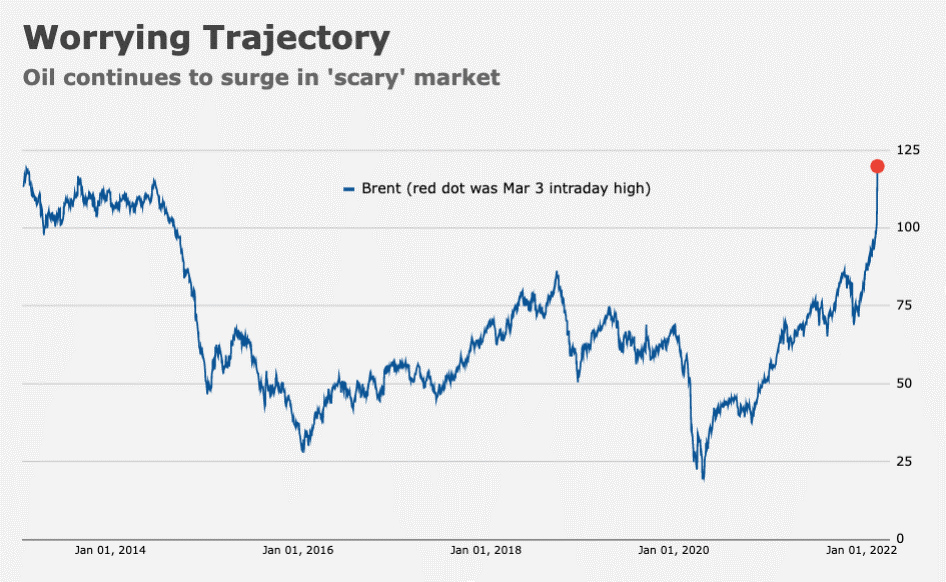

Here is Brent crude. On March 3, it reached an intraday high of over $120 a barrel. We haven’t seen that since 2014. So the critical thing here is that we’re going to see rising energy prices in the short term. JPMorgan Chase predicts that oil could hit $150 barrel, that could knock 1.6% off of global GDP and raise consumer prices around the world by another 2%. Big question is, what do we do about it?

The Russian invasion of Ukraine has showed us that reliance on fossil fuels is not just bad for the environment, it’s bad geopolitical policy, basically. Because if you are dependent on countries digging that stuff out of the ground and then selling it to others, as opposed to using the sunlight and wind that’s around all of us, basically, you hitch yourself to some undesirable wagons. You basically make yourself dependent on them. That’s what’s happened to Russia. And what’s amazing to me is that Western countries have decided that they’re going to put up with the costs of cutting Russia out of the global energy market, because essentially they find that it’s so unpredictable. I mean, it’s just amazing to think that people who a week ago would’ve never thought of ceasing their imports of Russian oil and natural gas are now doing it voluntarily, without sanctions. They just don’t want to be caught with their pants down if sanctions get tightened.

So renewables to the rescue, here’s a picture of a solar array.

And then here’s a picture of a wind farm.

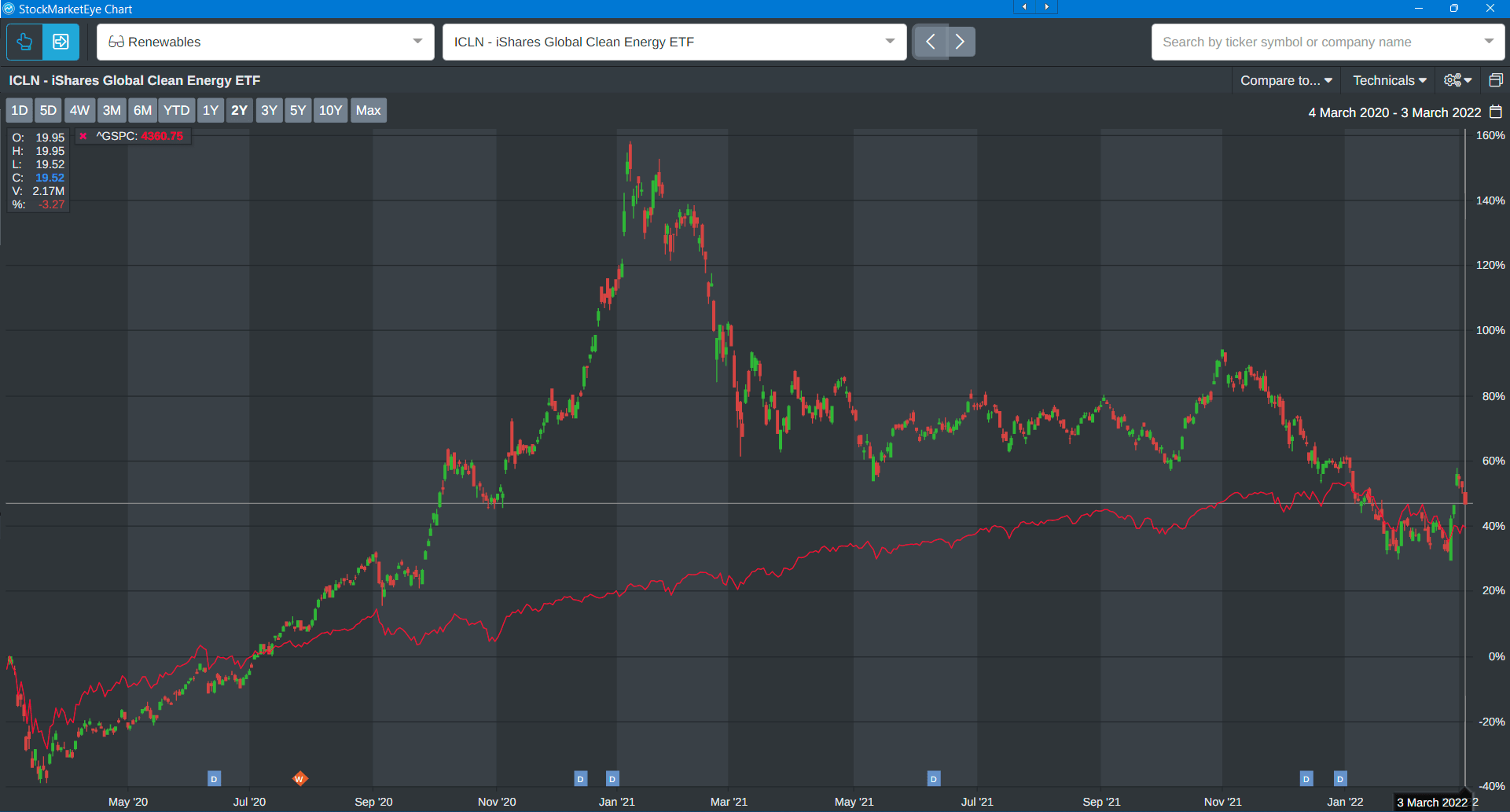

These are the things that are supposed to, in a sense, move us away from this overdependence on fossil fuels and on the countries that produce fossil fuels. Most of which tend to be quite nasty countries. I mean besides Russia, you’ve got Saudi Arabia, Venezuela, other countries that produce oil tend to be fairly corrupt. Anyway, the point is that right now, renewables are not able to bridge the cap immediately. Obviously you’re not going to get wind farms and solar power to substitute for all this natural gas that could be cut off from Russia. Anyway, the market thinks that it will, here’s a chart that shows the ICLN Global Clean Energy ETF.

After spiking to frankly ridiculous levels in early January ’21, trading sideways for a while, and then pulling back very sharply from the third quarter of 2021, with the failure of the Democrats Build Back Better bill, look at the bottom right-hand corner. I’ve shown you, I put a crosshair there to show you that they’ve spiked again. Now this is kind of a knee-jerk reaction. And the reason is that clearly, as I said earlier, these technologies are not going to be substituting for natural gas or oil anytime soon from Russia or anywhere else. What’s the bridging technology everybody’s been talking about it. That there’s going to be an intermediate stage between reliance on oil and coal to when we rely on renewables. And what is it? It’s natural gas. Now Shell, which is one of the world’s biggest producers of natural gas expects global consumption of liquified natural gas to double to almost 700 million megatons by 2040 from its 2020 level. So that’s doubling over the next 20 years.

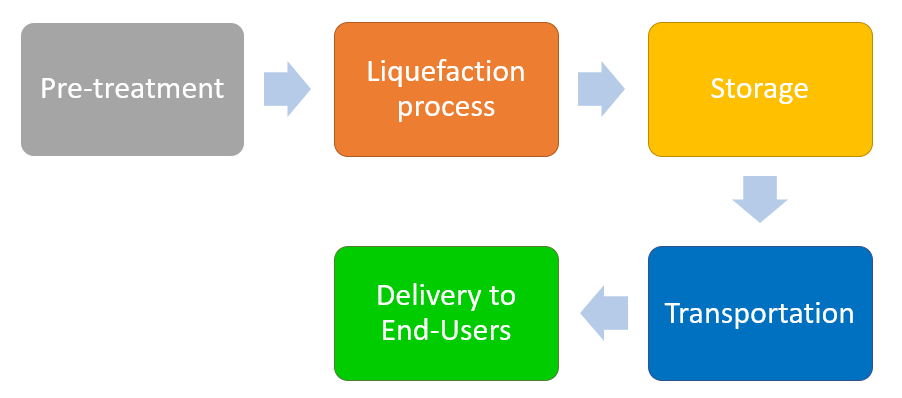

Now, why liquified natural gas? Well, let’s look at a chart that shows what it is.

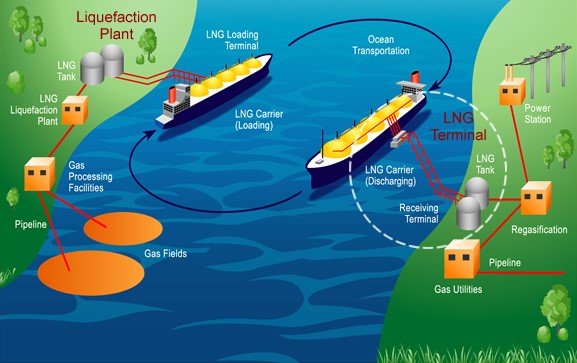

Here’s a flow chart that shows liquified natural gas is basically just a natural gas which exists in its natural form in a gaseous state, which is then liquified, stored, transported, and delivered to end users. So, you could imagine a situation where instead of a pipeline through which gaseous natural gas flows, like the kind that flows into my house here in Atlanta to supply my stove and my heating system, you could imagine it being delivered in liquid form, like the bottles that we often get to power our gas grills and things. Well, here’s a picture that shows how this works at a global scale.

You have gas fields which produce the natural gas, they’re then processed and cleaned up, some of the impurities removed, then they go into a liquefaction plant, which involves cooling the gas, turning it into a liquid form, storing it in tanks on the shore side, and then put into ships, which then go and do the opposite on the other side, they go to wherever the exports are headed, they unload.

They are then turned from liquid back into gas, and they’re used for whatever they’re use for. Here’s a picture of an LNG ship.

This is the classic. It’s basically just big floating tanks, four of them, full of liquified natural gas. Here’s a picture of an offshore terminal.

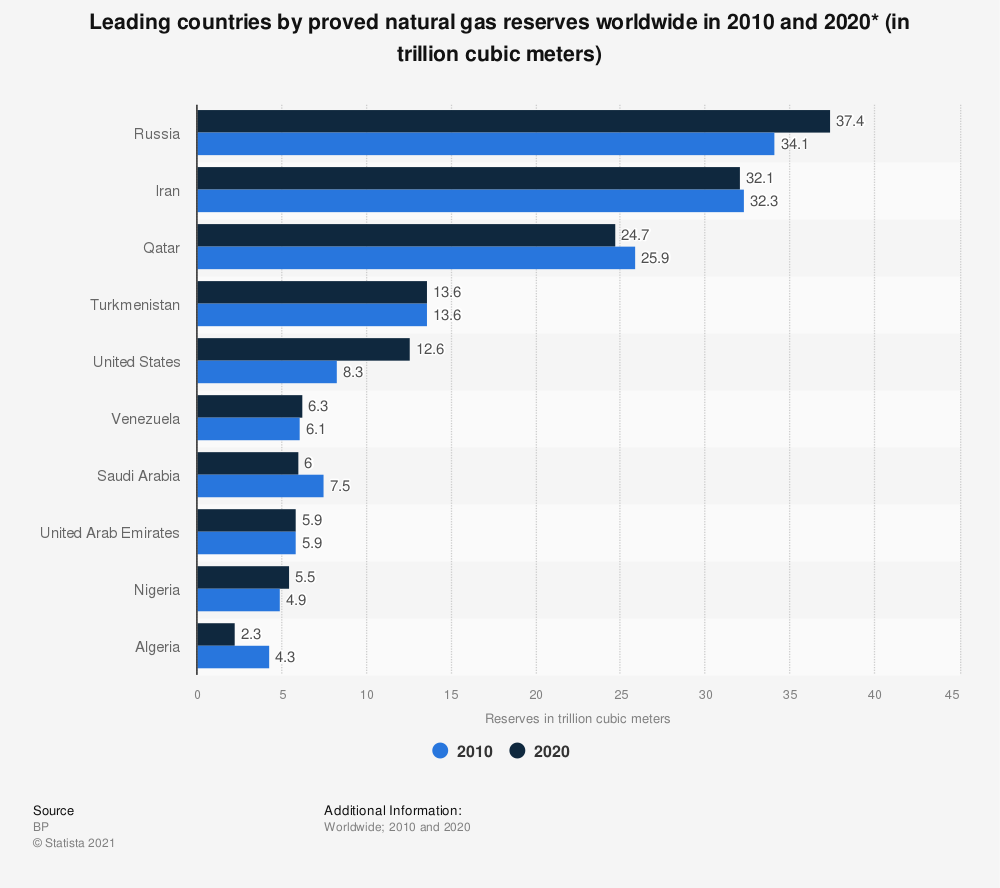

This shows a ship just like that basically unloading its gas and being delivered. Now, what’s so important about liquified natural gas? Whereas with pipelines, you’re tied to a specific geographical arrangement that’s baked in stone, or rather baked in steel, the pipeline, LNG can be sourced from anywhere in the world. And basically if you can get ships to bring it from wherever it is being produced to where you need it, you can actually bypass situations like Russia. Now, here is a chart that shows the leading countries with proven natural gas reserves worldwide.

And you can see that Russia, Iran, Qatar and Turkmenistan are all the biggest in terms of reserves.

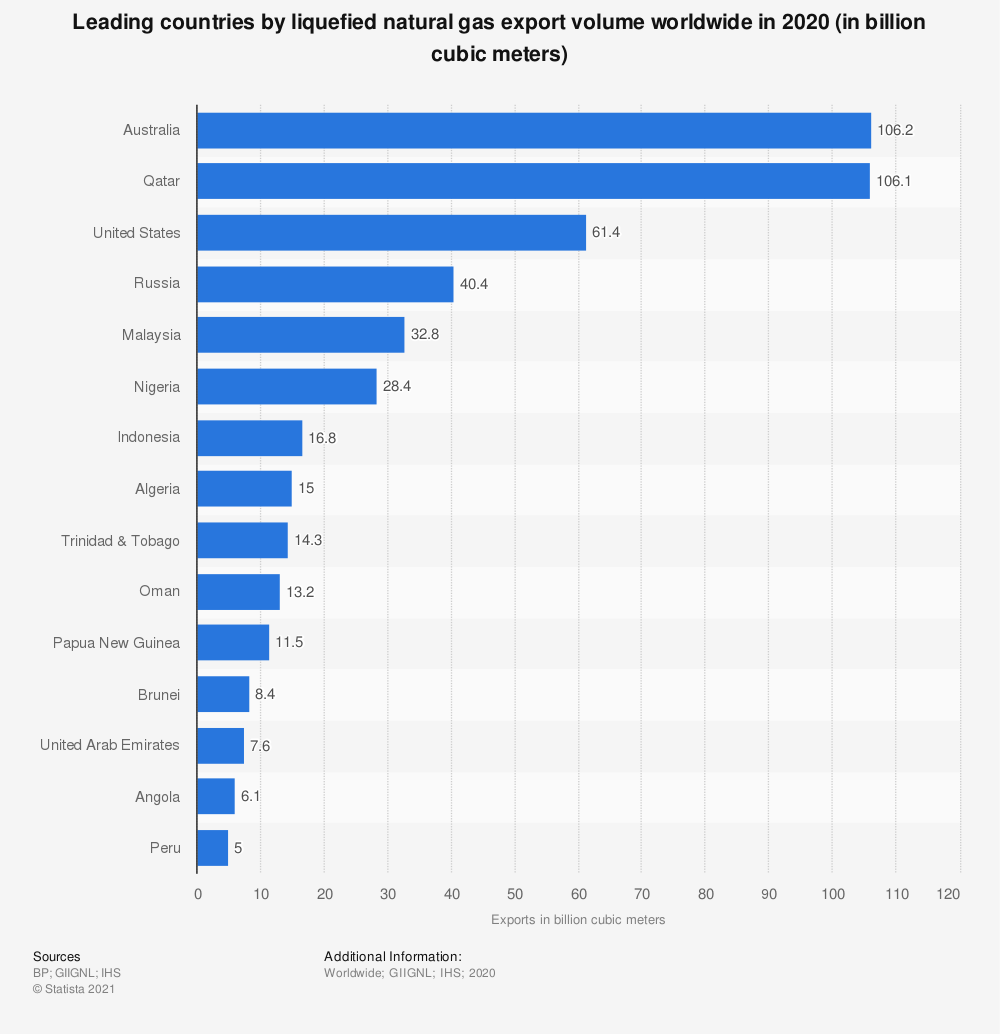

The United States though has increased its reserves very dramatically since 2010. And as I’m going to show you, that has made it one of the world’s top suppliers of natural gas. Here’s a chart that shows leading countries who export liquified natural gas.

This was in 2020, Australia and Qatar at the very top, but look who’s number three? United States. It’s bigger than Russia. Russia has more natural gas than United States, but the United States exports more of the liquid stuff. Of course, one of the reasons for that is because Russia exports the majority or the bulk of its natural gas in gaseous form and not liquid. But the point is that there are plenty of other countries who could step in to supply Europe with its natural gas in liquid form if necessary. Why do I mention all this? Well, because there are two things driving the liquid natural gas market right now. One is the Russia situation. Everybody is scrambling to find ways to top up Europe’s natural gas supplies, their stored supplies.

If they can get liquified gas from the US or Australia or Qatar or wherever, they can store it for this coming winter. In other words, the next winter at the end of 2022, and that would allow them to continue sanctions against Russia if the situation has not been resolved. So that’s good for LNG producers and shippers. But there’s another thing that’s also good. It’s recognized now that we’re not going to be able to make an immediate seamless transition from relying on coal and oil-fired power plants to produce electricity and other things. We’re going to need an intermediate stage between now and renewable energy. And that is liquid natural gas. The idea being that if you can get the technology right, and if you can put the supply chains in motion, you could actually move as an incremental step away from coal and oil towards natural gas as a maybe 10 or 15 year transitional phase, and then move while you’re building up your renewable energy.

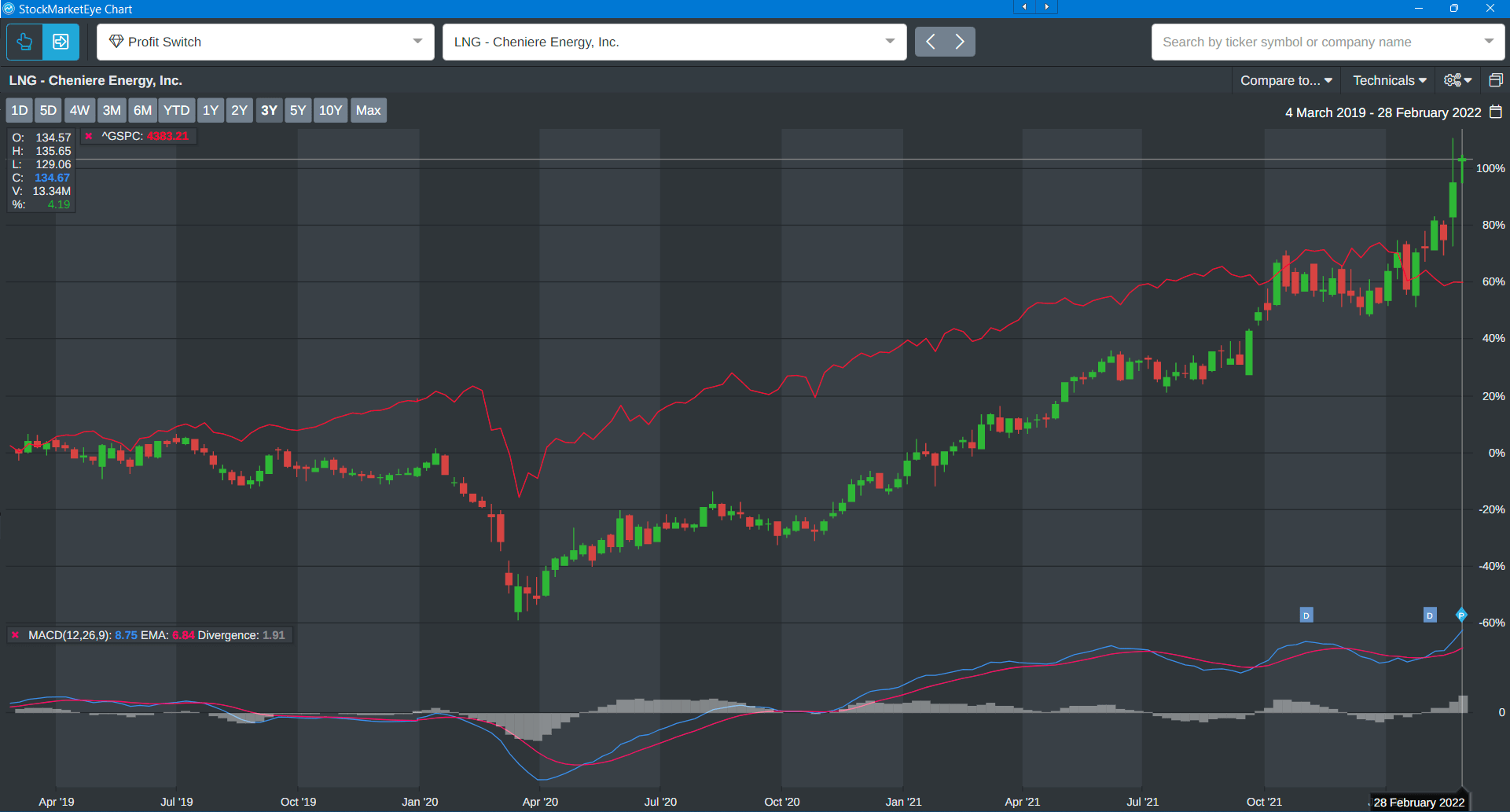

Now, the problem with that is that there has been a reluctance to invest in liquid natural gas or any other natural gas in terms of power plant technology, simply because it’s considered a fossil fuel. The fact that it’s a cleaner burning fossil fuel doesn’t make people willing to invest in it. That means that there is a shortage of new investment into LNG, which means that existing companies are going to be trading at a premium. So today I’m going to give you a pick. This is Cheniere Energy.

This is one of the first companies to produce liquid natural gas in the United States, started in 2016. It’s become the leading LNG producer, it’s the second largest LNG operator and fourth largest supplier in the world today. Basically what they do, they buy natural gas on the open market. They pipe it to their liquefaction plants on the Gulf Coast. They fill it into their ships and they take it to wherever the highest bid willing to buy it from them.

They tend to operate on long-term fixed contracts, which means that they have built-in revenues going forward, which is always a nice business model to have. Obviously they can charge premiums in situations like this. But here’s the critical thing. Here is the stock price for LNG. After trailing behind the S and P 500 for a long time, it is now comfortably above the S and P starting really at the beginning of February, rather at the beginning of this year in anticipation of issues happening in Russia. So the key thing here is that we’ve experienced a breakout, but I predict that not only will it sustain this breakout, but companies like this are going to become ever more important to the global energy mix over the next 10 to 15 years, because we’re going to depend on what they produce and transport in order to make it possible for us to get from where we are now, which is coal and oil and get essentially to renewables.

So there’s a pick for you. It’s LNG. I believe that it’s a company that’s going to do very well in the short, but also in the intermediate term. In the long-term, of course, all of this stuff is going to have to disappear as we move in the direction of renewables. But in the short-term, particularly if you’re in Europe, you don’t really have much of a choice. And when it comes to markets, nothing is better than somebody who doesn’t have a choice when it comes to supply. Because that is where prices go up. And so do the share prices of the companies that supply that stuff. Anyway, this is Ted Bauman signing off. I’ll talk to you again next week. Bye-bye.

Kind regards,

Ted Bauman

Editor, The Bauman Letter

Curious how AI will play a role in the energy sector? Click here to read Ian King AI energy coverage.